PeopleImages/iStock via Getty Images

Investment Thesis

Spotify (NYSE:SPOT) has few reasons to complain in 2024.

The Stockholm, Sweden-based company finally won their fight against Apple (AAPL) earlier this year, with the EU Commission fining Apple $2 billion for its anti-competitive practices against apps like Spotify.

Then, Spotify reported a strong Q1 FY24 earnings report, which showed a bump in its premium subscribers. But, most importantly, the Q1 earnings report also demonstrated sustained performance in the company’s GAAP profitability progress, putting it on track to report its first full year of GAAP profit.

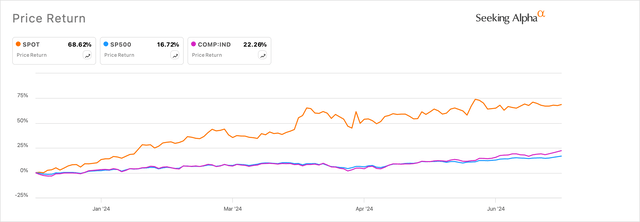

Naturally, the progress has emboldened investors and Spotify’s own management team, as Spotify’s stock has climbed almost 70% ytd versus the broader markets. Spotify’s management feels encouraged to raise prices across its suite of plans, the second price hike in a year.

Exhibit A: Spotify’s stock outperforms the broader markets by at least three times the returns posted by key indices. (SA)

Spotify’s price hikes would otherwise be bullish in my view, but the timing of the hikes, which continues to be in stark contrast to its peers in an uncertain environment, from an inflation point of view has me cautious. I recommend a Hold on Spotify.

Price Hikes May Offset the Impressive Premium User Momentum

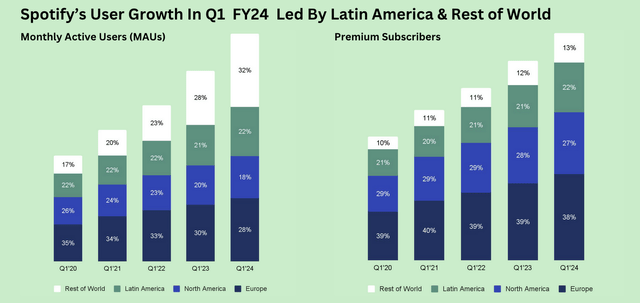

In Q1, Spotify saw healthy growth in users both in its total MAUs (Monthly Active Users) and in its Premium Subscribers as observed in Exhibit B below. The highlight in this part of the earnings report was the solid mid-teens growth exhibited by the volume of Premium Subscribers Spotify added to its platform in Q1 that grew 14% y/y to 239 million, with strong double-digit growth seen in all of Spotify’s business geographies.

Exhibit B: Spotify demonstrates strong growth in its Premium Subscribers growing 14% y/y to 239 million subscribers (Q1 FY24 Earnings Report, Spotify)

While Spotify reported 19% y/y growth among its MAUs to 615 million in Q1, I still think it was an impressive attempt by the music streaming company given that it has promised to spend less on marketing expenses to acquire new users.

I had discussed this in detail in an earlier coverage of how I was left impressed by Spotify’s management’s efforts to optimize its cost structure. Here are my comments from that coverage:

I am encouraged by the observation that the company grew revenue by 16.5% y/y in FY23 while its expenses grew by just 1.5% y/y in the same period. At the same time, gross margins expanded by one percent to 26%, and the company almost became profitable on an operating profit basis in FY23.

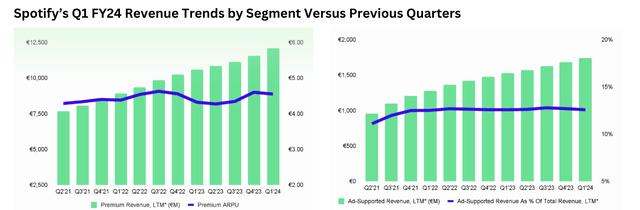

Spotify’s efforts have also led to a resurgence in the ARPU through last year, as seen in Exhibit C below. Premium Revenue, which accounts for ~90% of Spotify’s total revenue, grew by a handsome 20% y/y to €3.3 million, driven by gains in Premium Subscribers that I discussed earlier and a 5% y/y increase in ARPU to €4.55.

Exhibit C: Spotify’s Q1 Report saw surge in Premium Subscribers driving higher Premium Revenue (Q1 FY24 Earnings Report, Spotify)

In hindsight, the growth in Premium Subscribers brushed off the first-ever price hike by Spotify at this time last year, when the company hiked the monthly prices of its Premium plan by ~10% to $10.99. This was also supported by the list of features, such as DJ tools, podcasts, & audiobook content, that were added in the last year.

However, with the company recently announcing another round of price hikes within twelve months already, which would see U.S. subscribers pay an additional 9% to $11.99 per month, I believe this would turn its current subscribers and potential new subscribers cautious. Spotify’s first price hike of 10% seemed warranted and occurred in an environment where core inflation was still growing at 4.9% in June last year.

But its recent price hike of 9% is occurring in an environment where core inflation has slowed to 3.4% y/y per the May 2024 reading. Consumers may not take kindly to such rapid successions of price hikes by Spotify, in my opinion. Recent checks on social networks provide anecdotal evidence that consumers could push back against Spotify’s price hikes.

Moreover, Spotify’s peers have not yet signaled any indication of hiking prices for their music streaming platforms. Apple continues to charge U.S. consumers $10.99. So does Google’s (GOOGL) (GOOG) YouTube Music, also at $10.99 per month. Amazon (AMZN) has kept its prices unchanged at $9.99 for Prime members and $10.99 for non-Prime members. In recent surveys, Amazon’s Prime Music is getting popular among certain subscribers, climbing up the popularity charts. Even Tidal, an independent streaming service, has slashed their monthly fees to $10.99, as well as a few months ago.

In summary, Spotify’s price hikes might look appealing to investors on paper, but a relatively cooling inflationary environment, increasing caution being exhibited by consumers, and a competitive environment will make it challenging for Spotify to justify its prices to its consumers, in my opinion.

Valuation Points To Minimal Upside For Spotify

With the stock up almost 70% ytd, Spotify’s performance in the backdrop does little to justify its valuation.

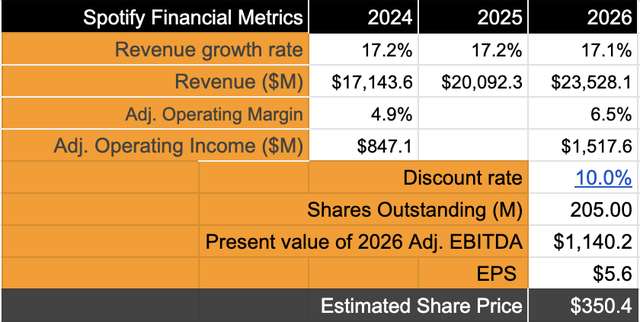

Given the growth rates demonstrated by Spotify, I continue to believe Spotify will grow its top line by a 17% CAGR through FY26. For now, I will assume no impact yet on Spotify from its second round of price hikes due to the lack of factual evidence on the matter, while still being cognizant of the consumer pushback risks I highlighted earlier.

In addition, I believe Spotify will grow its adj. operating income by ~35% CAGR over the same time period based on the superior operating leverage management continues to demonstrate. There is no change in my assumed share outstanding of 205 million, while my discount rate stands at 10%.

Exhibit D: Spotify’s valuation model shows minimal upside (Author)

Spotify currently trades at a forward valuation premium of ~63x, which is expensive but appears justified given that the earnings growth rate expected for Spotify over the next three years will grow four times faster than the long-term earnings growth rate of the S&P 500.

My model indicates ~10% from current levels, but with the risks that I highlighted earlier, I do not feel it is favorable to investors given the risk/reward.

Takeaway

Spotify has been able to engineer an impressive turnaround so far in the last 12–18 months, with management getting mature and focused on growing its business sustainably with an optimized cost structure. The music streaming company continues to demonstrate strong growth in its revenue and its Premium Subscriber base.

However, the recent round of price hikes has me concerned since the company is raising prices in a cooling inflationary environment, with consumers wallets looking stretched and Spotify’s peers so far reluctant to match Spotify’s price hikes, leading to uncertainty.

For now, I will continue to recommend a Hold rating on Spotify.

Credit: Source link

{kind=link}