Nemes Laszlo/iStock via Getty Images

Arcellx’s Anito-cel: A Promising Contender in Multiple Myeloma Therapy

Arcellx (NASDAQ:ACLX) is developing cell therapies for multiple myeloma [MM], acute myeloid leukemia, and myelodysplastic syndrome. Anito-cel (formerly CART-ddBCMA), the company’s flagship product, is being developed in a Phase 2 pivotal trial for relapsed or refractory MM (rrMM). My last article on Arcellx was in September, a month after the FDA lifted the partial clinical hold (limits some trial aspects) on their T-cell therapy for rrMM, Anito-cel. The partial hold came after a patient died in the pivotal Phase 2 iMMagine-1 clinical trial. The death was reportedly and unfortunately due to a deviation in trial protocol that treated a patient who should have been ineligible. I concluded that their efforts in rrMM are “potentially groundbreaking” and recommended a speculative buy on ACLX. Its stock is up 45% since the recommendation, while the S&P 500 is up 22%.

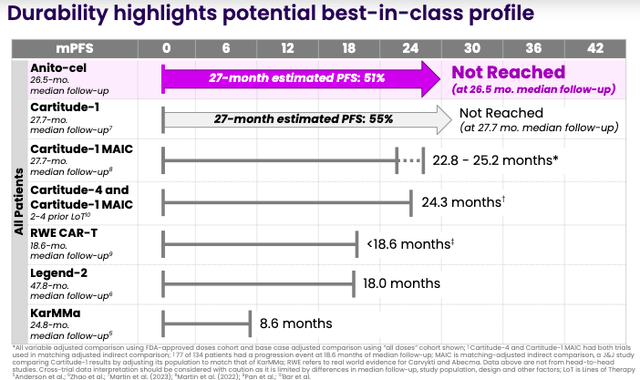

In December, Arcellx presented Phase 1 data on Anito-cel in patients with rrMM at the American Society of Hematology [ASH] Annual Meeting. The data, focused on results from at least one year of follow-up in patients with poor prognostic factors, was encouraging. In 38 evaluable patients with a median follow-up of 22 months, the overall response rate [ORR] was 100%. 76% of patients achieved a complete response [CR]. To review, per RECIST criteria, the ORR is the sum of partial (at least a 30% decrease in the sum of the LD of target lesions) and CRs. CRs indicate the disappearance of all target lesions. Moreover, progression-free survival [PFS] was 67.5% at 18 months (and 84.6% for the patients that achieved a CR).

Kite, a division of Gilead Sciences (GILD), expanded their collaboration with Arcellx, centered around Anito-cel, to include studies in lymphoma. Gilead paid an upfront cash payment of $85 million and acquired $200 million of Arcellx’s stock at a price of $61.68 per share as part of the expanded collaboration.

In May, the two shared the design of the planned global Phase 3 trial, iMMagine-3, testing Anito-cel against the standard of care in patients with rrMM. This will target earlier lines than assessed in iMMagine-1. Moreover, they also stated that preliminary data from the iMMagine-1 trial is expected by the end of the year.

Arcellx anticipates Anito-cel’s launch in 2026 and believes it has the potential to be “best in class” and disrupt the rrMM market.

Arcellx

Anito-cel would not be the first CAR-T to enter the $20 billion-plus MM market. Johnson & Johnson’s (JNJ) and Legend’s (LEGN) Carvykti already netted $500 million in revenue last year, despite being approved in 2022. I discussed Carvykti, along with the other CAR-T in the MM market, Abecma, marketed by 2seventy bio (TSVT) and Bristol-Myers Squibb (BMY), in another recent article.

Anito-cel is thought to be differentiated from the other two CAR-T products because of its novel “D-Domain attributes” that are proposed to facilitate “high transduction efficiency, CAR positivity, and CAR density on the T-cell surface.” In other words, Anito-cel requires lower overall cell dosing than other CAR-T products, which the company points out is “a key risk factor for both severe CRS and severe neurological toxicities.” If this is, in fact, the case, Anito-cel could become the favored CAR-T in MM. For context, per Johnson & Johnson’s CFO, Carvykti is projected to secure at least $5 billion in peak annual revenue.

Financial Health

Arcellx reported $691 million in cash and cash equivalents, as well as marketable securities, as of March 31. They have $779.69 million in total assets and $283.122 million in total liabilities. Arcellx does record revenue from their collaborations. Q1 revenue amounted to $39.256 million. Expenses for R&D and G&A came to $32.3 million and $22.7 million, respectively. Q1’s net loss amounted to $7.198 million. As ACLX’s share count increased from about 46 million to about 52 million, there was a noticeable dilution, which is normal for a biotech in the clinical stages. Arcellx believes their cash is sufficient to fund its operations into 2027.

Risk/Reward Analysis and Investment Recommendation

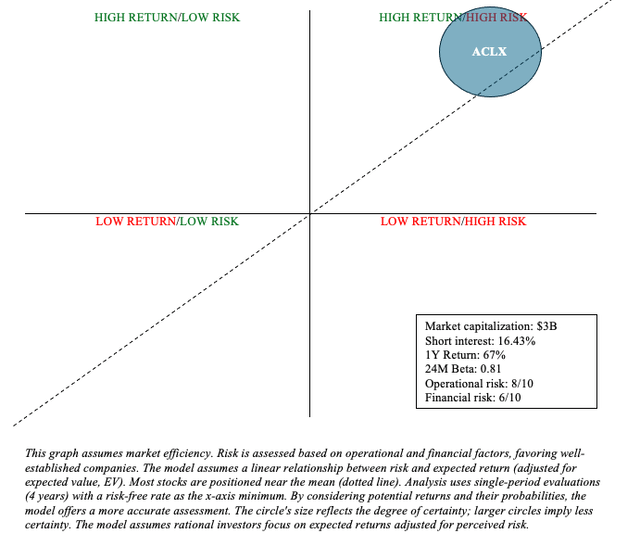

In terms of risk and reward, Arcellx’s early-stage data in MM is encouraging and bodes well for its differentiated CAR-T product, Anito-cel. Their collaboration with Kite (Gilead) mitigates some operational (e.g., manufacturing, marketing, etc.) and financial risk (e.g., collaboration revenue to offset development costs). Arcellx, with a market capitalization of $3 billion, appears undervalued given the size of the opportunity ahead and Anito-cel’s data to date.

Author

ACLX is very much a Quadrant 1 stock and should be of interest to a biotech-focused investor with a barbell portfolio strategy where one allocates the majority of their funds to low-risk assets, like Treasuries and broad market ETFs, with a small portion dedicated to high-risk/high-reward investments like ACLX. The recent events certainly justify keeping ACLX as a buy. Anito-cel has the potential to be a multibillion-dollar biologic in the lucrative MM market, and Gilead has expressed interest in it.

Nonetheless, one must be aware of some significant risks. For starters, CAR-T is a dynamic and complicated product. For example, in April, the FDA required CAR-T products, like Carvykti, to include a boxed warning for T cell malignancies. So, there may be perceived safety issues among providers and patients that limit CAR-T in general. Moreover, Anito-cel will face competition from other CAR-T products and if it fails to provide obvious differentiation, it is unlikely to secure a sizable portion of the market. Second, it remains to be seen if Anito-cel’s clinical benefits in endpoints like CR and PFS will appease regulatory authorities. CAR-T products have had a challenging time achieving statistical significance in a key cancer endpoint, overall survival. Moreover, Anito-cel still has major clinical barriers to overcome prior to regulatory consideration (phases 2 and 3). Finally, competitor advancements or shifts in treatment paradigms could affect Anito-cel’s uptake.

Credit: Source link

{kind=link}