Konev Timur/iStock Editorial via Getty Images

Investment thesis

My initial cautious thesis about XPEL (NASDAQ:XPEL) (TSXV:XPEL.U:CA)aged well as the stock tanked by 52% since September 2023. The main reason is on the surface. The company’s offerings are mostly for new car owners, and the current interest rates environment significantly weighs on the demand for new cars as around 80% sales are financed in the U.S. The unfavorable environment has led to XPEL’s management substantially trimming revenue growth guidance, which adversely affected the stock’s fair value. All in all, I downgrade XPEL from “Hold” to “Sell”.

Recent developments

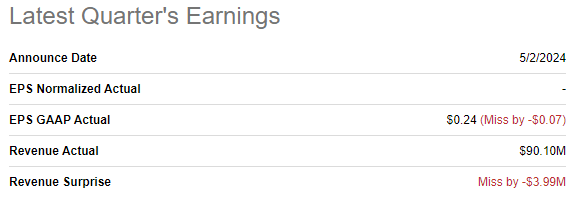

The latest quarterly earnings were released on May 2, when XPEL missed revenue and bottom-line consensus estimates. Revenue grew by 5% YoY, but the adjusted EPS shrunk from $0.41 to $0.24. Modest revenue growth is explained be the weakness in the U.S. and Chinese markets.

Seeking Alpha

The EPS decline is explained by a sharp increase in SG&A expenses. According to the management’s discussion in the latest 10-Q report, the company sharply increased marketing and personnel costs in Q1 “to support the ongoing growth of the business”. The explanation about the ongoing growth of business looks inconsistent with very modest revenue growth expectations for the next three quarters.

Seeking Alpha

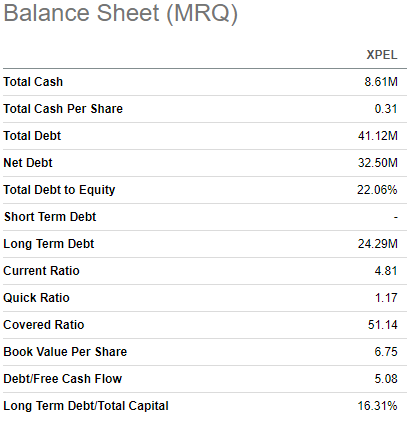

During the earnings call, the management was cautious and downgraded guidance for the organic revenue growth for the full year from 15% to 10%. I consider this downgrade as quite significant, but it looks fair given the unfavorable macroenvironment for the automotive industry with high interest rates. Nevertheless, I think that the company’s financial position is strong enough to weather the storm, as it has very low debt levels and liquidity metrics look healthy.

Seeking Alpha

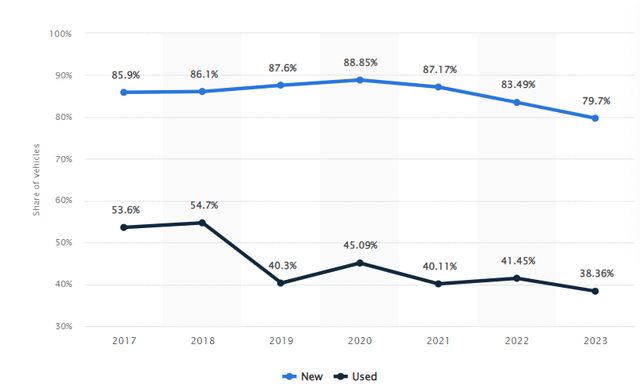

I believe that XPEL’s target audience is mostly owners of new cars because it is much less probable that the company’s products and services will be in high demand for used cars. Therefore, it is useful to understand trends in the industry of new cars. The market experiences headwinds as interest rates are still high. This is crucial because around 80% of new cars in the U.S. are financed, meaning that higher interest rates increase the amount of the monthly car loan payment.

Statista

The Fed remains quite hawkish, and they demonstrate no rush in decreasing interest rates. For example, in March 2024 the Fed announced that three rate cuts are coming this year. However, two weeks ago, there was an announcement that we will see only one interest rate cut this year. That said, the monetary environment is expected to remain unfavorable for the automotive industry, and XPEL particularly.

TrendSpider

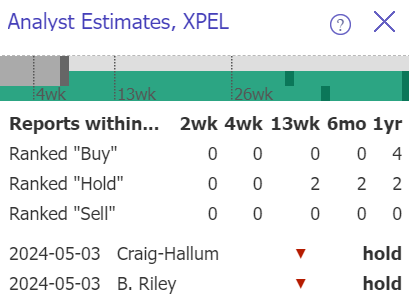

Therefore, I am not surprised that there were two downgrades from Buy to Hold from Wall Street analysts after the company’s latest earnings release. To add context, B. Riley slashed its target price estimate for XPEL from $74 to $37.

Valuation update

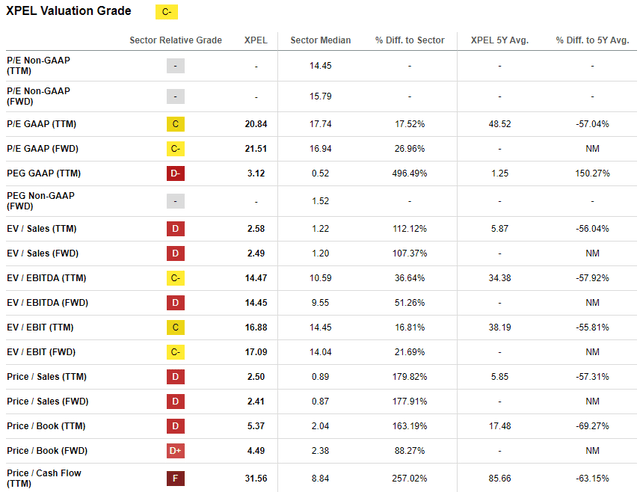

The stock plunged by 57% over the last twelve months and 2024 performance is also quite poor so far with a 33% YTD price decrease. Despite the big share price drop, XPEL’s valuation ratios are still high with a 21.5 forward P/E ratio and a massive 31.6 price to FCF ratio. That said, the stock still looks overvalued from the ratios’ perspective.

Seeking Alpha

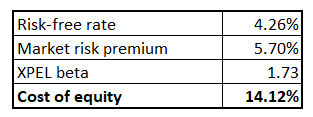

Looking only at ratios is never enough for me, which means that I have to simulate the discounted cash flow [DCF] model. Based on my CAPM calculations, XPEL’s cost of equity is 14.12%. All variables for the below table are easily available on the internet. I use cost of equity as a discount rate because of the company’s low leverage levels.

Author’s calculations

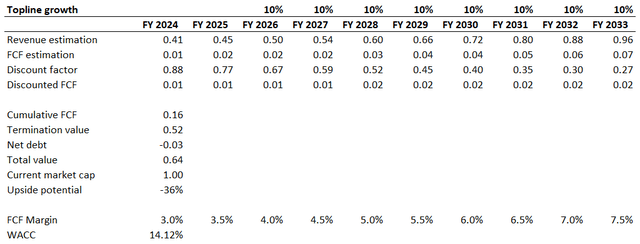

Consensus revenue estimates forecast around mid-single digit revenue growth for FY 2024 and FY 2025. The TTM FCF ex-SBC margin is 3%. The level of uncertainty about revenue and FCF growth is extremely high. However, what is extremely likely is that a 10% revenue CAGR and 50 basis points yearly FCF expansion are extremely aggressive assumptions for a company like XPEL.

Author’s calculations

As shown below, the stock is still significantly overvalued even with these aggressive assumptions. Therefore, the valuation is not attractive.

Risks to my bearish thesis

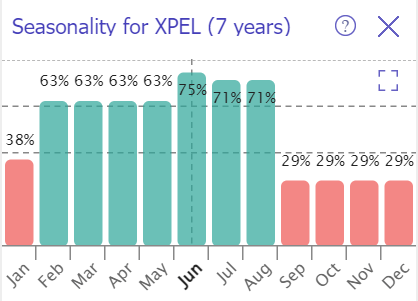

According to the seasonality analysis of XPEL from TrendSpider, the stock historically performs the best in summer. In more than 70% cases over the last seven years, the stock was green in each of the summer months. Therefore, the stock’s historical seasonality trends are against my bearish thesis.

TrendSpider

The environment is quite uncertain and is evolving rapidly, which might again affect the Fed’s decisions regarding interest rates. Therefore, the Fed might unexpectedly start cutting rates more aggressively than it is currently priced in by the market. In this case, the stock might see a solid rebound.

Bottom line

To conclude, I downgrade XPEL to a “Sell”. The stock’s fair value deteriorated significantly after the management trimmed its revenue growth guidance and the company started spending more aggressively on marketing and personnel. The macro environment is very unfavorable for the company as well, as high interest rates weigh on the demand for new cars.

Credit: Source link

{kind=link}