Yagi Studio/DigitalVision via Getty Images

Solo Brands (NYSE:DTC) is a company building a direct-to-consumer (DTC) business focusing on outdoor and lifestyle products for customers in the US.

All-time share performance has been disappointing. Having gone public in 2021 at a price of $18, the stock reached its all-time high of $21 towards the end of 2021, but then continued trending down and reached low-to-mid single-digits in the next two years. Recent performance has been weak, with DTC being down over -61% and -67% on a 1-year and YTD basis. It is currently trading at $1.9 per share.

I rate the stock a buy. My 1-year price target of $2.6 per share projects about 38% upside. At this level, DTC appears undervalued. Risk reward remains decent, in my opinion. The management has taken active steps in improving marketing ROI by working with a leading agency, a big commitment that could bring in investors’ confidence. Nonetheless, I believe execution of the strategy will dictate share price in the medium term.

Financial Reviews

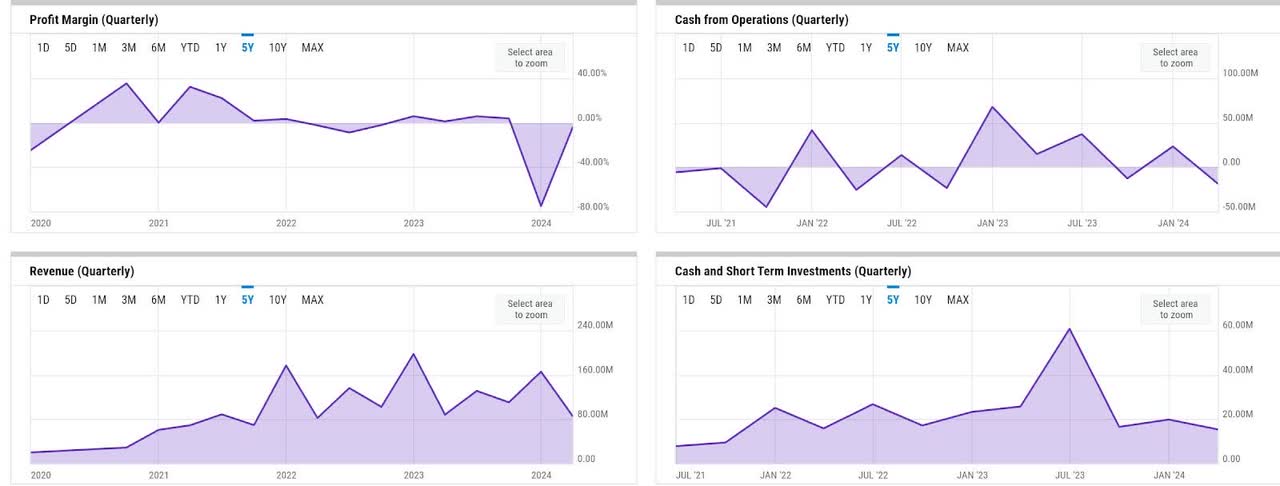

ycharts

Fundamentals have been relatively underwhelming as of late. Revenue declined YoY in FY 2023, and in Q1 2024, DTC maintained that trend, delivering a quarterly revenue of $85 million, down -3.3% YoY. Meanwhile, DTC also realized GAAP net loss in Q1. Net loss margin was -4% in Q1, while the same time last year, it was 1%. Furthermore, DTC also burned through -$18.4 million of OCF in Q1, in contrast to the same time last year when DTC generated $14.7 million of OCF.

Liquidity saw a downtick in Q1, though it has relatively been steady above $15 million for some time now. This was also helped by the $92 million raised from debt issuance in Q1, which the company used for share repurchases and also debt repayment. On a net basis, financing cash inflow of $16.3 million, which mainly consisted of $22 million debt issuance, offset the OCF burn in the quarter and helped maintain stability. As a result, DTC only saw a -$4.4 million of decline in liquidity. I believe DTC is likely to see better OCFs in the consecutive quarters due to the potentially higher spend in Q1, which should alleviate concern about liquidity runway. Meanwhile, the debt-to-equity ratio saw an uptick to 0.7x, highest level since 2021.

Catalyst

Though major catalysts appear minimal at present, the swift action by the management to improve the underperforming D2C channel and the recent initiative to hire a leading marketing agency could be important drivers for a growth turnaround. As reported by some media outlet, the performance of the commercial partnership with Snoop Dogg to make viral one of the DTC’s brands, Solo Stove, has fallen short of expectations. As commented by the management in Q1, this has resulted in inefficient marketing spend as of late.

However, it appears that the management has taken important steps to fix things up as of Q1. As commented by the management, DTC already saw a much softer D2C revenue decline in Q1:

On our last call, I talked about fixing our direct-to-consumer or D2C business and returning this channel to growth. Although still way too early, I very much like the progress we saw in Q1. As I mentioned earlier, we went from minus 21% in Q4 versus prior year to minus 6.8% in Q1 versus prior year, certainly not a victory, but a marked improvement. And importantly, we gained momentum as Q1 progressed

Source: Q1 earnings call.

10Q

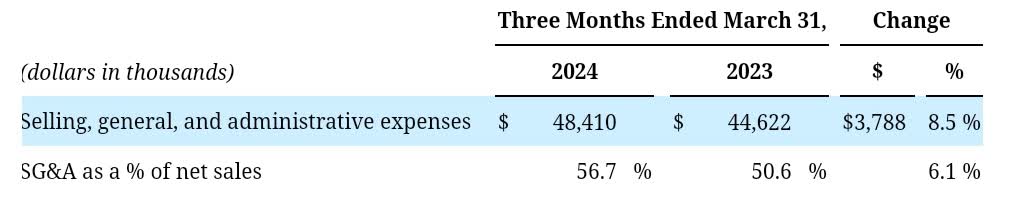

D2C revenue continued to make up over 60% of DTC’s business as of Q1, which means that an improvement there should bring in a meaningful impact to the growth turnaround plan. Furthermore, SG&A expenses also remained high, making up almost 57% of revenue in Q1, up 6% YoY, suggesting that there is indeed a potential room for more efficiencies here. In my opinion, though I would expect the positive impact to only be noticeable at least in the medium term, the recent appointment of the new agencies could potentially help achieving the goal, as per the management’s comment:

Now it will take time to see significant sales growth from the new doors, but I’m encouraged about the trajectory for our retail channel moving forward. During the last call, I discussed our plans to change marketing agencies. We efficiently entered a new relationship with a world-class marketing agency that has full funnel performance and digital capabilities. I am highly confident this will pay dividends as we move through the balance of this year and beyond.

Source: Q1 earnings call.

Risk

Risk to my thesis remains high. While the management appears to have taken the right steps, in my opinion, everything remains uncertain. The ongoing work with the new agency, for instance, has only reached 50% completion. However, the next important part would be the implementation of the strategy. This uncertainty is further exacerbated by the new leadership appointment in Solo Stove, where the Chief Growth Officer of the company, Mike McGowan, will take on an added responsibility as the president of Solo Stove. In my opinion, the dual responsibility here could result in lower effectiveness due to the dispersed focus in the less desirable scenario.

Valuation / Pricing

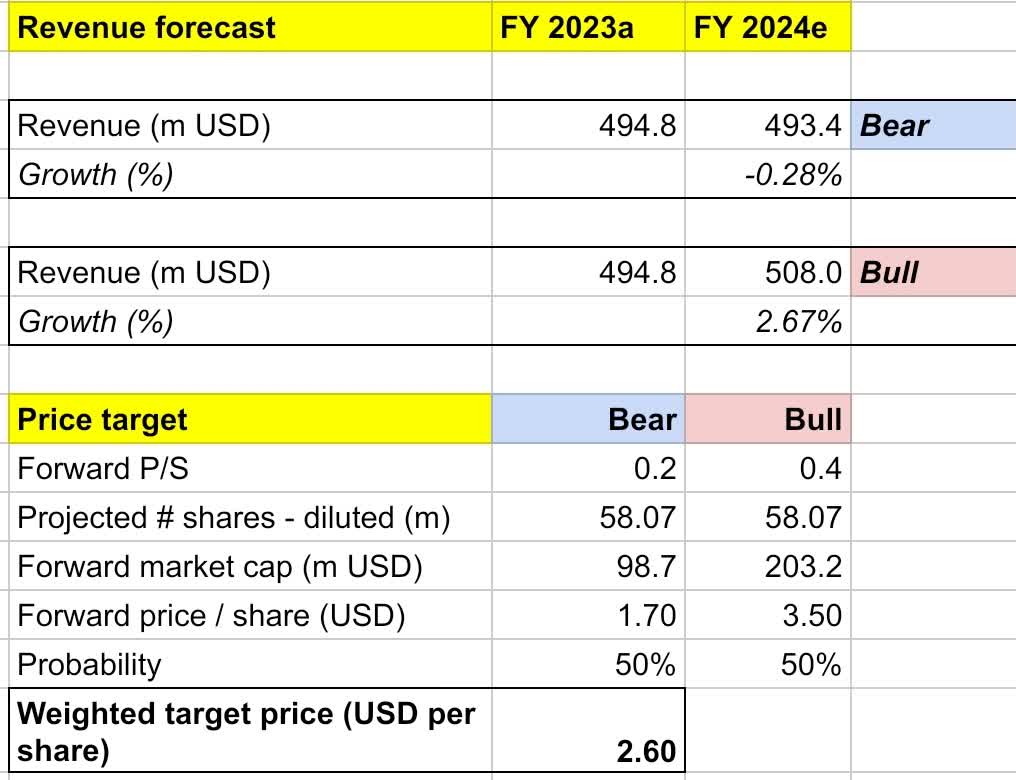

My target price for DTC is driven by the following assumptions for the bull vs bear scenarios of the FY 2024 projection:

-

Bull scenario (50% probability) assumptions – I expect revenue to grow by 2.7% YoY to $508 million, in line with the market’s estimate. I assume forward P/S to expand to 0.4x to assume a share price appreciation to $3.5.

-

Bear scenario (50% probability) assumptions – DTC to deliver FY 2024 revenue of $493.4 million, a -0.3% YoY decline. I assume P/S to contract slightly to 0.2x, driving share price down to $1.7.

own analysis

Consolidating all the information above into my model, I arrived at an FY 2024 weighted target price of $2.6 per share, a projected 1-year return of about 38%. I would rate the stock a buy.

My 50-50 bull-bear probability assignment is based on my belief that DTC’s outlook is still highly uncertain, driven by the relatively new initiatives in place to drive turnaround. At this point, I believe investors should continue monitoring DTC’s progress, especially on the marketing strategy implementation with the new agency. Overall, though, I feel that DTC remains a decent undervalued opportunity that could see an improvement in share price upon early signs of turnaround in the D2C business.

Conclusion

DTC is a company building outdoor and lifestyle branded products for customers in the US. It recently experienced a setback from the inefficient marketing campaign, resulting in revenue decline as of late. Management has taken active steps to improve the situation. Revenue decline in Q1 was softer as a result, demonstrating a decent progress. The recent appointment of a new agency to take care of the marketing initiatives could also lead to better marketing ROI. I expect risk to remain high until DTC could demonstrate more successes across these activities. My price target model suggests that DTC may appear undervalued. I would expect a $2.6 price target at year’s end, with 38% potential return, rating the stock a buy.

Credit: Source link

{kind=link}