buzbuzzer/iStock via Getty Images

Global Medical REIT Inc. (NYSE:GMRE), incorporated in 2011 and headquartered in Bethesda, MD, mainly owns and manages net-lease off-campus medical office buildings across the country.

This stock represents a very good opportunity for those looking for high-income generation but also for those who are looking for double-digit total returns. The dividend is more sustainable than you may think because of the prudent investments made by the management and the income stability of the portfolio. Though I don’t see a lot of fundamental growth potential here, the shares are severely undervalued and I think it’s a matter of time before the market realizes the discrepancy and corrects it.

The Dividend Yield Is Sustainable

GMRE currently pays a quarterly dividend of $0.21 per share, resulting in a forward yield of 9.53%.

From one point of view, the market is reasonable to drive it so high when the payout ratio is 92.3%. While REITs like Global Medical enjoy long-term leases that make for predictable income which makes for a stable ratio, it goes without saying that a lot of income investors are interested in REITs for their attractive yields which are often well-covered by cash flows; the margin of safety presented here is too narrow for such defensive investors.

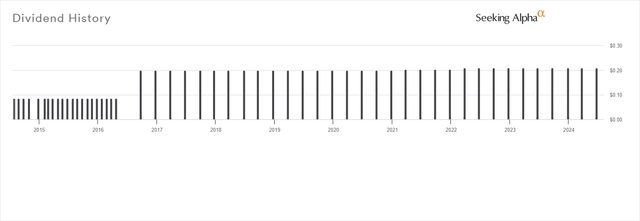

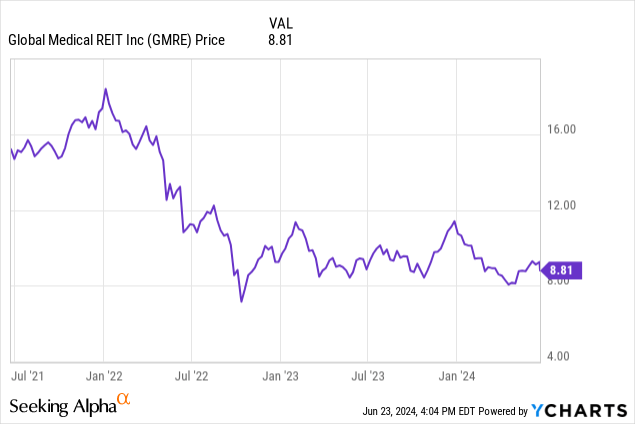

On the other hand, this REIT has been very consistent with its distributions for a long time:

Seeking Alpha

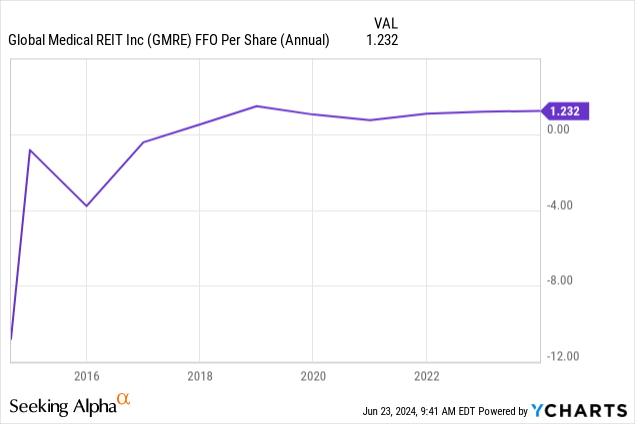

On top of that, management has been paying a quarterly dividend since the IPO in 2016, even though FFO was negative back then:

So, while the relatively flat FFO per share in the last couple of years doesn’t inspire confidence, this REIT went from negative to positive cash flow and now it appears to have been stabilized.

Slow But Stable Income Generation

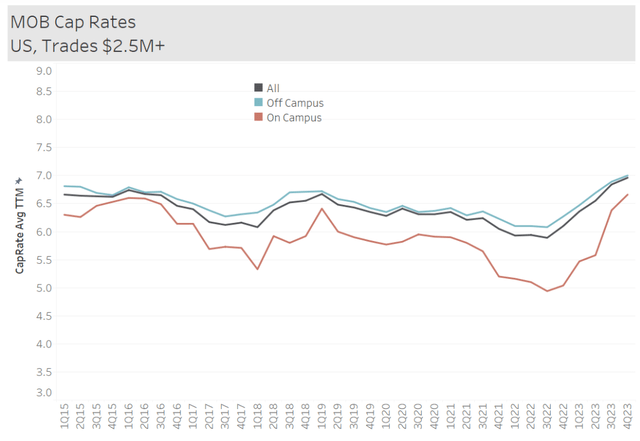

Now, based on the latest investor presentation, Global Medical has invested a total of $1.4 billion in real estate assets and acquisitions have been made at a weighted average cap rate of 7.9%, which is what management has stated they are looking for. In the past, off-campus medical office building cap rates haven’t been sold for more than a 7% rate:

revistamed.com

Sure, the spread is more narrow today, but my point is that managers have established they have an eye for bargains and their attempts to provide value to shareholders have been successful so far.

That provides important context for the operating performance, which doesn’t appear to be very promising so far. Here are the changes between the relevant average figures from the past 3 fiscal years and the last quarter’s ones annualized:

| Rental Revenue Δ | 6.83% |

| Cash NOI Δ | 2.06% |

| AFFO/Share Δ | -2.82% |

What the most recent results reflect is stability here. The same goes for when comparing them to the 1Q23 ones. Total revenue decreased by 3% on a YoY basis, but that was because of the impact some dispositions had. And since expenses are likely to be stable going forward, I don’t see a considerable threat to the predictability of revenue; interest expenses decreased from $8.3 million in 1Q23 to $6.9 million in 1Q24, operating expenses were $7.4 million versus $7.5 million in the same quarter a year ago, and G&A were $4.4 million compared to $3.8 million in the first quarter of the previous year, but management expects them to be in the range of $4.4 million to $4.6 million per quarter for this year. Last, AFFO was a bit higher at $16.5 million, marking a $500K YoY increase. In the last earnings call, management also noted that they are trending towards a retention rate of 76% based on the 2024 upcoming lease expirations and past renewals.

I believe that the business can grow and improve its operating performance over time, but it will likely be a slow process. First, there is currently not much liquidity available for growth based on 1) low retained earnings, 2) low equity price, 3) no intent to dispose of many assets, and 4) not much room for higher leverage. In regard to the second point, the price is too low relative to NAV, so I think new offerings won’t occur for a while. Also, in the last call, the CEO said that they could sell assets, but he wouldn’t do it today; that makes sense considering how narrow the cap rate spread is right now.

As for funding growth with debt, while management hasn’t excluded the possibility of using their credit line in the short term to acquire more assets, I think it’s unlikely they will be too aggressive here. While 54.8% of total assets being funded with debt is not very high, the company’s credit facility agreement has a covenant of a maximum leverage ratio of 60%. And the weighted average interest rate may be low at 3.85%, but debt/EBITDA at 7.95x and interest coverage at 3.38x, although sufficient, don’t have a lot of room for expanding and contracting, respectively.

In the last earnings call, the CEO also said:

The acquisitions, it could go on our credit line temporarily, but we do have things that we’ve put up for sale, which should match some of this, at least the earlier ones.

Right now, there are $280 million available under the revolver and though there are no maturities in 2024 and 2025, those that come after that involve large amounts. In 2026, a $350 term loan comes due, as well as $400 million under the revolver which has two 6-month extension options. To be clear, I don’t believe the maturities are well-laddered but I also don’t think the REIT will face problems refinancing; the credit facility agreement also has a $500 million accordion feature. However, I don’t see them funding growth through debt in an aggressive manner to have a large impact on growth in the short term.

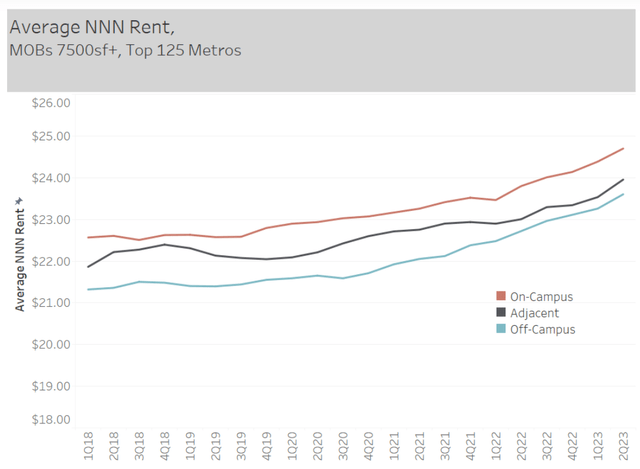

Another reason I expect stable but slow growth is that general off-campus MOB rent growth has been slow in the past:

revistamed.com

Coupled with the fact that the weighted average lease term is 5.8 years, investors should not expect high growth potential.

On the bright side, long-term leases offer better revenue stability. Also, the REIT’s portfolio consists of 185 properties that aggregate 4.8 million square feet and are spread across 34 states. That’s a well-diversified portfolio and minimizes the risk that comes from changes in population trends. The tenant base is also well-diversified based on an average rent coverage of 4.8x from 268 tenants and the fact that in the last quarter, no tenant accounted for more than 10% of rental revenue.

Of course, there were some bankruptcies in the past. The latest one was announced this year by Steward Health Care. But only 2.8% of the REIT’s ABR was coming from that tenant and management has already stated that it was actively pursuing opportunities for re-leasing the facility before the announcement, and it actually experienced a lot of demand. This is what the CIO said in the last call:

Shortly after the announcement was made that the facility was available, we got interest from a number of parties that expressed strong interest. And the conversations went pretty quickly as well.

But it’s hard to gauge. I mean, it could be very soon that we are finding ourselves negotiating a lease or it could take a few months for us to be in that position, hard to say. But the interest seems sincere and the conversations have been very positive.

Therefore, based on the state of the portfolio and the thesis for long-term stability in that sector, the outlook is positive. Consider that no matter what economic environment we are in, patients are still going to need treatment. Moreover, the median age of the U.S. population has been increasing historically, which is leading to increasing demand for medical services. Also, the sector faces lower risk from the work-from-home phenomenon as most of the work must only be done in the clinics; so, it is the nature of the industry that is favorable here as well. Last, based on CBRE, the supply in the sector struggles to meet this demand.

Wide Margin of Safety Offered By a Large and Undeserved Discount to NAV

Now, because of this stability in the income generated by Global Medical, this is an attractive income vehicle. But because the shares have taken a dive since interest rates started climbing in 2022, I also think that it’s a value play as well:

Right now, the AFFO yield is 10.44%, representing great value and potential returns when the market better appreciates the fundamental growth. The FFO multiple of 10.77x is also too low right now, considering that the sector median is 12.64x.

But most importantly, the implied cap rate the shares are trading at is 8.79%. We saw that average cap rates for MOBs are about 7%; that is also what management stated it can sell assets at today in the last earnings call. Reasonably assuming that this is more appropriate then, NAV comes at $13.55 per share, representing a 35% discount to NAV and a ~53% upside from the current price.

This may also understate the upside since based on GMRE’s 2022 high of ~$18.4 and the available information the market had back then, it had assigned a 27% premium to NAV (~$14.5). That’s more rational considering the excellent management of this business and should interest rates decrease to such a level again in the future, the shares could experience it again.

Risks

You should be aware of some risks, however, that, depending on your tolerance, may outweigh the potential benefits here. First, 18.7% of ABR comes from the state of Texas and 10.6% from Florida. That’s nearly a third of rental revenue coming from a tighter geographical area than one can initially imagine after observing how well-diversified the portfolio is. Long-term population growth trend changes could impact the bottom line of the business. That being said, that’s more applicable to those looking for long-term income generation; exiting the position after it’s clear the shares are fairly valued makes the impact of this risk’s realization less serious.

Another risk comes from the possibility of interest rates remaining elevated for longer than we think. If the REIT has to refinance at current rates in 2026, the cost of its debt will increase significantly, because its average interest rate is too low right now and the maturity too large.

I also need to remind you that it’s possible for management to cut the dividend if it needs to. The payout ratio is very high and managers may decide that freeing up some cash this way is the best option to take advantage of opportunities. Unlikely, of course, but this is definitely far from the safest dividend you can find in REITs right now.

Last but not least, NAV calculation is dependent on the data that we have today. There is, therefore, the risk that an increase in the average cap rate for MOBs results in our NAV being seen as unreasonably optimistic; the market reaction is going to punish shareholders if such a thing were to happen.

Verdict

All in all, I think the prospects supported by the high but sustainable dividend yield and undeserved undervaluation greatly outweigh those risks, so I am rating GMRE a strong buy. I am looking forward to monitoring this REIT very closely and changing my thesis if something material occurs.

What do you think? Do you own this REIT or intend to? Let me know and I’ll get back to you soon. Also, please leave a comment if you found this post useful; it means a lot! Thank you for reading.

Credit: Source link

{kind=link}