peshkov

I was attracted to Nuvei Corporation (NASDAQ:NVEI) last March while searching for global Fintech companies that promise to make it big in the future. Nuvei stock jumped 30% on March 18 – before I published my piece on March 17 – after the WSJ reported that a PE deal is likely to be finalized.

After evaluating the prospects for the company, I found Nuvei an attractive bet as the company was pursuing a growth strategy centered on new products, new markets, and new clients which I expected to result in strong earnings growth in the long run.

Soon after my analysis was published on Seeking Alpha, Nuvei announced that it had accepted an offer from PE firm Advent International to take the company private in a deal valued at $6.3 billion. This deal, which is expected to go through by the first quarter of 2025, values each Nuvei share at $34. NVEI is currently trading at $32 per share, which leaves little room for investors to look for an arbitrage opportunity, as expected.

A Great Business In The Making

Nuvei’s fundamentals have improved in the last few years, and I doubt whether long-term-oriented shareholders would be happy with the decision to take the company private in less than four years since its IPO. Nuvei stock hit a high of close to $150 in 2021 when growth stocks were moving higher in full swing amid zero interest rates, another reason why the deal price of $34 may not be appealing to some long-term investors. With this deal having the support of holders of multiple voting shares, who collectively control more than 90% of voting rights, there’s nothing much left to do for a retail investor in any case.

Coming to the business, I still find Nuvei very attractive.

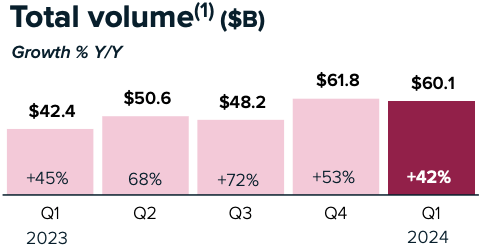

Total payment volume grew 42% YoY in Q1 to $60.1 billion, and growth is continuing to remain at very healthy levels. The payment solutions market is fragmented with many legacy and modern players vying for market share, and this has made it difficult for some companies to maintain stellar growth despite industry tailwinds. Not for Nuvei, though. In fact, Nuvei belongs among the aggressors who try to expand beyond borders to capture market share in new geographies.

Exhibit 1: Total volume growth

Q1 shareholder letter

Commenting on the company’s strategy and recent financial performance, Phillip Fayer, CEO, and David Schwartz, CFO, wrote to shareholders:

Results were driven by our ability to win market share from both legacy and modern players in our core verticals, by expanding our leadership and challenger position in large new end markets, by extending our footprint across more geographies, by growing upmarket with more marquee customers, and by continuously creating differentiated value across our global end-to-end payment solutions platform.

From a technology perspective, one of Nuvei’s biggest selling points is the single integration platform it offers to clients, which allows them to accept different types of payment methods seamlessly without having to configure the software to support each of these payment types individually.

The growing number of payment types supported by Nuvei is also a differentiator. According to the company website, Nuvei currently supports around 700 alternative payment methods, which makes it a top contender to secure deals with companies that are looking for global payment solutions.

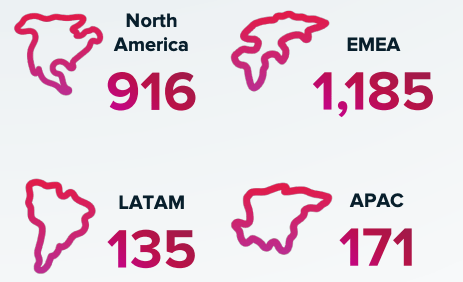

To maintain growth momentum, Nuvei is focused on expanding geographically. Below are some of the highlights from Q1 on this front.

- Nuvei launched direct local acquiring capabilities in Columbia.

- The company was awarded a Major Payment Institution license in Singapore, which is required by law to conduct payment activities in the country.

- Received authorization to operate as an electronic money institution in the UK.

Exhibit 2: Nuvei’s global footprint

Q1 shareholder letter

One attractive aspect of payment solutions providers, in my opinion, is the limited capital expenditures required to maintain growth after investing in the core software platform. Nuvei’s financial performance confirms this. Capital expenditures have consistently remained under 5% of revenue in recent quarters, allowing the adjusted EBITDA conversion ratio to reach as high as 86% in Q1. The company already pays a quarterly dividend of 10 cents and I thought Nuvei was well on track to rewarding long-term shareholders with both dividends and buybacks in the coming years.

In my previous analysis, I also predicted that the revival of the e-commerce industry would help Nuvei’s global commerce business, and there were early signs of that in Q1 where global commerce segment revenue increased 13% YoY to $192 million, accounting for almost 60% of total revenue. Nuvei’s global commerce expertise coupled with the growing B2B business is at the center of my investment thesis for the company.

Not to forget, a key ingredient of Nuvei’s success has been its willingness to cater to certain high-risk industries. For instance, the company accepts merchants from sectors such as gambling and other digital entertainment businesses that may be overlooked by legacy players. As a growth investor, I immediately found this to be a differentiator that could help Nuvei see outsized growth compared to the industry.

At a forward P/E of around 16, I strongly believe the market is still being very cautious about Nuvei’s prospects. Although the company may have missed a trick with the acquisition of Paya by potentially overpaying for the business at a time when Fintech companies were trading at cheap valuations, I believe Nuvei is well-positioned to see above-market growth in the next few years, which should have led to an expansion in valuation multiples had Nuvei decided to stay as a public company.

Takeaway

Nuvei, a business that I believe is moving in the right direction, no longer presents an investment opportunity as the company has agreed to go private in a deal with Advent. Although the deal price represents a 56% premium to the closing market price on March 15 – the last trading day before deal rumors – I still believe Nuvei would have seen much higher stock prices in the long run.

Credit: Source link

{kind=link}