Unaihuiziphotography/iStock via Getty Images

Lifeward (NASDAQ:LFWD), formerly doing business as ReWalk Robotics Ltd., is a micro-cap medical device company that had its origins in creating a robot exoskeleton that assists people with spinal cord injuries to be able to walk. The company has been a long-time holding of mine and a name I have covered numerous times on Seeking Alpha going back to 2016. However, I have not updated my views in well over a year, going back to March of 2023, and more changes have probably been packed into the last year than the previous 10 years combined. I will get into the details below, but in summary, the most critical development is that the ReWalk exoskeleton was cleared for Medicare coverage, creating a clear pathway to possible profitability. With this critical development, I continue to like the long-term prospects. I rate the shares a “hold” for the near term, but a “buy” for the long term in spite of the lack of sustained traction in the market so far.

Detailed Review of Developments Since Early 2023

The title of my last piece was “The Next Phase Hinges On Medicare,” and in late 2023, the Centers for Medicare and Medicaid (known as “CMS”) approved the ReWalk exoskeleton for Medicare coverage. The submission of claims has gotten off to a solid start with 35 units (1 unit in Q4 of 2023, 34 units in Q1 of 2024), along with initial payouts from Medicare, with more claims in the pipeline. Management is guiding to a goal of delivering a range of 60 to 75 more units in 2024 to Medicare-eligible patients, for a total of about 100 units for the current year. This volume would amount to revenue on the order of about $9.1 million; to put that in historical perspective, total annual revenue from all sources from 2018 to 2022 ranged from about $4.5 million to $6.5 million. In other words, Medicare reimbursement alone from a revenue standpoint should be 50% greater than what the company was previously generating from all sales, including its sales in Germany and its existing coverage under the Veterans Affairs department.

Prior to the Medicare development, ReWalk closed an agreement in August 2023 to acquire AlterG for ~$19 million. AlterG had been a profitable company in private hands, selling specialized treadmills for physical rehabilitation centers. These treadmills employ zero gravity technology that is useful for patients who may experience some pain in walking. Selling AlterG products is done through a more traditional sales force and does not rely on getting individual approval for medical claims. The impact to ReWalk was obviously a use of cash, trimming their cash balance down to about ~$28 million at year-end 2023 from about $68 million to start the year, but expanding the revenue base by a large factor. The difference is significant – with the acquisition, the scale of the company goes from a $6 million annual revenue company to a $30 million annual revenue company.

In conjunction with this expansion into new business lines beyond robotics, ReWalk moved to doing business under a new name, and rebranded itself as “Lifeward,” which I believe is trying to capture the sense of moving one’s life forward, in spite of injury or setback. The legal business structure of the underlying entity remains ReWalk Robotics Ltd.

Lastly, in spite of the changes, the company’s shares had long been trading in the $0.70 range, with neither the acquisition nor the Medicare announcements moving the needle on any sustained basis. As a result, the listing was out of compliance with the standard to maintain a minimum of $1.00, so in order to regain compliance there was a reverse split of 7:1 in March 2024. On the split-adjusted basis then shares have regained compliance, moving in the $4.50 – $5.00 range since the split, though dropping further recently. There are now roughly 8.6 million shares.

Meet The New, Same As The Old?

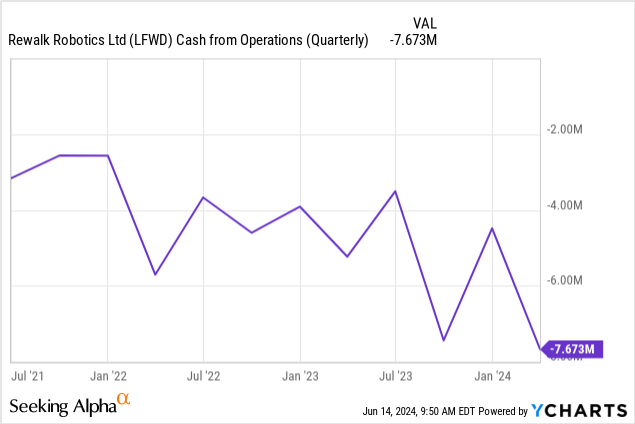

The lack of positive momentum in the shares in spite of the exciting developments, especially the Medicare coverage, probably leaves existing investors a little flummoxed. Exchanging a very strong balance sheet for the potential in AlterG may be one reason, with the company now pressed to really start executing to carefully manage its more depleted cash balances. The quarterly cash burn rate before the acquisition of AlterG was around $5 million, and through Q1 of 2024, that has not yet improved, in fact hitting a new low of ($7.7 million) during the last quarter, on a net loss in the quarter of ($6.3 million) and negative impacts from changes in working capital. Management’s overall assessment of the Q1 results was largely that they were attributable to taking some time to integrate AlterG’s operations and not to read too much into that single quarter.

I won’t dwell on those first quarter results, but offer a short sketch for information purposes, mainly to give a glimpse of how the tie-up with AlterG is impacting the scale of the company. First quarter 2024 revenue was $5.3 million, as contrasted with just $1.2 million in Q1 of 2023, or a 330% increase relative to the same period before AlterG was in the picture. Consolidated gross margin was just 26%, notably lower than previous quarters, which have at times ranged well over 40%. With operating expenses ballooning to $7.9 million from $4.9 million, especially notable in sales & marketing, net loss for the quarter amounted to ($6.3 million), or ($0.73) per share.

With about $20 million in cash remaining on the balance sheet, unless that narrative changes quickly, I believe the company has 12 months of cash, give or take. Publicly, management has expressed confidence more than once that they will achieve “breakeven” on their current cash in 2026, clearly implying a drastic reduction in cash burn starting immediately.

Resetting On Expectations and Valuation

CEO Larry Jasinski has stated that the company needs to be in the annual revenue range of at least $50 million to $55 million to hit that break-even point, with guidance for this year to be about 60% of the low-end of that goal. Baked into that assumption is at least having the capacity to double the delivery of the ReWalk systems in 2025 and again in 2026. That translates from a baseline in 2024 of 100 systems, growing to 200 next year and 400 in 2026. Assuming temporarily that there is qualified demand and available coverage for these unit goals, and they all go to Medicare patients (instead of attempting to split out sales in Germany or to VA patients), at the current reimbursement rate that would reflect around $18 million in 2025 revenue, and $36.0 million for 2026, with the implication being that AlterG would have sufficient sales get them over the hump of $50 million, which is realistic enough on paper. The top line growth targets are certainly aggressive, but not unrealistically high given the door being thrown wide open with the establishment of Medicare coverage.

Of course, higher revenue doesn’t necessarily lead to lower cash burn, though one would hope so over the long term. Mike Lawless, Lifeward’s CFO, explained how the new Medicare coverage impacted their revenue recognition and associated gross margin. In essence, he pointed to conservative revenue recognition practices with regard to Medicare due to uncertainty as to how many claims will receive final approval, so they apply a discount to it, planning to recognize the balance remaining once they confirm that the claim is approved. Secondly, Medicare covers 80% of approved claims, leaving 20% as the patient’s liability. However, many patients have Medicare supplemental insurance, of which there are many variations in terms of their benefits, but several of these supplemental plans do cover the remaining 20% for the patient. However, as ReWalk has no history with these supplemental insurances, they elected to not yet recognize any revenue that could come from them.

It adds to real money that goes straight against the topline, and any benefit from future recognition of the revenue would fall directly through to the gross margin improvement. Mr. Lawless summarized it this way:

Taking together these two factors, in Q1 ’24, we have reserved approximately $700,000 of revenue pending approval of claims by Medicare and supplemental insurance, and this affects our gross margin in Q1 ’24 by approximately 8 percentage points.

As the next couple of quarters unfold, I will definitely be looking for additional color around how the supplemental insurance claims are working out.

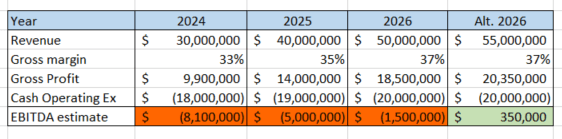

To hit that breakeven point by 2026, on just a fairly crude model, requires getting gross margins back closer to 40% and hitting the higher end of the revenue target while maintaining cash operating expenses at $5 million per quarter or less. Of course, the numbers in the outlook can be fiddled around with, but if they come close to hitting the $30 million in revenue mark for 2024 and end the year with more like 33% gross margin and really contain the cash operating expenses, then finishing with an EBITDA loss of less than ($10 million) is entirely plausible, and ultimately hitting the growth targets while expanding gross margin back towards its historical levels does point to the possibility of break-even by 2026 without running out of cash.

ReWalk / Lifeward EBITDA estimates, 2024 – 2026 (Author’s spreadsheet)

Two fundamental questions, as I see it, are 1) whether or not 400 ReWalk units in a year by 2026 is feasible, and 2) assuming the answer to #1 is a “yes,” then what is a reasonable path to expect beyond 2026 – can it do a lot better than break-even performance? There is actually a third question pertaining to how AlterG’s growth profile fits into the story, but at this point, I do not know that we have enough information to address that question.

The 400 units by 2026 question essentially depends on matching up qualified patients having a spinal cord injury with access to insurance coverage. There are three primary avenues for finding qualified patients with coverage. From a volume perspective, Medicare is the most important source, but ReWalk is also covered by the insurance given to American veterans by the Veterans Affairs department, and coverage through social insurance programs has been broadly established in Germany.

In terms of the United States alone, there would appear to be abundant opportunity to readily hit the 400 units per year, without even needing Germany (which for context, had 54 ReWalk cases pending at the end of Q1). While not everyone who suffers a spinal cord injury is a good candidate for ReWalk’s exoskeleton, according to the National Institutes of Health [NIH], there is a sufficiently large existing population and number of new cases per year that ReWalk would need only to capture an almost imperceptibly small share of the total to reach 400 units. From the NIH’s data, which I believe is current through 2022:

Between 250,000 and 500,000 patients each year suffer from [spinal cord injuries] globally. Most SCI cases arise from preventable causes, such as violence and [motor vehicular crashes]. Approximately 17,000 new SCI cases in the United States occur each year, and 282,000 persons are estimated to be living with SCIs.

There are additional medical details on the global prevalence and severity of disability from the NIH based on a 2019 study, but bottom line, even realizing that many of the cases of SCI may not be severe enough to result in the loss of walking, there should be no shortage of volume of people who could qualify in the United States alone. Accessing those potential cases is a result of getting patients qualified for disability and Medicare, followed by a separate timeline to qualify specifically for the ReWalk device.

So in terms of expectations, in order for there to be any present value, the growth will need to take that long-delayed hockey-stick turn for the ReWalk personal devices, with AlterG at a minimum holding steady in its contribution to revenues. At $4.50 a share, give or take, an investor today is essentially buying the odds that the growth story will do two things: 1) in the medium-term between now and 2026 grow sufficiently to hit at least break-even and not require additional capital, and 2) beyond 2026, continue to grow profitably, as there is no value to investors at merely breaking even.

Significant risks remain, beyond the inherent risks involved in micro-cap investing and the med-tech space. Specific to ReWalk / Lifeward, execution risk is shifted away from getting Medicare approval to now hitting large growth targets while also working out the integration of AlterG into the company’s development, all while keeping a clear eye on the cash on hand and really keeping a lid on expenses. Can you grow this aggressively while trying to hold spending down at the same time? It is not going to be easy.

Concluding Thoughts

The narrative switched from “everything depends on Medicare” a year ago, to now “everything depends on growth with the cash available.” Assuming that Lifeward can successfully scale that two-year mountain, then it will still be up to it to continue to grow beyond mere breakeven to justify any value to shareholders.

Overall, with the Medicare question now put to rest with a favorable outcome, I think the fruition of the growth aspirations long held is now or never. I am on the fence about the value brought to ReWalk from acquiring AlterG, as $19 million more in cash would have been a deeper buffer against the execution risks, especially now when the heat will be on to achieve that growth without letting operating expenses consume the available cash too quickly. However, the AlterG part of the ReWalk / Lifeward story is very early yet, and time may prove it to be a smart and timely expansion. With the growth gate open as wide as it has ever been for ReWalk, in spite of the risks, I consider it a “hold” in the strict sense that I do not necessarily believe the shares will move higher in the next twelve months, but for those with a time horizon going beyond 2025, I still consider it a cautious “buy.”

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Credit: Source link

{kind=link}