Oselote

Investment Thesis

Super Micro Computer (NASDAQ:NASDAQ:SMCI) is a key player in the server systems market. Over 90% of its total revenue comes from server and storage systems. The revenue mix from this segment has increased from 79% of the total in FY2020 to 92% in FY2023. The massive spending on AI infrastructure due to the GenAI boom is expected to create a strong growth tailwind for the server market, which will significantly benefit SMCI. The stock has jumped nearly 190% YTD, reflecting this growth optimism. I believe its 200% YoY revenue growth in the last quarter justifies this rally. Additionally, the current EV/Sales forward of 3.2x and non-GAAP P/E forward of 34.8x indicate that the stock is not trading at lofty multiples compared to semi peers. Therefore, I’m initiating a buy rating on the stock, as the company is significantly boosting its capex to maintain a strong growth trajectory in the long term.

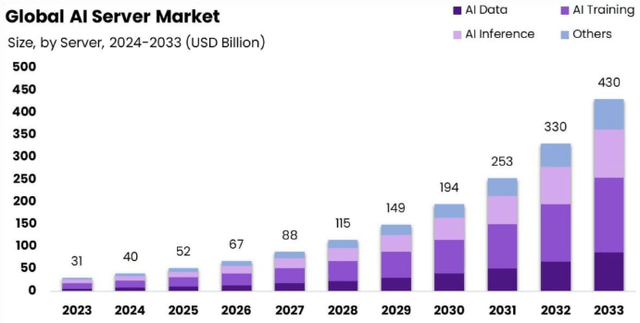

AI Server Market Is Booming

Market.us

First of all, let’s analyze SMCI using a top-down approach. It’s crucial to evaluate the market’s growth outlook, as most of the company’s revenue comes from server market spending. According to market.us, AI server market spending grew by 29% in 2024 and is expected to continue with a CAGR of 30.3% from 2024 to 2033, reaching $430 billion. As shown in the chart, server spending growth will start accelerating this year. Most enterprises are expected to increase investment in data center infrastructure, including AI servers.

In the 3Q FY2024 earnings call, the management has highlighted that the company’s rapid business growth requires scaling up their capacity. The company is expected to acquire additional warehouses to support the next phase of enterprise and data center operations. Currently, they are on track to produce over 2,000 liquid cooling DLC racks per month for AI servers, with production volumes steadily rising. In addition, they are also delivering more than 1,000 racks of NVIDIA (NVDA) HGX AI supercomputers and continue to extend their partnerships. Therefore, due to the AI growth tailwind, I believe SMCI’s growth inflection is imminent, as supported by recent stock actions.

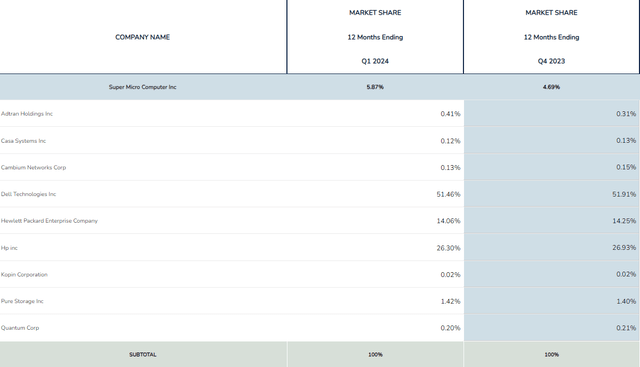

SMCI is Gaining Market Share

CSIMarket

As we can see from the table, SMCI’s market share has expanded from 4.69% in Q4 FY2023 to 5.87% in Q1 FY2024. While this number is not as significant as the market share of the top three server venders, it presents a tremendous opportunity for SMCI to further expand its market share. Notably, the market shares of the top three server providers have slightly decreased since Q4 FY2023 TTM. However, prioritizing market share gains will come at a cost. Its R&D (excluding SBC) increased by 32% YoY, and total capex in 9M FY2024 has tripled on a YoY basis, significantly impacting its FCF. But I believe this is the right move, which I’ll explain in a later section.

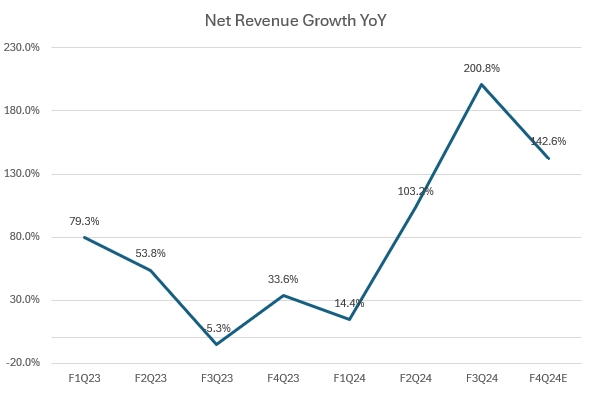

+100% Revenue Momentum Continues

The company model

Looking at the chart, we can see that SMCI’s revenue growth has significantly rebounded starting from 2Q FY2024, maintaining over 100% YoY growth in the last two quarters due to robust demand for AI compute. Although 3Q FY2024 revenue did not meet consensus expectations due to supply chain challenges regarding Direct Liquid Cooling-related components, the company remains optimistic about its revenue outlook as those challenges will gradually improve in the coming quarters. They have raised their guidance from a range of $14.3 billion to $14.7 billion to a new range of $14.7 billion to $15.1 billion. The midpoint of this new guidance implies a 142.6% YoY growth in 4Q FY2024, which is expected to bring FY2024 growth to 110% YoY, a significant increase from the 37.1% YoY growth in FY2023. I believe this tremendous growth reacceleration deserves a higher valuation multiple. Particularly, the demand for AI servers in the next decade is expected to be significantly higher.

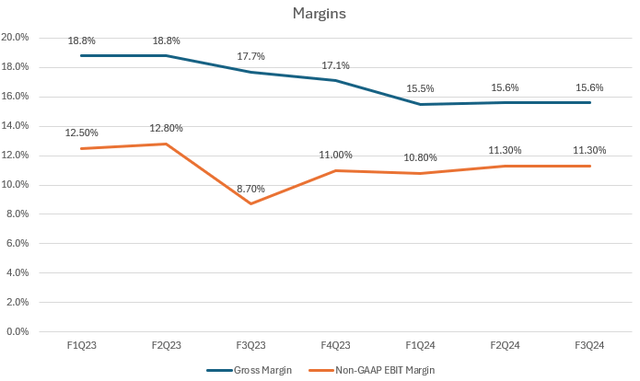

Prioritizing Growth Over Margins

The company model

Like other hyper-growth companies, SMCI is currently prioritizing top-line growth and boosting demand while sacrificing margins, as management expects gross margins to decrease sequentially. I’m not surprised by the company’s trade-off between near-term profitability and long-term growth potential, especially in maintaining market share within this highly competitive industry. Both its gross margin and operating margin have been declining since 1Q FY2023. The company’s margins were flat in the last quarter, indicating that earnings growth was entirely driven by its top-line growth rather than operating efficiency.

The company model

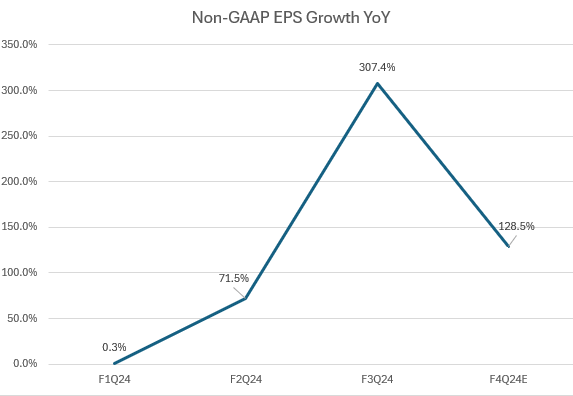

Additionally, the company achieved 307.4% YoY growth in non-GAAP EPS in 3Q FY2024. It’s important to note that the strong beat on EPS was largely driven by a $20 million tax benefit. For 4Q FY2024, the company guided a midpoint non-GAAP EPS of $8.02, which is above the market consensus. This implies a significant 128.5% YoY growth. I believe the stock’s P/E multiple will largely come down due to the robust EPS growth outlook.

Valuation

Seeking Alpha

The stock is currently trading at a premium valuation, reflecting a strong growth outlook. Its P/E GAAP TTM is 46.9x, but the multiple is expected to come down significantly to 34.8x on a non-GAAP forward basis. The P/E is almost in-line with the semi sector index (SOXX).

I believe that its historical averages are not directly comparable, as previous multiples did not factor in the robust growth potential from the GenAI boom. Given the company’s primary focus on revenue growth, let’s consider its EV/Sales Fwd, currently at 3.23x, just 10% above its sector median according to Seeking Alpha.

However, there is a catch. Despite the strong AI tailwind, I believe the overall U.S. stock market has been trading at an expensive level, making SMCI’s valuation appear reasonable on a relative basis. Nonetheless, the stock may experience consolidation following a 170% rally this year.

Conclusion

In conclusion, SMCI is a major player in the server systems market. The increasing investment in AI infrastructure due to the GenAI boom is expected to drive further growth. The recent stock move reflects this optimism, supported by the company’s 200% YoY top-line growth. We notice that the company is gaining market share, and its robust revenue growth outlook justifies a higher valuation multiple. Although the company’s margins have been decreasing as it prioritizes growth over profitability, the strong demand for AI servers and the company’s optimistic revenue guidance suggest continued above-trend growth. Despite this, the stock’s P/E is almost in-line with semi-index multiple and appears reasonable given broader market conditions. Therefore, I think SMCI is a buy.

Credit: Source link

{kind=link}