Cristi Croitoru

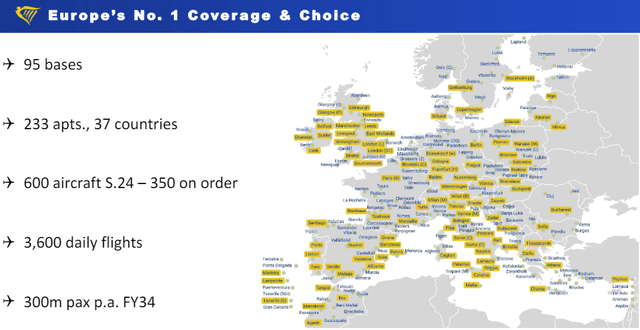

Following our early January update called Bullish Long-Term Story, Ryanair (NASDAQ:RYAAY) reported its full-year results and paid its first dividend. The company started its operations in 1985 and became a low-cost player in the early 1990s. Its business model is based on the low-cost principles pioneered by the US company Southwest. Currently, the company is the largest airline in Europe, carrying more than 180 million passengers per year, with a fleet of almost 600 planes.

Ryanair in a Snap

Source: Ryanair Fiscal Year 2024 Results

Our long-standing buy rating was supported by a unique cost basis with a clear upside compared to peers. This is backed by Ryanair’s Gamechanger Strategy: ‘more seats, less fuel consumption, higher capacity loads, lower tariffs, and consequently more customers that equal more profit.’ In addition, the company secured a contract with Boeing to purchase 300 aircraft and is now Equipped For A Decade Of Growth. Here at the Lab, we believe Ryanair will be able to deliver long-term returns; however, since our update, the company’s stock price has decreased by 7.88%. That said, following the FY analyst call, we decided to lower our estimates on a 12-month view based on more muted pricing activities in the summer of 2024. This is mainly based on a lower conviction level in the face of clients’ concerns over pricing. While our revised €20 target price still implies a 22% potential upside, we maintain a buy rating estimate.

Ryanair Rating Update

What has changed now?

- (A softer pricing environment). During the Fiscal Year 2024 results conference call, by CEO Michael O’Leary’s own admission, the company is cautiously optimistic that peak summer 2024 fares will likely be flat to modestly ahead compared to last summer. This happened after two consecutive years of very material fare increases. In addition, following statements from package holiday operators, summer trends have been disappointing. The increasing regularity of low-cost carrier fare sales in email inboxes also supports this. Looking at the past two years of travel spending (with almost no budget) to make trips after the COVID-19 outbreak, consumers are pushing back to further inflation plus price increases. For this reason, here at the Lab, we are slightly lowering our Q3 estimates. There is some degree of consumer resistance to priced in;

- (No capacity constraints) Here at the Lab, we believe this lower trend is not due to capacity constraints. We are still below the pre-COVID-19 level. Having said that, we still forecast low-single-digit capacity growth for our favorite low-cost operator;

- (Non-fuel costs stubbornly inflate). On a cost basis, we now forecast another year of mid-to-high-single digit non-fuel unit cost. Due to the CAPEX delay from 737 MAX aircraft, the company is in a suboptimal cost structure, given that it continues to restore staff. Our team sees this as a transitionary trend; however, it impacts the current margin. Without considering the fuel hedging strategy, Ryanair’s yield needs a step-up to avoid margin contraction, but we believe there is no space for improvements;

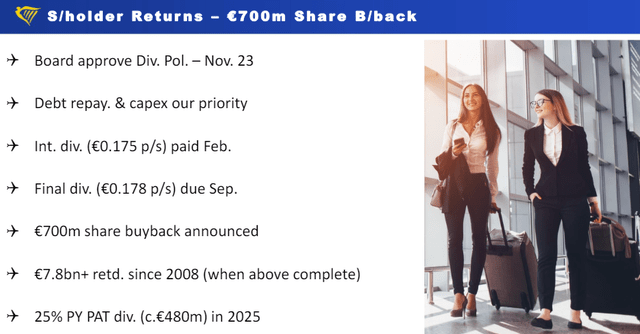

- (Higher CAPEX and lower profit diminish the potential for excess returns). We are reducing our net cash projection by considering a higher shareholder remuneration with a buyback of €700 million and a dividend payment (projected for a final DPS in September of €0.178 – Fig 1). Looking back at Ryanair’s original guidance, investment CAPEX was estimated at €2.8 billion in 2024 and €1.3 billion in 2025. However, the company only invested €2.4 billion, with €400 million now estimated for 2025. That said, the low-cost operator now anticipated €2.3 billion in CAPEX guidance, and there is an extra €600 million from somewhere. Given an inferior EBITDA outlook, our March 2025 net cash estimate was reduced to €1 billion. This might imply a more muted shareholders’ return for the following year. As a reminder, the company has a total dividend payment of €480 million, which aligns with the 25% payout ratio dividend policy.

Ryanair CAPEX and Payout Evolution

Source: Ryanair FY 2024 Results – Fig 1

Earnings Changes and Valuation

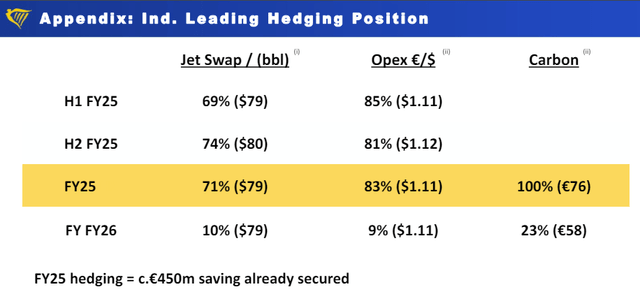

Post results, in May, Ryanair also released traffic growth of 11% with a load factor of 95%. This was one basis point above last year’s results, with confidence for a positive customer response to the lower fares. Starting with the revenue line, we adjusted Ryanair forecasts to reflect a more cautious pricing view. We lowered pricing from -1% in Q1 and by -5% in Q2. In our estimates, we now arrived at sales of €14.6 billion from €14.9 billion. In Q1, we forecast top-line sales of €3.8bn with a core operating profit of €540 million. In addition, the company now guides for a modest rise in unit costs due to rising labor expenses. Higher interest income and fuel savings partially offset Boeing delivery delays and submittal staff. In addition, the company has hedged almost 70% of fuel requirements at $80 per barrel (Fig 2). Ex-fuel, our unit costs forecast increased by +0.5% every year. Therefore, lower pricing power (still supported by small capacity growth) and higher costs led to a change in our EBITDA projections that moved from €3.49 billion to €3.15 billion. As reported above, there is also a higher CAPEX expectation with €600 million in additional investments. Our EBIT margin is now set at 13.35%, resulting in €1.95 billion. Considering a positive net cash and a higher interest rate environment, our adjusted net income reached €1.87 billion with an EPS of €2. Our previous estimates was set at €2.15. The net impact on 2025 EPS is a downgrade of 7%.

Ryanair hedging strategy

Fig 2

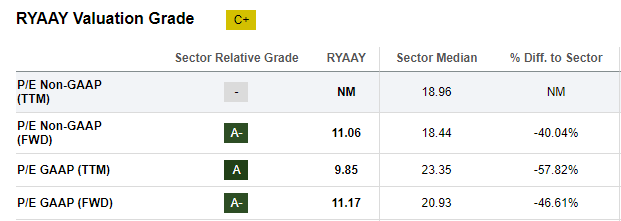

Our team believes the company should be the mid-term industry short-haul winner. Despite that, the company is not immune to a consumer slowdown due to persistent inflation and prolonged higher interest rates. Higher uncertainty results in a new €20 price target ($140 in ADR) based on an unchanged P/E target of 10x with an EPS of €2. Ryanair valuation is also aligned with its historical average (Fig 3).

Ryanair SA Valuation

Fig 3

Risks

Key downside risks include 1) higher competition from Wizz and EasyJet, 2) delay in B737 MAX aircraft with a mismatched in additional wage payment for new staff, 3) volatility in fuel prices (even if the company has a clear strategy for hedging), 4) lower consumer demand, 5) and significant event associated primarily with nature actions and terrorist attack.

Conclusion

Here at the Lab, we still believe in Ryanair’s long-term earnings projection. A combination of lower net cash, higher CAPEX in 2025, and pricing pressure from clients slightly changed our buy rating target price. That said, our positive forward-thinking is confirmed.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Credit: Source link

{kind=link}