Timon Schneider

Investment Thesis

We used to be invested in Dynagas LNG Partners (NYSE:DLNG). Our positive thesis then was based on the company’s long-term charters and the niche they had with their vessels which enabled them to pass through the northern route from the Russian Arctic to Asia in the summer months, cutting the sailing time.

DLNG vessel in the Arctic Ocean (DLNG Q1 2024 Presentation)

It is almost two years since we wrote our Sell analysis on DLNG. We explained why we believed it was becoming less and less interesting to invest in this company.

Seeking Alpha reached out to us and asked if we could share our more recent view on the company’s prospects and what our stance was now.

Let us start by looking at their most recent financial results

DLNG First Quarter 2024 Financial Results

We want to remind our readers why we did take a position in DLNG some years ago. Their entire fleet had long-term charters with fixed rates, not index-linked. That is generally the kind of shipping companies we like to invest in. It eliminates the uncertainties of the spot market, which in most shipping sectors causes booms and busts.

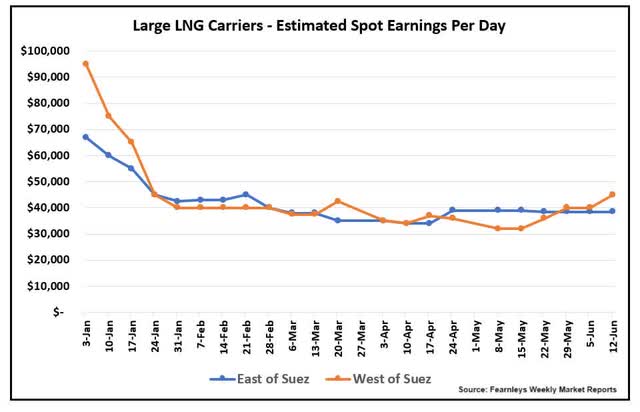

Spot rates for LNG carriers have not been good so far this year.

Large LNG carriers spot rates in 2024 (Data from Fearnleys Shipbrokers. Graph by author)

However, with DLNG’s 100% utilization of their fleet in Q1, they managed to earn a strong average of $72,770 per day per vessel. This is an improvement of approximately $10,000 per day per vessel Y-o-Y.

The adjusted EPS in Q1 came in at $0.25, after taking into account payments on the two series of preferred shares (DLNG.PR.A) and (DLNG.PR.B).

The A-series units are presently yielding 8.9% and the B-series are yielding 9.6%.

Those familiar with DLNG know that they were barred by their banks from paying any dividends on the common units. No dividend has been paid on those since the 2nd of May 2019 which was the last payment of 6 US cents per unit.

In terms of cash flow, DLNG did generate net cash from operation of $11.6 million in Q1. That was 15.3% lower Y-o-Y due to a change in working capital held. This net cash works out to $0.32 per share.

Let us look at their balance sheet. It was the high debt they had earlier that caused the lenders to force DLNG to eliminate dividends on the common units.

Of the outstanding credit facility of $675 million which was due for payment in September this year, the balance outstanding was $408.6 million as of 31st March 2024.

Debt profile and financial lease arrangement (DLNG Q1 2024 Presentation)

To refinance the credit facility, DLNG will make full payment using cash liquidity and proceeds from the sale of four of their vessels for $345 million to a Chinese leasing company called China Development Bank Financial Leasing Co. Ltd. These four vessels are bareboat chartered back to DLNG.

Two of the vessels are chartered for 5 years, and the other two for 10 years. After these charters expire, DLNG has a purchase obligation to buy back the vessels for 20% and 15% of the financing amount.

Focus on the fundamentals

Supply and demand dynamics always dictate how much a seller can achieve.

Short-term market rumors, combined with greed and fear can push the market in the short run, but in the end, cargo owners know how to drive a bargain if there simply are too many ships fighting for the same cargo.

Two years ago, we were concerned about talks of large orders of newbuildings of LNG carriers.

The lower rates we have seen so far this year, is in our opinion, a prelude to what is to come. In an article in early May this year, Riviera reaffirmed our concern about the large number of LNG carriers that will enter the market this year and the next. According to them, the number of large LNG carriers scheduled to hit the water next year could be as many as there are presently on the water. That is based on large LNG carriers which were built between 1990 and 2005.

That is a doubling of the fleet.

A “normal” order book with 5 to 10% of newbuildings is possible to absorb with a modest growth in cargo volumes and attrition of older vessels.

However, those shipowners that have committed billions of dollars to build these new LNG carriers, have done so under the premise that the demand for seaborne LNG is going to grow explosively.

Cheniere Energy, earlier this year projected that China, which now has become the world’s largest importer of LNG, could potentially double its imports in the next ten to fifteen years’ time.

Last year, China imported 71.3 million tons, which was 12.6% higher Y-o-Y.

Natural gas is always going to be an intermediate solution towards the global move to decarbonize. If we look at how rapidly China is shifting its source of energy for power generation into renewable energy, we could see peak natural gas come earlier than what some believe.

Conclusion

The positive takeaway is DLNG’s long-term charter arrangements. With an average balance duration of charters of their vessels of 6.6 years, their total backlog as of the end of Q1 was $1.07 billion.

This, in combination with having paid down a substantial part of their debt, does make their financial position quite good.

On a more negative note, we are concerned about the oversupply of vessels.

When will a dividend be reinstated?

Based on the $0.23 per share free cash flow in Q1, there is a chance that management will decide to return to paying owners of the ordinary units a dividend.

Without any capital return to shareholders, DLNG is less interesting than many other shipping companies.

During the Q1 conference call, only one analyst had any question. It was Ben Nolan from Stifel. He raised the question again, as he had also done at the previous quarterly call, on whether DLNG had any plans to return capital to common unit shareholders through dividend payments. Again, management was hesitant to commit or comment.

We believe they might start paying a dividend later this year, but it will most likely be a low amount of 6 to 8 cents per unit, as we believe their priority going forward will be to add more fuel-economic vessels to their fleet. These will come from their sponsor Dynacom.

One reason we will not invest in DLNG at this moment is based on our ethical view.

We do not want to support Russian companies in fueling the financial cost of the war between Russia and Ukraine. We hope that peace can come soon. But even when after peace has been reached, we believe it is going to take a long time before international trust in Russia is restored.

As such, we continue our Sell stance on DLNG.

Credit: Source link

{kind=link}