SDI Productions/E+ via Getty Images

MidCap Financial (NASDAQ:MFIC) continues to report Net Asset Cash flow above its dividend at $0.38 per share with the last quarter reporting sustained earnings at $0.44. Higher interest rates definitely contributed to the result, yet management believes that the current dividend is sustainable for several quarters under any and all interest rate scenarios. We publish articles quarterly on MidCap, mainly because this is our second largest business development (BDC) holding. It is also our favorite. Our last published article in March, MidCap Financial Went Conservative But Still Offers Investors A Compelling Opportunity, discussed high yields at recent stock prices. We continue that discussion with a caveat, the price moved significantly higher signaling an opportunity door might be closing. The ATM is just across the street. Cross with me if you like to make a transaction.

Quarter

Noted above, MidCap Financial is a BDC targeted at mid-range size opportunities while investing in only very high senior debt. At the call, management noted,

“We believe MFIC has one of the most senior corporate lending portfolios among BDCs as evidenced by our weighted average attachment point of essentially zero. We believe we have constructed a corporate lending portfolio that will perform well even during a potential economic downturn.”

In addition, the reported business parameters include:

- Corporate lending at 92%.

- 97% 1st lien.

- 2nd lien exposure at less than 0.7%, almost zero.

- Investments in Merx aircraft now totals less than $190 million.

- PIK income remains low at 3%.

- A net asset value of $15.42.

- Net leverage of 1.35.

- Paying a de minimis amount of excise tax in March.

- Non-accruals remaining very low, totaling $14.4 million, or 0.6%.

- One entity, Naviga, is now in liquidation with the correct market value stated in company reports.

- Undistributable taxable income of $67.3 million or $1.03 per share.

Thus far, management reported no signs of credit weakness.

The price of the stock has been in the $16s but fell into the low $15s.

In this article, we listed several key parameters marking a last reference before the company most likely merges.

The Merger

Several months prior, MidCap announced a merger with two other Apollo Group investments, Apollo Senior Floating Rate Fund Inc. (AFT) and Apollo Tactical Income Fund Inc. (AIF). The senior floating rate fund invests in corporate senior notes rated below investment grade. Tactical Income blends senior loans with high yield corporate bonds. Management of the three groups announced that MidCap reached the necessary 50% plus for merging, but that the other two were a few percentage points short, approximately 48%, at the end of May. An additional month was added for investors to vote.

After the Merger View

With a merger likely coming, Kyle Joseph of Jefferies asked, “But did you give a sense or pro forma leverage or ballpark area post-merger?” Tanner Powell, company CEO, answered, “We’ll be somewhere around between 1.15 and 1.2 times levered.” This is a far cry from the current 1.35 level. Also, with the two other entities possessing mostly senior liens, risks remain low. At past conferences, when asked about timing for converting the merged entities into the MidCap instruments, management stated times from just more than a year to a few years. It depends upon marketplace strength. With the expected conversion approach, dividend yields will remain unchanged for all holders. Once completed, the combined group will have a lot of dry powder from which to invest leaving open possibilities for future dividend increases.

The Marketplace

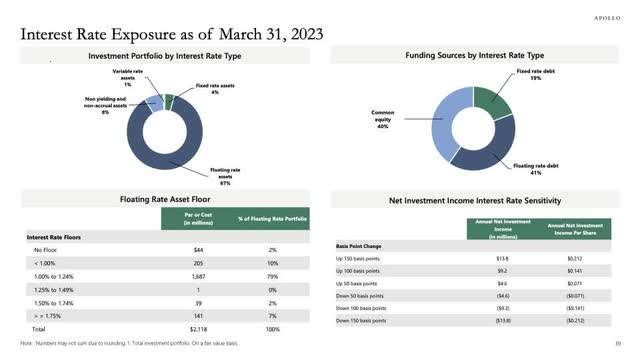

The company addressed several important marketplace conditions. We begin with the elephant in the room. Several BDCs use floating rate loans which have slightly positive biased returns at higher rates. MidCap is one which has benefited. The next slide from March of 2023 shows a relative relationship.

MidCap Presentation

At a 150-basis point change, the portfolio losses approximately $0.20 per share per year or $0.05 per quarter. A few important factors come into play for determining dividend safety. First, current earnings which average $0.45 per quarter, are well above the dividend. Second, the ablity to generate higher earnings through increases in leverage from its 1.35 to 1.50 still exist. And third, a year ago, management cut its fee schedule. Higher investor yields from lower fees is still in the early inning. At $0.38 per quarter, the dividend is clearly safe even with signficantly lower rates.

But the question remains, what will the Fed do? At year’s beginning, most believed that the Fed might cut rates multiple times. At the call, the company reported that Apollo’s Chief Economist believed that zero cuts were more likely in 2024. Maria Bartiromo hosted guest Peter Anderson on a recent show. His comment, 4% – 5% rates. are the long-term norms and might never be lowered except in unusual circumstances. That is a hard argument to counter in our view.

On the other side of the coin, the most recent employment report claimed significant job growth with the headline of 272,000 new jobs. But again, the underlining Household Survey showed severe weakness at a loss of 406,000. Unemployment jumped to 4% indicating how dangerously close a recession is. But the so-called red-hot headlining number likely took any cut in September off the table.

And then at May meeting, Chairman Powell offered investors a scenario which cuts once or 0.25% in 2024. This will have a minor negative affect on MidCap’s earnings.

Continuing, management discussed the ever-important weighted average net leverage of new commitments being at a strong 3.9 times. They also noted that a level of market strength appeared in the quarter stating,

“We believe the risk return on these new commitments is very compelling. Our pipeline of investment opportunities remains strong.”

For investors, MFIC focus on the middle market, makes it “less susceptible to competition from the syndicated loan market.” Last quarter, the company averaged 624 basis points for spreads unchanged from the previous quarter. The OID spread represents asset yields at 12%.

The marketplace has weakened some but generates still lucrative returns. This is also a parameter to carefully follow.

Dividend

The company held the dividend constant, which is significantly less than earnings. It also continues to carry-over excesses. Management reminded analysts that once the merger is approved, MidCap investors will receive a $0.20 special dividend.

A Chart

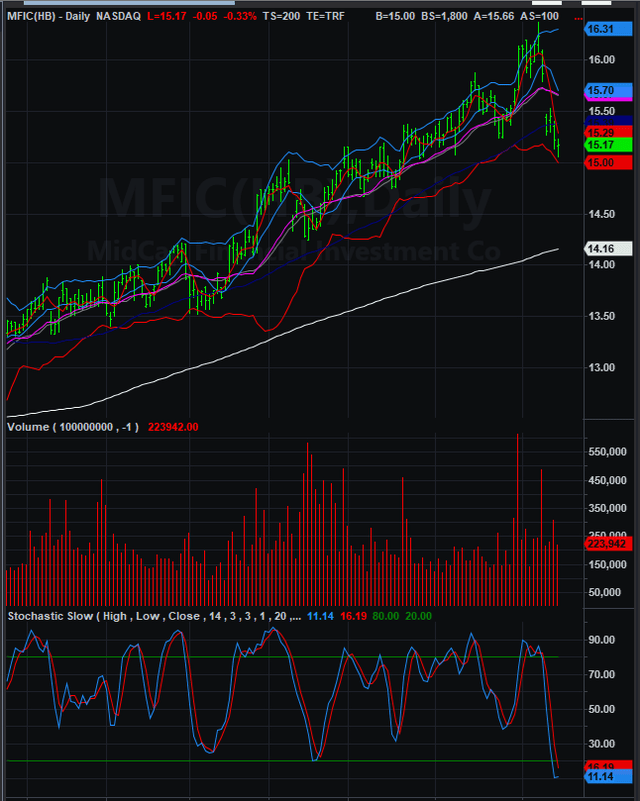

Included next is a MidCap chart generated using TradeStation Securities.

TradeStation Securities

The price had a nice long run from the $12s eight months ago, to the low $16s. A break in the price upward movement was clearly warranted. With the price now lower by over a $1 and the day stochastic underbought, investors might pay attention to buy.

Risks

We discussed a risk from lower rates, which could lower performance. Also, the cost of borrowing increased slightly from 6.94% to 7.09% due to the recent issued CLO being fully incorporated. On the other side with lower rates, debt costs will also fall in a relatively correlated fashion. A recession, which seems much closer than ever, also could put downward pressure on investment yields, except the company now has minimal 2nd liens and cyclical business exposure. Our biggest concern, for buying at this point, is price, which has fallen a point from its high, enough in our view to entice investors to watch for an entrance. On the basis of yield, stock prices above $17 would change our rating to a sell. It is about yield not about the value or health of the company. We continue a buy in the $15s. The ATM has a lot of money to dispense. Put your card in and enjoy.

Credit: Source link

{kind=link}