mokee81/iStock via Getty Images

Investment Thesis

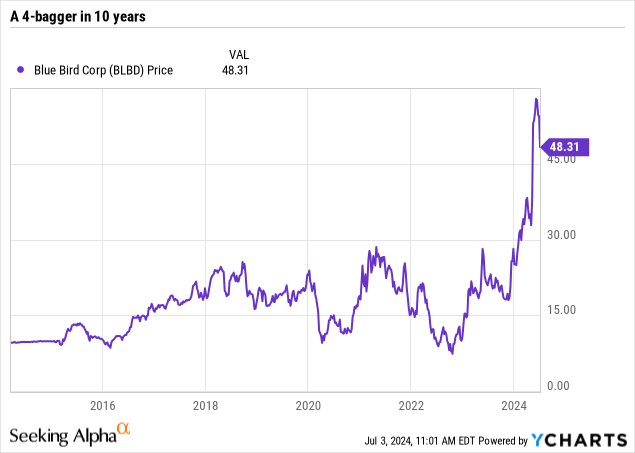

Blue Bird (NASDAQ:BLBD) operates in the not-so-fancy school bus manufacturing industry. A stable, mature sector with high barriers to entry that has been the breeding ground for a 4-bagger in the last 10 years of being listed on the stock market.

Recently, the shares marked a rise of 70% in one month due to a new increase in guidance, and then dropped almost 18%, which brings us to today. The company has two very clear growth catalysts due to the age of school buses and the transition to electric buses, added to a reasonable valuation and strong momentum, makes me think that it still currently a buy.

Industry With Entry Barriers

Blue Bird is dedicated to manufacturing and distributing school buses of all types, which are categorized based on the design and size of the buses.

Although the vast majority of its sales come from the United States (92.5%), it also exports a portion to Canada (7%) and the rest of the world. Although it doesn’t seem like a very fancy business or an exciting industry, it has certain tailwinds and structural advantages what we will discuss.

Blue Bird Investor Presentation

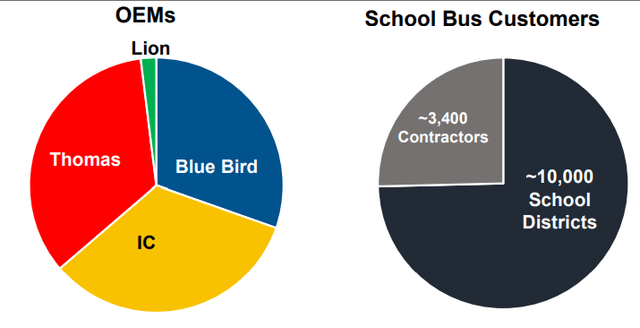

The first peculiarity is that it is a business dominated by a few OEMs, among which Blue Bird stands out as one of the three largest. This is a large competitive advantage because the barriers to entry are high, since it is required to comply with strict industry standards (no one wants their children to go to school on an unsafe bus) and to have developed business relationships with clients. Of each region, which will hardly change suppliers once they have chosen a trusted one.

Other competitors highlighted by the company itself include Lion Electric (NYSE:LEV), Thomas Built, a subsidiary of Daimler Truck (OTCPK:DTRUY), and Navistar International’s IC Bus.

Blue Bird Investor Presentation

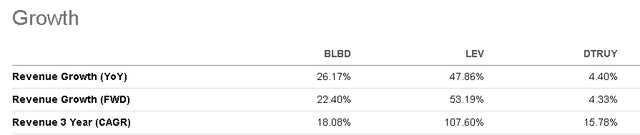

In the long term, this industry typically grows about 5% (this is BLBD’s 10-yr average growth) or only above inflation, because it is a stable, but very mature sector. In that regard, we must highlight the rapid growth that Lion has had in the last three years. This is to be expected considering that it’s the smallest of the four aforementioned, by far, so its comparable growth base is tiny.

Seeking Alpha

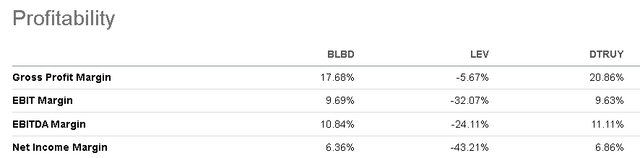

However, Lion’s growth is anything but profitable for now, not even generating gross profit. And although Daimler has higher margins than Blue Bird, it must be remembered that this company isn’t only dedicated to selling school buses, as BLBD does.

Seeking Alpha

Growth Drivers

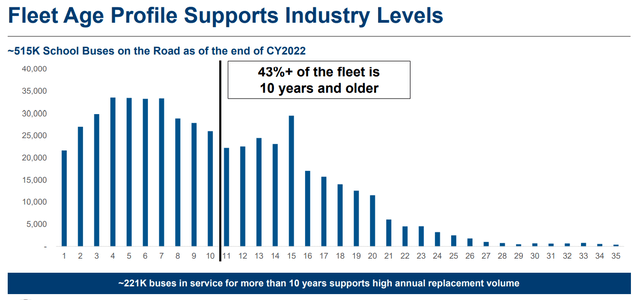

One of the trends causing tailwinds for the school bus industry is the average age of buses. As I mentioned before, it is a fairly mature industry, which is why the buses used today are sometimes many years old. Specifically, the company estimates that more than 40% of the buses are more than 10 years old.

This would represent about 220,000 buses that will need to be changed within a few years. If we consider that the price of a bus is between $60,000 and $150,000, depending on the type and manufacturer, it would represent a potential market of between $13 and $33 billion (BLBD only generated $1.13 billion in revenue in 2023) that would be distributed among a few players. This was calculated by multiplying the 220,000 buses over 10 years old by the average price of a bus.

Blue Bird Investor Presentation

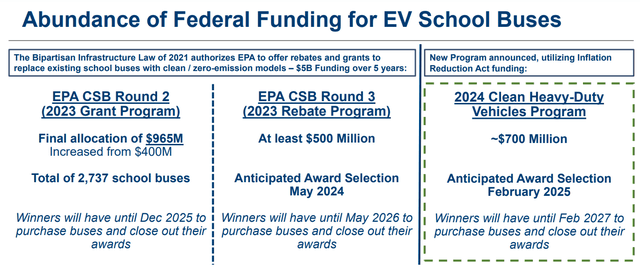

Added to the above, we have the transition towards electric buses, a transition that is not only happening in cars and is directly supported by the government. A new government program of nearly 700 million was recently announced in which it is expected to purchase heavy-duty electric vehicles to continue this transition.

Currently, only 34% of BLBD’s bus sales come from diesel, while the remaining 65% comes from alternative sources such as gasoline, propane or electric, positioning the company well to take advantage of this trend towards electric vehicles.

Blue Bird Investor Presentation

Valuation

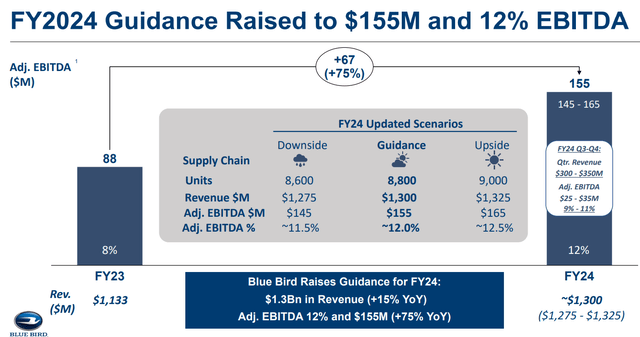

Between May and early June, the company had an increase of more than 70% due to increasing its guidance for FY2024. In my opinion, it wasn’t that big of a deal either, since the increase in the guidance was around 6% in the top line and approximately 14% in the free cash flow compared to the previous guidance and would represent growth of around 15% this year.

In any case, from the beginning of June to date, the company fell about 16%, so it seems worth taking a look at the numbers.

Blue Bird Investor Presentation

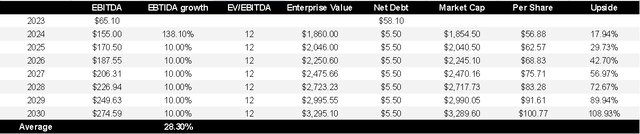

If we take into account the updated FY2024 guidance for EBITDA, of $155 million this year, and apply a multiple of 12 times EV/EBITDA, we would obtain a possible upside for the remainder of the year of almost 18% and 72% in the next five years if EBITDA continues to grow 10% annually, which seems like a reasonable assumption to me. If we make our estimates for this year using the low end of the guidance, the potential upside would be 10% for this year and 60% in the next five years.

I usually look for at least 100% upside in the next five years to consider an investment idea attractive and, in this case, I don’t think Blue Bird is. This doesn’t surprise me at all, since the recent rise in price already discounted much of the expected growth this year.

Valuation model (Author’s Compilation)

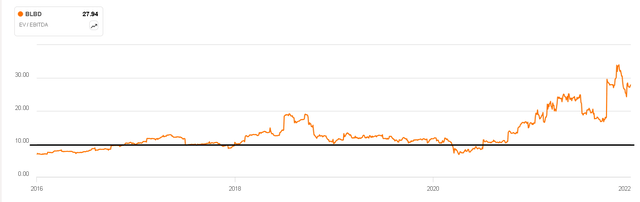

By the way, the choice of the EV/EBITDA multiple was not random, but rather the company between 2016 and 2021 used to trade above 10 times consistently. In 2022 it stopped being profitable in EBITDA and in the last year, it again traded on average at 10-12 times.

Seeking Alpha

What About Momentum?

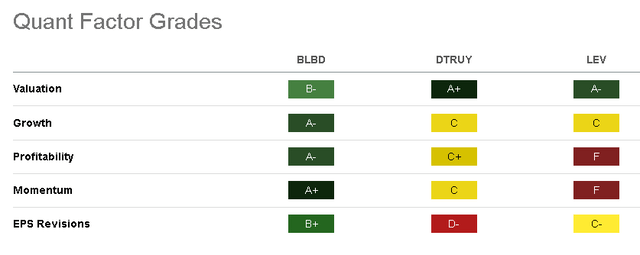

According to Seeking Alpha’s Quant Ratings Factor, the company has very strong momentum because it is trading at a reasonable valuation compared to the industry, with superior growth and profitability. This gives Blue Bird a strong buy rating.

Seeking Alpha

In terms of technical analysis, while the shares could fall close to 18% to get closer to the 200-day Weighted Moving Average (WMA) (blue line in the upper box), the Relative Strength Index (black line in the lower box) tells us that the stock is close to being oversold, therefore the buying force could resume, and it would be a good point to take advantage of the momentum that the company is presenting. As long as it doesn’t fall beyond the WMA 200, I would still view it as a buy.

Trading View

The Bottom Line

In conclusion, good fundamentals combined with powerful momentum make me think that the company is a buy currently. While the valuation could be better, it doesn’t seem to me that we are buying an overvalued company by any means, and the growth opportunity and competitive position of the company is an exciting story to follow closely.

Risks

Although the company currently has strong momentum due to the increase in guidance and the expectation of growing its top line by close to 15%, in the future this growth should stabilize, since I previously commented that this is a mature industry with slow growth. When this happens, the company will probably get a derating. I’m not saying that this will happen “tomorrow”, but it’s clear to me that at some point in the medium term it will happen.

Credit: Source link

{kind=link}