sturti

Today, we are putting TransMedics Group, Inc. (NASDAQ:TMDX) in the spotlight. This company provides the technology needed to transform/enable organ transplant therapy for end-stage organ failure patients. The company’s stock has more than tripled since the summer market swoon ended in late October. Can the good times continue for shareholders? An updated analysis follows below.

Seeking Alpha

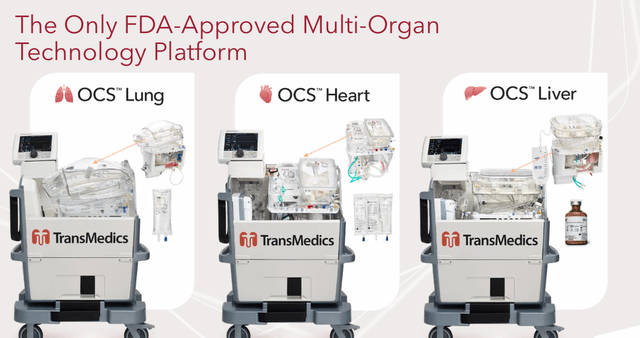

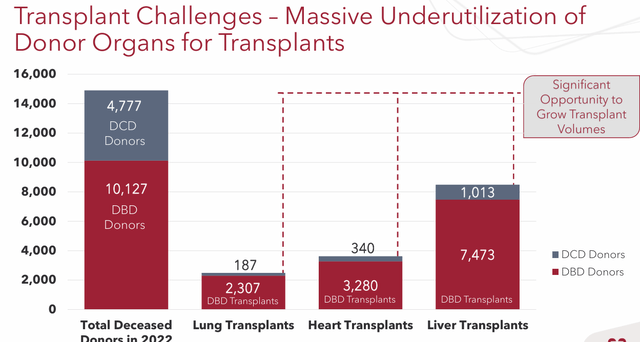

TransMedics Group is headquartered in Andover, MA. The company had developed a portable organ perfusion, optimization, and monitoring system called Organ Care System {OCS} which has been modified to allow the transport of lungs, livers and hearts for organ transplants primarily in the United States. These systems increase the amount of donor organs that can be utilized.

February 2024 Company Presentation

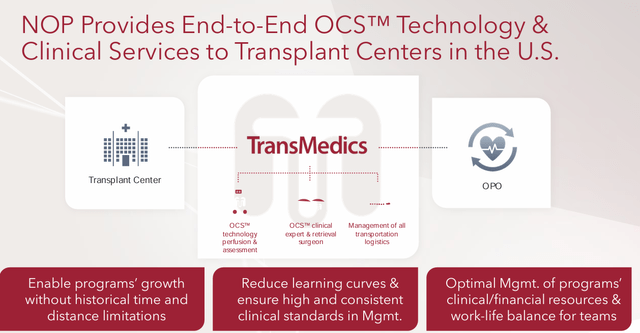

TransMedics also runs a national OCS program. This is a turnkey solution for outsourced organ retrieval. It provides OCS organ management and logistics services, including aviation and ground transportation, as well as other coordination services needed in organ transplants. The company is building a fleet of jets to deliver these critical products. TransMedics had nine active planes online as of the first quarter and is looking to grow its fleet to 15 to 20 planes over time. Eventually, 80% of overall transplant deliveries will be done, all internally from a logistical perspective.

February 2024 Company Presentation

With the rally in the shares, the stock trades at around $153.00 a share and sports an approximate market capitalization of $5 billion.

February 2024 Company Presentation

Recent Results:

TransMedics posted its Q1 numbers on April 30th. They were outstanding results. TransMedics delivered GAAP earnings of 35 cents a share. The analyst consensus estimate was looking for a one cent a share loss. The company had net income for the quarter of $12.2 million, compared to a loss of $2.6 million in the same period a year ago. Operating expenses did rise some $16.6 million from 1Q2023 to $47.5 million. This was primarily due to a rise in R&D expense and other growth enabling initiatives.

Sales rose 132% on a year-over-year basis to just under $97 million, some $13 better than expectations. Thanks to a greater proportion of overall sales from service revenues, gross margins fell to 62% from 69% in 1Q2023, but were up sequentially from the 59% level in the fourth quarter of last year. Liver transplant services drove two thirds of overall revenues, with heart transplant related revenues making up most of the rests. Logistics revenues made up $14.5 million of contributions. International revenues rose 16% on a year-over-year basis to $4.1 million.

Leadership also boosted FY2024 sales guidance by $30 million over previous estimates to a new range of $390 million to $400 million. This would represent 61% to 66% revenue growth from FY2023.

Analyst Commentary & Balance Sheet:

Obviously, the analyst community has liked what they have seen from recent results. Since Q1 numbers hit the wires, seven analyst firms including J.P. Morgan and Piper Sandler have reissued/assigned Buy ratings on the stock. Three of these contained upward price target revisions. New price targets proffered range from $117 to $175 a share. Here is Stephen’s take on TMDX when they initiated the shares as a new Outperform with a $151 a share price target early in June:

Technology is helping drive improved outcomes and increased donor organ utilization “to better meet market demand.” TMDX’s National OCS Program and aviation logistics program “capture the entire organ transportation process, reducing costs and deepening customer relationships.”

Several insiders are frequent and consistent sellers of the stock. That insider activity seems to have picked up a bit in the second quarter, as insiders disposed of north of $20 million worth of shares during the quarter. One insider has sold north of $400,000 worth of equity in several transactions in the first few days of July. Approximately 18% of the outstanding float in TMDX is currently held short. The company ended the first quarter with approximately $350 million in cash and marketable securities on its balance sheet. TransMedics listed $59 million of long-term debt on the 10-Q the company filed for the first quarter.

Conclusion:

February 2024 Company Presentation

The company lost 77 cents a share in FY2023 on just less than $242 million in revenues. The current analyst firm consensus has TransMedics swinging to a profit of 80 cents a share in FY2024 as sales soar to just over $400 million in FY2024. They project earnings of $1.12 in FY2025 on just over 30% revenue growth.

February 2024 Company Presentation

The stock is trading with an Icarus like valuation of north of 190 times forward earnings and more than 12 times forward revenues. Granted, TransMedics is the unquestioned leader in its space, which has significant growth opportunities. The rally in the stock has brought the share above all but two analyst firm price targets on the equity. I am not surprised insiders are taking some chips off the table or that the shares have a high short interest.

TransMedics Group, Inc. management has done a commendable job moving the company towards profitability, but at current levels, the stock seems priced for perfection. I would not be shocked to see some profit taking in the shares in the months ahead.

Credit: Source link

{kind=link}