piranka/E+ via Getty Images

W. P. Carey (NYSE:WPC) management seems to be attempting to establish a new normal after a gut-wrenching year. So far, the market is not buying it. Despite that, the argument from the previous article that W. P. Carey is a strong buy remains. The decisions made over the past year are not going to be easily forgotten. But the potential gains from a return to a historical valuation (or maybe better) are still there.

The latest dividend declaration of $.87 per share would appear to be an attempt to get back to a steadily rising dividend. This will succeed if earnings rise accordingly to prevent the rather low dividend coverage that occurred before the dividend was “adjusted downward”. It is a little early to tell how this will work out, but management has clearly begun to start a new record of consistency.

Much of the industry went out of favor due to interest rates. Over the last few articles, there have been arguments to establish that interest rates will remain high for the foreseeable future. Yet rates have declined considerably from their highs. Even if it takes a year or so for the remaining inflation threat to be extinguished, that is still not forever.

But the stock price is another matter entirely.

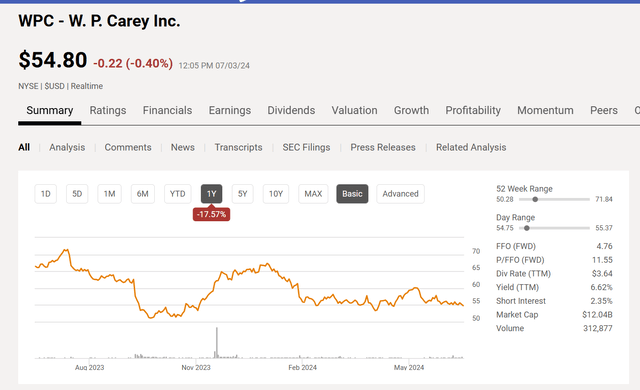

W. P. Carey Common Stock Price History And Key Valuation Measures (Seeking Alpha Website July 3, 2024)

The stock price would appear to indicate a level of pessimism about the future not seen since the pandemic days of 2020. Clearly, prospects were not that bad then and they are likely not that bad now.

But that pessimism and the bad feelings from the dividend cut have led to the current situation. However, that predominance of “bad feelings” likely means that the downside risk is minimal while the recovery potential is substantial.

The company remains with a debt rating of investment grade. That alone is an accomplishment that many in the industry have not achieved, and it also helps to increase the safety of the investment.

First Quarter Earnings

Probably the most important aspect about the first quarter earnings was the positive quarterly comparison. This gets the company back on the growth track after a spinoff and a dividend cut. It begins to reassure the market that the company will resume the consistency it was known for before the last fiscal year.

Of course, it will take a lot more than one quarter. But it is reassuring to investors that the process has begun.

The spinoff and the accompanying sales probably gave the company an unusual amount of liquidity to redeploy. Therefore, the first quarter CEO newsletter likely similarly reassured the market that a return to “business as usual” was the goal of management.

Now let us see if the second quarter report builds on this because first impressions are very important after things like a dividend cut and spinoff.

Whether the redeployment of capital was on favorable enough and significant enough terms to influence the growth rate remains to be seen.

But regaining that consistency reputation is going to be the key to a better stock price in the long-run.

Growth

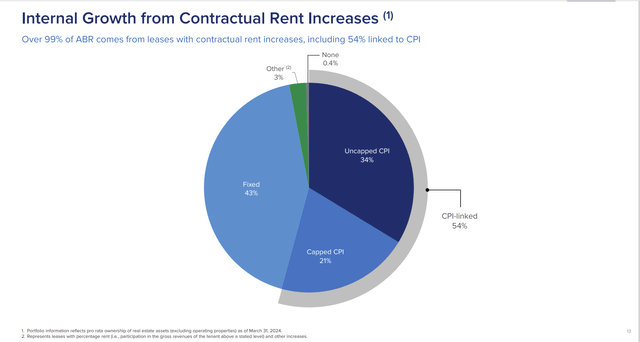

Management has tried to answer the earnings per share, funds flow per share or cash flow per share (many REIT investors watch various funds flow measures) growth by addressing the top line growth with the following slide:

W. P. Carey Existing Business Growth Guidance (W. P. Carey Corporate Presentation First Quarter 2024, Earnings Conference Call Slides)

Clearly, the conservative assumption is that funds flow growth (such as FFO which is often the most important for REITs) from existing business should be something less than the CPI. That probably limits growth to the low single digits.

That growth could be augmented by a significant acquisition that turns out to be accretive. Long-term, that could add a percentage point or maybe even a few percentage points to the average growth rate.

Any growth (including FFO and other common REIT measures) will likely be at a minimum from the contracts of the existing business that would appear to be something less than the consumer price index.

Augmenting that growth rate would be a combination of lease expirations, new business, and some property sales or acquisitions that would likely occur on an opportunistic basis.

Offsetting this consideration is the relatively high dividend yield at the current time of nearly 7%. That figure is nearly what most investors report for a long-term total return. Therefore, any growth would mean that the return on this investment grade idea is above average. Should the valuation expand back to historical levels, that would be icing on the cake. That expansion possibility provides for a lot of icing too.

Exactly what is realized in the form of a total return would depend upon the business conditions seen by the investor roughly five years out. It would appear that a total return in the low teens should be probable over the long term for a buy-and-hold investor.

Debt

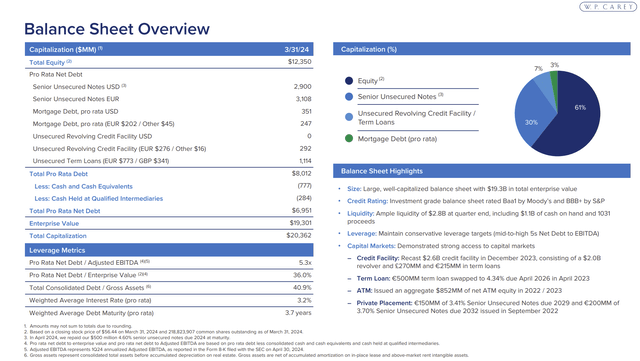

Generally, any company with investment grade rated debt will not have refinancing issues if that is the chosen route. Since it is highly likely that management will return to growing the business, it is also highly likely that debt will not be repaid. Instead, debt will be rolled over when it comes due.

W. P. Carey Debt Summary And Enterprise ValueW. P. Carey Debt Summary And Enterprise Value (W. P. Carey Corporate Presentation First Quarter 2024, Earnings Conference Call Slides)

It would take several years of higher long-term interest rates to make a sizable difference in the company outlook. But at least some of those higher rates would be offset by the increase in contracted rent (as shown before).

On the other hand, should interest rates decline in the long-term as has been the case in the recent past, this company would benefit by refinancing at lower rates.

Companies can also take advantage of interest rates by short-term refinancing when conditions are unfavorable or long-term refinancing when conditions become more favorable. It is also possible to increase equity participation during times of unfavorable financing through joint ventures. That gives this company a number of ways to survive hostile industry conditions.

The investment grade rating likely means the company has access to the debt market as needed. That gives management considerable financing flexibility.

Conclusion

W. P. Carey interrupted a long record of dividend increases with a dividend cut and a spinoff. That upset investors that were willing to pay a premium for what was considered an above average record. Those same investors will likely continue to punish the company for its transgression of cutting the dividend for an indeterminate amount of time into the future.

However, if the company manages to establish a track record of consistency again, then current investors not only benefit from the relatively high yield, but they will also benefit from the establishment of another track record that would likely cause investors to again value the stock at higher levels. Over the long run, that should be a combined return in the teens.

The first quarter report was important to establish a beginning record after the dividend cut and spinoff. I believe much of this fiscal year will establish that management, as usual, gave some decent and reliable guidance.

The fact that the stock was punished for the dividend cut limits downside risk. Meanwhile, recovery risk is there to give an asymmetric return that favors the upside. If management grows the business as planned, then the asymmetric return is an even better bet.

The actual future value of the stock will depend upon business conditions 5 years out. That can be murky. But it is very likely that management will likely re-establish a pattern of business and dividend growth. That would enable an investor to wait for favorable conditions upon which to potentially sell the stock.

Risks

Any growth record can come to an end at any time. Companies can only grow so large as any industry is a finite size and each company in it is likely limited by the abilities of management to grow and run the company. There is always a risk to paying for a good track record that can come to an end at any time. But that never seems to stop Mr. Market from becoming over enthused about a good record (as if it will go on forever because it seemingly has in the past).

The article assumes continuing (if irregular) inflation declines. Should that prove to be inaccurate, rising inflation could change the outlook of the company considerably.

The loss of key personnel could have a material effect on the outlook of the company’s future.

Credit: Source link

{kind=link}