André Muller

Shares of Automatic Data Processing (NASDAQ:ADP) have been a moderate performer over the past year, rising 13%, though shares have been unable to sustainably break above $250 since last August. I last covered ADP in October, and I rated shares a “strong sell,” given its premium valuation, reliance on interest income, and slowing employment growth. Since that recommendation, shares have significantly underperformed the market, rising just 13% while the S&P 500 is up 30%. Given the magnitude of underperformance, a negative rating was justified, though the rally in shares has defied my concerns about a potential decline. Interest rates staying higher for longer has played a role in that, and now is a good time to revisit ADP.

Seeking Alpha

In the company’s fiscal third quarter, it grew EPS by 14% to $2.88 as revenue increased by 7% to $5.25 billion. ADP operates two units. Employee services earned $1.4 billion, up 14%, while its PEO services of $236 million were down 10%. Employee services is where ADP acts as a payroll processor for companies—this service is used by companies of all sizes. In PEO, it functions like the HR arm of employers, who outsource employment and benefits to ADP-this service is largely used by small businesses.

Employee services revenue rose by 8%, and per-employer headcount was up 2%. This additional growth was because client funds balances rose 6%, and ADP earned 3.1% on those balances from 2.5% last year. At quarter end, there were $47.9 billion in funds held for clients. This is a critical piece of ADP’s payroll processing business. Employers provide ADP the funds to pay their employees, and ADP distributes it to employees. In the meantime, it earns interest on the balances.

As such, ADP is a significant beneficiary of higher interest rates. Higher rates mean it can secure higher yielding deposits with banks, earning more net interest on these balances. In fact, in Q3, ADP’s pre-tax earnings rose $142 million to $1.184 billion. Half of this growth came from interest on funds held from clients–$71 million. Through nine months, higher interest income has accounted for about half of income growth as well. Indeed, because of wider interest spreads, employee services margins expanded by 230bp to 39.6%. Now, just as ADP has seen much of its profit growth come from higher interest income, when the Federal Reserve reduces rates, the reverse will happen. This is a concern of mine, as we look to the company’s outlook further below.

Its PEO unit has not performed as strongly, lacking the same cash balance tailwind. PEO Services revenue rose 5% to $1.7 billion, but 3% of this growth came from zero-margin pass-through business. Margins compressed 220bps to 14.2% given mix toward zero-margin business. Employment was up 3% to 723k. This is a fairly slow growth business with relatively tight margins.

Overall, ADP is performing as one would expect in a buoyant labor market with high rates. To its credit, it continues to show excellent cost discipline with SG&A up just 0.2%. Because it holds client funds to pay employees, ADP needs to retain an excellent balance sheet. As such, it carries $3 billion in long-term debt against $3.3 billion of corporate cash. It should also generate about $3.2 billion in free cash flow this year.

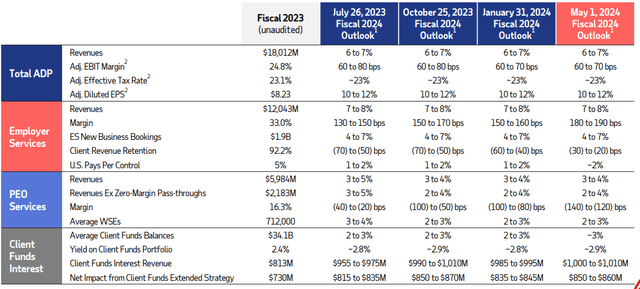

Last October, I forecast $9-$9.20 in earnings power. As you can see below, ADP is guiding to about $9.13 in EPS, consistent with my expectations, and the analyst consensus is currently $9.15. With no changes in interest rates or significant shift in employment, I would expect fiscal year earnings to come in-line with guidance, around $9.15.

ADP

ADP’s earnings have broadly followed my expectations laid out last October, +/-$0.05, and so the meaningful share price underperformance does not surprise me vs the market, though I am somewhat surprised that shares have risen even as much as they have. Ultimately, I continue to believe the market is assigning ADP too high of an earnings multiple. Now, this year EPS growth will be about 10-12%, but half of this growth is coming from client funds’ interest revenue. Excluding this, growth is closer to 5-6%. That is still growth, of course, but shares have a 3% free cash flow and 26.7x earnings multiple, which is expensive for a company with mid-single digit growth.

Now, the analyst consensus is for $10.00 in EPS next year, or about 9%, which simply seems too aggressive. Even if we held interest rates flat, this consensus would assume an acceleration in the noninterest aspect of the business. Moreover, holding rates flat is an aggressive assumption. In my view, we will see 1-2 rate cuts this year, and then depending on the trajectory of inflation, 2-4 rate cuts in 2024.

If we assume client fund balances rise 3%, but the average yield falls by even 40bp (i.e. 1.5 cuts on average), that will be an over $100 million net headwind to pre-tax profits and a ~2-2.5% reduction in EPS. I view this as a reasonable central case for interest income, absent a recession (not my base case), which would push rates down further.

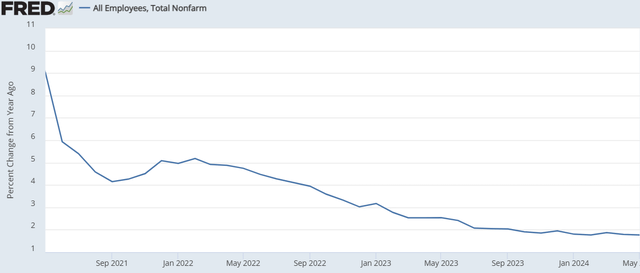

The next question is how fast the company can grow ex-interest income. Given its dominant size, ADP is more impacted by overall employment trend than market share ones. Over the past year, there has been 1.8% employment growth as of May. As you can see, this has been steadily decelerating for the past three years. Slower payroll growth all else equal means slower growth for ADP.

St. Louis Federal Reserve

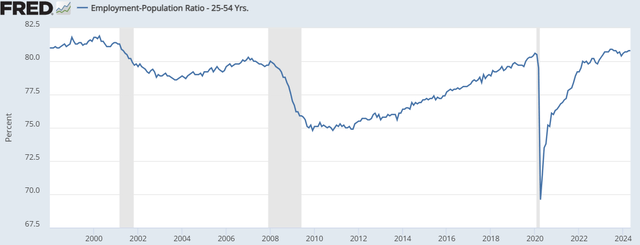

Of course, slowing job growth is entirely consistent with the aging of an economic cycle. As the labor market improves, there are fewer remaining unemployed workers, which means there are fewer people to hire and add to payrolls, slowing job growth. We are at that point. Indeed, prime-age employment to population is essentially at historic highs. Without significant slack in the economy, employment growth will continue to slow towards labor force growth, which is likely closer to 1%.

St. Louis Federal Reserve

Now, with price increases and strong cost discipline, ADP may be able to build some operating leverage. Still, we are looking at a revenue environment where revenue growth is likelier to be 2-4% next year, assuming slower employment growth. From that, we may see 3-6% earnings growth, depending on the ability to hold costs flat. Based on its pace of repurchases, its share count should be about 1% lower, but net interest income will be a 2% headwind. As such, I look for 2-5% EPS growth in fiscal 2025 or $9.50.

25.7x earnings for a company with mid-single digit growth is expensive in my view. ADP is not trading like other companies that receive much of their income growth from higher rates. Companies like Chubb (CB) for instance trade at 12x. When we see the Federal Reserve begin to lower rates, investors may more clearly appreciate how much of a driver of earnings growth interest rates have been. Combine this with slowing job growth, and ADP’s growth profile is not particularly impressive. Its 2.3% dividend is also not high enough to be the sole reason to own the stock.

ADP has tremendous scale, a capital-light services business, and a flawless balance sheet. I understand the appeal of owning that type of business, but nearly 26x forward earnings with EPS growth set to decelerate meaningfully is in my view over-paying for that type of growth. I would rather own a company like Chubb at a much lower multiple. Or if one wants a higher-growth, high-multiple stock, ADP’s P/E is not much different than companies like Alphabet (GOOGL) and Apple (AAPL), which with AI may have much faster growth prospects than a company like ADP.

The S&P 500 has a 21x forward multiple. With slower growth but a better balance sheet, I can justify a market-like multiple for ADP. That would be closer to $205, pointing to about 16% downside. With earnings growth set to slow, ADP is too expensive. I continue to expect it to significantly underperform the market, and I still expect shares to fall on an absolute basis. I would be a seller of ADP and continue to view shares as particularly unattractive.

Credit: Source link

{kind=link}