Gilnature

Investment Overview

SIGA Technologies (NASDAQ:SIGA) is a New York based, commercial stage pharmaceutical company with a niche product. To quote from the company’s Q1 2024 quarterly report / 10Q submission:

The Company sells its lead product, TPOXX® (“oral TPOXX®,” also known as “tecovirimat” in certain international markets), to the U.S. Government and international governments (including government affiliated entities). Additionally, the Company sells the intravenous formulation of TPOXX® (“IV TPOXX®”) to the U.S. Government.

TPOXX® is an oral formulation antiviral drug for the treatment of human smallpox disease caused by variola virus. On July 13, 2018, the United States Food & Drug Administration (“FDA”) approved oral TPOXX® for the treatment of smallpox. The Company has been delivering oral TPOXX® to the U.S. Strategic National Stockpile (“Strategic Stockpile”) since 2013.

In connection with IV TPOXX®, SIGA announced on May 19, 2022 that the FDA approved this formulation for the treatment of smallpox.

In addition to being approved by the FDA, oral TPOXX® (tecovirimat) has regulatory approval with the European Medicines Agency (“EMA”), Health Canada and the Medicines and Healthcare Products Regulatory Agency (“MHRA”) of the United Kingdom.

The EMA and MHRA approved label indication covers the treatment of smallpox, monkeypox (“mpox”), cowpox, and vaccinia complications following vaccination against smallpox. The Health Canada approved label indication covers the treatment of smallpox.

This product and business model has served SIGA well over its years as a listed company – the company completed its Initial Public Offering (“IPO”) in 1999, raising $13m at $5 per share.

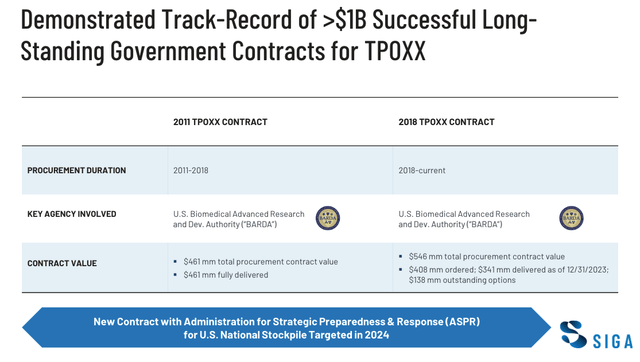

SIGA’s BARDA contracts (investor presentation)

As we can see below, SIGA’s main source of revenues over the past decade and more has been via its contracts to supply TPOXX to the U.S. Biomedical Advanced Research and Development Authority (“BARDA”). The US maintains a supply of TPOXX under Project BioShield to guard against the threat of an outbreak.

The vast majority of revenues from the first contract were realised in 2018, when SIGA reported $477m of revenues – prior to its FDA approval, revenues from the first agreement had been deferred owing to the possibility the product would not be approved and require replacing.

Since 2018, revenue generation has primarily come from this source, and has been consistent – $125m, $134m, $111m and $140m in 2020, 2021, 2022 and 2023, and margins have been impressive – net income in those years amounts to $56m, $70m, $34m, and $68m. In short, this is an efficient, profitable company, however there are potential downsides.

Firstly, A heavy reliance on the BARDA contract – $98 million of 2023 fourth quarter product sales of oral TPOXX were to the U.S. Strategic National Stockpile (“SNS”), out of $131m product sales altogether. Secondly, a potential lack of growth potential, with only one product to market and sell, that is not a widely demanded product, for obvious reasons.

On the other hand, the possibility that SIGA is one day required to manufacture substantially more of its product in response to an infectious disease breakout is continually in play – in 2022, for example, the last time I covered SIGA for Seeking Alpha, its stock price was rising fast due to an outbreak of Monkeypox – as I wrote at the time:

According to CNBC, by Tuesday this week there had been 131 confirmed cases of monkeypox, and 106 suspected cases across 19 different countries, including the U.S., U.K. Canada, Australia, Italy, Spain and Portugal.

I gave SIGA a “buy” recommendation when shares traded at $12, their highest ever value, and although in the course of the next few days they rose to $17, as the number of cases began falling, the share price began to rapidly decline.

SIGA in 2024 – A New BARDA Contract Needed, Expansion Plans Afoot

In May SIGA announced its Q1 2024 earnings, reporting some impressive numbers – product sales rose to $23.9m, from $5.7m in the prior year quarter, operating income was $11.3m, versus a loss of $(2.1m) in 2023, and earnings per share were $0.14, compared to $(0.01) one year ago. SIGA management also declared a special dividend of $0.6 per share, paid in April. The company additionally reported a cash position of $144m.

Once again, BARDA accounted for the bulk – $15m – of revenues, which went to the SNS. According to the earnings press release, “$8 million of oral TPOXX was delivered to eight international customers.”

There may not be any reason to panic, but it does seem as though the contract with BARDA is up for renewal – speaking on the Q1 2024 earnings call, SIGA’s CEO Diem Nguyen told analysts:

With regard to the important U.S. market, as we look forward to fulfilling any remaining oral TPOXX orders under our current contracts to supply TPOXX to the U.S. Strategic National Pile, we are ready to work in close collaboration with the U.S. government in the next contract for SNS stockpiling.

We are confident on our ability to provide superior value to the U.S. government and collaborate with them to achieve the best outcome for public health security, SIGA shareholders and patients. Our aim is to secure a long-term contract with annual purchases that reflect TPOXX value today and in the future with a potentially expanded label.

There does not appear to be any major obstacle to a contract being renewed – after all, the US government will doubtless want to keep replenishing its stock of a smallpox antiviral – but with that said, the government does not have an obligation to sign another long-term deal with SIGA – in its 2023 annual report / 10K submission, management notes:

TPOXX® faces significant competition for government funding for both development and procurement of medical countermeasures for biological, chemical, radiological and nuclear threats, diagnostic testing systems, and other emergency preparedness countermeasures.

Our commercial opportunities could be reduced or eliminated if our competitors develop and commercialize products that are safer, more effective, have fewer side effects, are more convenient or are less expensive than products that we may develop.

SIGA name checks two companies – Emergent BioSolutions (EBS) and Bavarian Nordic A/S – as direct competitors, and any company in this field would doubtless push hard to try to negotiate the kind of deal that has turned SIGA into a successful, profitable, company.

Analysts on the earnings call guessed that discussions may take place in 2025 or 2026, but with the fourth and final tranche of the current contract set to be delivered in 2024, CEO Nguyen stated:

Although we haven’t yet received notice from the Administration of Strategic Preparedness and Response about its plans for issuing another RFP for the U.S. National Stockpile, we are preparing for it some time this year.

It is difficult to know how this scenario may play out – on the one hand, SIGA management seems confident a new contract will be agreed, on the other, it has declined to provide 2024 guidance pending news of a new order from BARDA.

There are no two ways about it, the contract is extremely valuable to SIGA and without it, the company would doubtless lose a good chunk of its valuation and share price value – as much as 75%, perhaps, based on the revenues it brings in.

SIGA does have other wheels in motion, for example, it sells its product in 25 other countries, where it is eligible to treat cowpox, mpox, and vaccinia virus, and it is conducting clinical studies for an approval in post-exposure prophylaxis (“PEP”), with an FDA submission planned in 2025, developing a pediatric program, and supporting five separate studies in mpox globally.

Management states in an investor presentation that it has “sold $100m of TPOXX to different countries since 2020”, but compared to the near $1bn received from BARDA, it may not be nearly enough to sustain recent progress should the BARDA contract be lost for any reason.

Looking Ahead – Post Q1 2024, Is SIGA Stock A “Buy”, “Sell”, or “Hold”?

2023 was a strong year for SIGA and 2024 will likely be equally as strong, with the final $113m tranche of the BARDA order to be delivered. The solid performance has led to a recent uplift in SIGA stock, which has risen by 42% year-to-date. The share price did, in fact, reach $10, but fell after the Q1 2024 earnings were reported in May.

With a market cap valuation of $565m at the time of writing, 2023 net income of $63m gives us a historic PE of ~9x, and it may well be that the forward PE is lower still, underlining that this is a profitable business.

While analysts at Edison have suggested SIGA’s stock price could reach $16 per share, based on income of ~$84m in 2024, this model assumes not only that there is no change in the relationship with BARDA, but also that sales in Europe, Japan, where the company has a commercial partner, and Australia, increase substantially over time.

There is also the supplementary NDA submitted for PEP, which requires a longer treatment course, increasing the market opportunity, and the opportunities with pediatric and mpox, although it may be worth noting that the IV approval for TPOXX has not been a major revenue driver to date.

Ultimately, I’d award SIGA a “hold” rating as the risk that amendments to the BARDA contract are not satisfactory for the company concerns me, and I would still regard this as absolutely key to the company’s future performance, despite the other growth initiatives in play.

Of course, as I have discussed before, SIGA stock can spike in the triple-digit percentages overnight in the event that a large number of mpox, or cowpox, outbreaks are observed, and shockingly, CEO Nguyen told analysts on the latest earnings call:

The CDC reports that the DRC is experiencing its largest surge of mpox cases ever recorded, with over 19,000 suspected cases and more than 900 deaths from January 2023 until about a week ago.

SIGA undoubtedly plays an important role in the global stockpiling of valuable antivirals against infectious disease, but at present, given all factors in play covered in this article, I believe the company to be fairly valued – any opportunistic investor willing to buy and hold, in the expectation of another infectious disease scare driving share price gains, would have to be patient, but such an event is likely to occur every few years.

Credit: Source link

{kind=link}