8vFanI

REITs (VNQ) delivered strong results in the first quarter, with most REITs continuing to grow their cash flows and dividends, and only a handful of them really feeling the pain of higher interest rates.

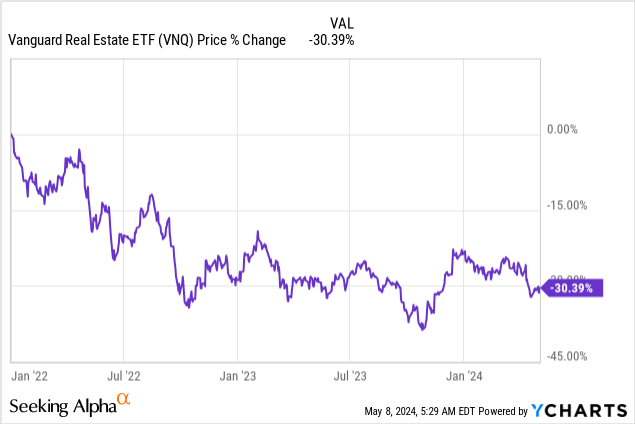

Despite that, they have all crashed as if they were facing a severe crisis. REITs are down ~30% on average, but keep in mind that their cash flows have also grown by ~10% during this same time period:

It is frustrating because we correctly predicted that REITs would perform well in a higher inflation/interest rate environment, but the market has still traded them as if they were just bond proxies. At the same time, the rest of the stock market has kept moving higher as if nothing had happened and as a result, the valuation multiples of most stocks are today historically high:

Multiph

This, of course, makes little sense when you think of it.

Somehow, the cash flows of REITs are now far less valuable, but those of regular stocks are more valuable.

In reality, REITs should have been far less impacted since they generate lots of cash flow already today, benefit from inflation, use little leverage, and have long debt maturities. Growth stocks, on the other hand, should have been much more heavily impacted because their cash flows have a longer duration.

But whether it makes sense or not, it does not change the fact that REITs have now been in a bear market for over 2 years, and many investors are starting to lose patience.

I see it even here on Seeking Alpha. Lots of investors who were happily buying REITs in 2022 have now lost all interest in them as if they were a lost cause.

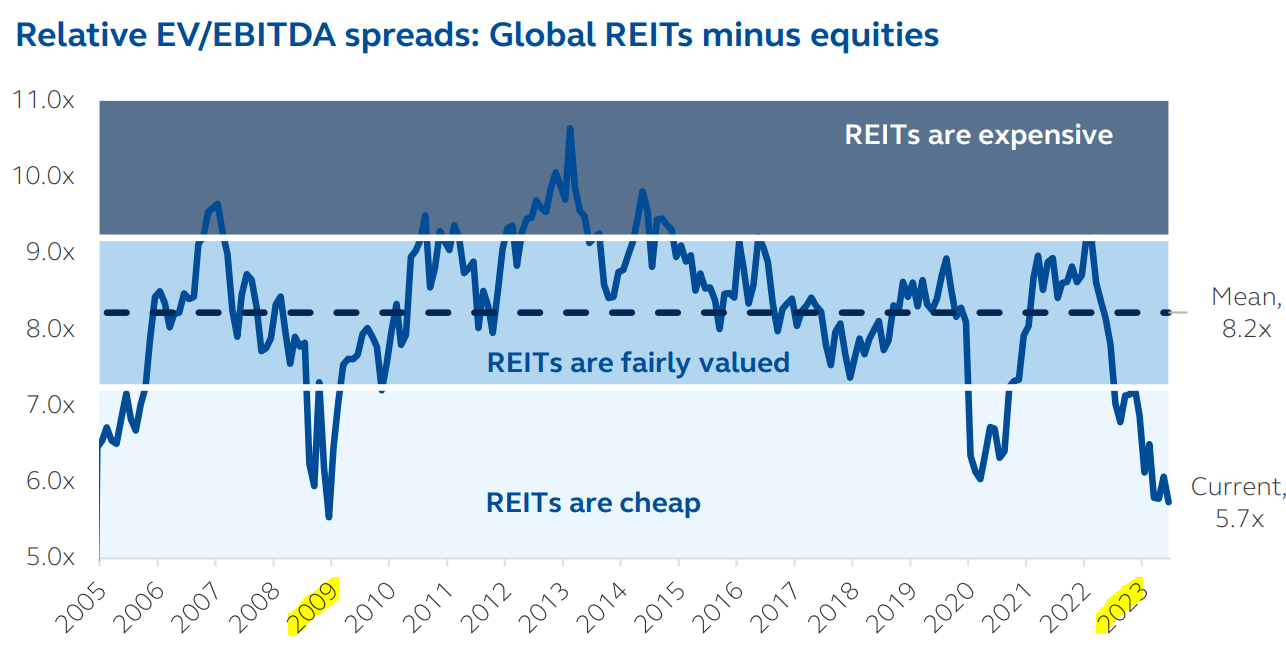

Now increasingly investors are selling REITs at the bottom to buy regular stocks at the top, even as their valuation spreads are the biggest in over a decade:

REITs are cheap 2024

I, of course, think that this is a giant mistake, but maybe I am just biased because I have over half of my net worth invested in REITs at the moment.

But I don’t think so.

I believe that as interest rates return to lower levels, REITs will enjoy an epic recovery, but even if I am wrong and rates remain high, REITs should be well-positioned to deliver strong returns going forward given their low valuations and strong fundamentals.

This was well-explained in a recent Twitter thread from Mr. Market Neutral, who is a fund manager that I follow. When asked how he would invest $10 million today, here is what he answered:

1) 80% REITs with 4.5-5.5% expected portfolio yield, 10% hand picked potential compounders, 10% towards a few managers, venture, and my analysts when they strike out on their own. But the answer would not have been like this prior to 2022. I’ll explain, long tweet ahead:

2) REITs have sold off a bunch with large cap multifamily REITs in the Sunbelt trading in the mid to high 6% cap rate range. Shopping center REITs are also cheap. Self Storage REITs are decent today. They yield on average 4.5-5.5%. That’s $360 to $440k pre-tax.

3) I live in NY, so I assume 40% tax all in. That’s $216-264k all in or $18k to $22k per month. Even thought, I’m in a HCOL, this works for me. Let’s talk about inflation protection and safety. The REITs I have in mind pays out 2/3 of their free cashflow and are 20-40% LTV.

4) Their debt maturities are well laddered and they can raised 10 yr fixed rate unsecured debt at 5% as they did earlier this year. For every $ of dividend they pay out, they have half a $ left over for reinvestments into acquisitions and developments. FCF is after int exp and cap ex. So, you’re not just buying an instrument that yields 4.5-5.5%. You’re actually getting levered FCF in the 6.5% range that will likely grow over time.

5) So there’s a good chunk that is being reinvested into future growth. Combined with real estate’s history of raising rent and beating inflation, I conservatively expect rent growth of 2% which results in 2% FCF growth organically. But remember, they are reinvesting $0.5 for every $ of dividends?

6) That will likely grow distribution by 4% per year which means that you can spent 100% of your dividends and realistically expect your dividends to grow by about 4% to perpetuity. This also means that the stock price should grow by 4% per year as well.

7) 4.5-5.5% distribution + 4% growth = 8.5 to 9.5% total return. IMO, these are conservative assumptions as these REITs that I have identified have historically grown faster and achieved total returns of low to mid teens.

8) What about diversification? What can go wrong. On a look through basis, you own a % of hundreds of buildings for each REIT. So there is no singular tornado or flood that will wipe your cashflow stream. With LTV in the 20-40% range, it’s hard to impair these REITs. Dividend cuts are unlikely as they only pay out 2/3 of FCF.

9) So I go about my life and spend the dividends and take vacations and spend time with my family. I don’t worry about single catastrophic events. Since most of the exposure will be in multifamily, shelter is the most fundamental need of human beings. I don’t worry about obsolescence. AI won’t change this.

10) Since I assume the dividends are ordinary income, I am not playing tricks with depreciation shielding distributions that may have to be paid all at once at some time down the road. If I pick the REITs well, I do not intend to sell them. If I need some cash, I will probably just take out a margin loan up to 20% of my REIT portfolio. This gives me a line of credit for up to $1.6 million on Day 1. REITs do go down, but they have not gone down by 80% even during the GFC.

11) What about interest rate coverage ratio? 6-8x vs 1.25x for most private deal at loan origination. There is no worry of the hand picked REITs not being able to pay dividends. I make this allocation once and just forget about and just don’t care what the stock price trade at. If the stock price goes down by 50%. I may use the dividend to buy more shares if I have excess cash.

12) What is the expected total return? I think that these REITs will generate 15-20% total return in the next 4 years and then it will trade down to a 3.0-3.5% yield and the forward returns will become about 8%. But I will probably still want to own them bc I don’t want to pay taxes. At the moment, people don’t want the REIT exposure. But once the elevated supply gets absorbed, there aren’t a lot of new starts for apartments in the Sunbelt and people keep moving there. I think this becomes a favored asset class soon.

13) I think some cap rate compression makes sense. The private markets are 5.0-5.5% from what we are tracking. The large cap, blue chip apartment REITs are 6.5%. If anything, they should trade at a premium today due to liquidity, platform value, scale, and access to cheap capital.

He thinks that large-cap blue-chip apartment REITs like Camden Property Trust (CPT) will deliver 15-20% average annual total returns going forward.

So you can imagine that smaller and riskier REITs could deliver even greater returns.

But the big question is whether you will have enough patience to actually see these returns, or will you run out of patience and sell two years into a bear market and move onto something else?

You already know my plan.

I will keep buying the dips by reinvesting our dividend income and making small additions to our portfolio each week.

Right now, I have the following two REITs high on my list:

- Healthcare Realty (HR): HR is a healthcare REIT that owns mostly medical office buildings, and it is heavily discounted relative to its net asset value. But the management has a plan. It just recently announced that it is in the process of selling $1 billion worth of assets at a 6.6%, and it is using these proceeds to buy back shares at an 8% implied cap rate to grow its FFO per share and improve its dividend coverage. The management also noted on their most recent conference call that they expect to keep doing more of the same as long as they trade at a steep discount to their NAV to create value for shareholders. We think that this acceleration in transaction activity could be a strong catalyst for HR’s stock and therefore, I am considering buying a bit more of it. Right now, the stock is offering a 7.5% dividend yield and the upside to our fair value target is about 30%.

Healthcare Realty

- First Industrial (FR): Tier 1 industrial REIT have become cheap, and we just recently initiated a new position in First Industrial (FR) for our Core Portfolio. We think that it is one of the best picks in its peer group because it owns mostly Class A properties in rapidly growing, but supply-constrained markets. Importantly, its rents are today deeply below market and the REIT expects to enjoy 30-50% rent bumps as its leases gradually expire. This means that unless its share price rises to higher levels, FR will soon trade at a very low multiple of its cash flow. Already today, its valuation multiple is historically low and therefore, I think that it is likelier that the market will reward FR with a higher share price to keep its multiple from declining to even lower levels. I expect 50% upside in the next 3-4 years as its leases roll over, and you also earn a 3% dividend yield while you wait.

First Industrial

Credit: Source link

{kind=link}