Natali_Mis

Back around early 2022, my boss at my last company urged me to write a bullish recommendation for Crispr Therapeutics (NASDAQ:CRSP).

I never heard of it. But that was ok. I love using quant screens and ratings to discover exciting new ideas. And our model favored CRSP.

So, I looked… And I nearly spit my coffee all over my keyboard. This was a no-serious-financials R&D shop. How, I wondered, could our model possibly flash a green light?

I quickly understood.

Imagine a company goes from little or no revenue in one period to massive revenue in the next. That’ll compute to a massive growth rate. And it’ll exert bullish pressure on a quant model that works with growth.

That’s an example of the kinds of things I was seeing with CRSP.

This is that ever-present challenge to quant investing. Sometimes numbers meet the letter of the law, but not its spirit.

That’s why I objected to recommending CRSP. My boss wasn’t happy. “But CRSP is the future of medicine,” he argued.

We argued back and forth. Eventually, I won. We passed and I wrote up another stock.

It’s different now. I don’t work there anymore. And I’m no longer tied to that company’s or any other quant model.

But being a futurist at heart, I’m still intrigued by the CRSP story.

The absence of usable financial numbers remains challenging. But as I demonstrated with Nvidia (NVDA) on May 28, 2024, I now use a different framework to assess stocks.

CRSPR presents another, extreme, version of the same story.

So, let’s get to it.

The Future of Medicine

It’s about gene editing… changing an organism’s DNA

It’s not like changing a wine lover into one who can only tolerate beer. This kind of transformation is much deeper. Operant conditioning, using rewards and punishments to teach new behaviors, can do that.

Gene editing literally changes one’s underlying physical traits, stuff we think of as having been inherited and with which we’re stuck.

Taken to the extreme, we might imagine reprogramming a human to grow a third ear in the back of one’s head. But for now, things like that would be limited to science fiction.

Gene editing is still pretty new, so it can’t yet do all we imagine. And it raises a whole new set of ethical considerations.

For now, this is about curing disease.

To appreciate that, let’s understand what exactly genes are. I’m not a geneticist, so I’ll stay pretty basic… but will cover enough to appreciate CRSP as the future of medicine.

Cells are the building blocks of all living things (Genes made Easy).

Each cell has a specific job. It knows what to do thanks to the DNA hidden inside the cell.

DNA operates as an instruction manual. The pages of this manual are known as genes. Each page (gene) has instructions telling the cell to make proteins.

We see and feel the result of what these proteins do. They result in eye color. They power your muscles. They attack bacterial invaders. And so forth.

Each page in a book is unique based on combinations of letters and words. Genes work similarly.

Each gene has a sequence of chemical bases known as A, C, T, and G. Each base is analogous to a letter. Each combination is analogous to a word.

As with any unedited manuscript, some pages are properly written. Others are not.

With genes, a badly written page is called a mutation.

Life is imperfect. So choppy pages and mutated genes occur often. We simply tolerate, and sometimes barely even notice choppiness/mutations. Most are harmless.

But sometimes, someone has to fix things.

An editor will correct a badly written page to make it publishable.

A truly troublesome genetic mutation manifests as disease.

Throughout human history, we responded to disease by treating it where we could. We try to mask its impact. But the mutation remains.

Now, however, we’re in a new world. We’re gaining the ability to eliminate bad mutations. We change the gene itself. We literally edit the gene… cut out something bad and replace it with something better.

CRSP isn’t alone in being able to edit genes. But according to MedlinePlus.gov, the company’s “CRiSPR-Cas9 system has generated a lot of excitement in the scientific community because it is faster, cheaper, more accurate, and more efficient than other genome editing methods.”

How CRISPR-Cas9 Works

Actually, CRiSPR-Cas9 isn’t a wheel CRSP invented from scratch. The protocol mimics nature, specifically, the way bacteria fights viruses. (Don’t always cringe at the word “bacteria.” Some kinds help, rather than hurt us.)

A bacterial defender will capture (kidnap) small pieces of a virus’ DNA. The defender inserts the viral DNA into its own DNA. This creates, within the defender bacteria, “Crispr arrays.”

These let the defender remember the virus. When the attacker (or something similar) comes back, the defender’s CRSP array makes RNA. This shows where within the attacker to go in order to cut and disable the virus.

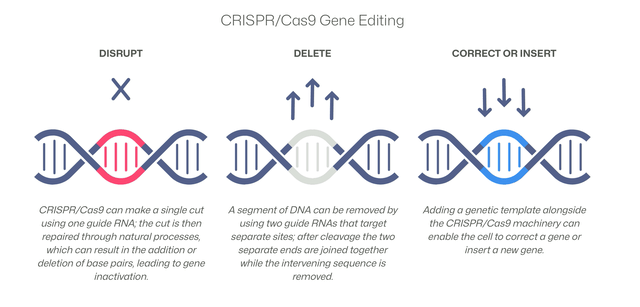

The CRISPR-Cas9 system imitates nature by creating a small piece of RNA with a short guide sequence. That will bind to the attacker’s DNA.

A Cas9 enzyme then cuts the appropriate part of the attacker DNA. The cell in which the attacked DNA lives will make a repair. It will replace the bad part of the DNA with something more suitable.

Here’s a very simple illustration of the extract-fix-replace process.

CRSP IR

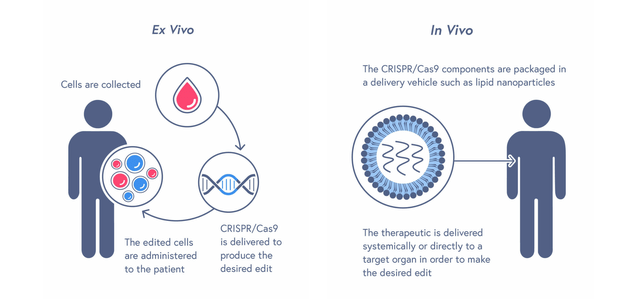

This can occur this inside a person’s body (In Vivo). Or it can be done outside (Ex Vivo) …

CRSP IR

So CRSP doesn’t just mask symptoms or do anything like that. It really Cures disease (bold face and with a capital “C”).

This is heady stuff.

No wonder it took well into the 21st century to get this going. I first heard of biotechnology in the 1970s.

That happened when I visited the brokerage office at which a friend worked. It turned out to have been a bucket shop that pushed tiny biotech IPOs. They wanted to capitalize on the fame of Genentech (a legitimate 1976 startup that became a Roche AG subsidiary in 2009).

Today, biotech is a very big deal. Naïve observers suspect that’s all about doing fancy things with genes. But that’s not really so.

Workaday biotech aims at the same kinds of tasks as do pharmaceutical companies. The differ in how they go about it.

Pharma companies use chemicals to develop drugs. Biotech companies use living organisms (biologics).

CRSP gene editing really is a new thing. Or as my ex-boss said, “the future of medicine.”

That’s the good news.

Now, here’s the bad, or let’s say more challenging, news…

Futurism Alone Does Not Make for a Good Investment

Right now, Cathie Wood of ARK Invest is invested heavily in CRSP.

It’s the sixth largest holding (5.32% of assets) in her flagship ARK Innovation ETF (ARKK). And it’s the second largest position (7.35%) of her ARK Genomic Revolution ETF (ARKG).

Wood’s interest here supports CRSP’s futuristic bona fides

Many have passionate views, both pro and con regarding Wood.

Back on October 28, 2022, at my old job, I penned an essay suggesting that readers “Follow Cathie Wood the Futurist… Not the Investor.”

That was the same opinion that caused me to push back on my former boss’ desire to recommend CRSP earlier that year.

I find it hard to be bullish on shares of a non-commercial company.

In my opinion, investments in non-commercial companies are best left for private venture capitalist. They latter have legal access to what we, in the public securities markets, can’t have or use, “inside information.”

Now, however, CRSP has reached the point where there’s enough legitimate publicly available information to let us think more seriously about commercial merit.

We’re not yet seeing that in reported numbers.

But we can now see that bona fide business revenues are at hand. The revenue line will soon have more than occasional (progress payments and the like) entries.

Where the Business Will Come From

Seeking Alpha Analysts who’ve been publishing on CRSP have been doing a fantastic job explaining their respective views.

I can’t and won’t try to outdo them. So, if you want details, I suggest you go to the CRSP Summary page and click away.

I’ll confine myself to a brief summary to the extent necessary to frame the investment decision we now face.

The big thing right now is Casgevy.

This is an Ex Vivo CRSP gene editing treatment for sickle cell disease (SCD).

CRSP is teaming up here with Vertex Pharmaceuticals (VRTX). The latter will handle selling and marketing. In exchange, it will get 60% of the profits.

Don’t think CRSP is being ripped off.

VRTX is an extremely valuable partner. Without support from partners like that R&D shops like CRSP wouldn’t survive, much less invent.

So the more VRTXs there are, the better for the industry.

Casgevy became the first CRISPR-cas9 approved treatment when the FDA said “yes” on December 8, 2023. It was approved for use against Sickle Cell Disease (SCD).

That’s a genetic mutation that bends red blood cells into the shape of a sickle. That often clogs circulation. This can lead to anemia, organ damage, severe pain, and potentially heart failure.

Soon thereafter, on January 16, 2024, Casgevy was also approved for treatment of Transfusion-Dependent Beta Thalassemia (TDT).

These patients’ red blood cells have abnormally low levels of hemoglobin, an iron-containing protein that carries oxygen throughout the body. Severe cases require frequent blood transfusions (i.e. they’re “transfusion dependent”).

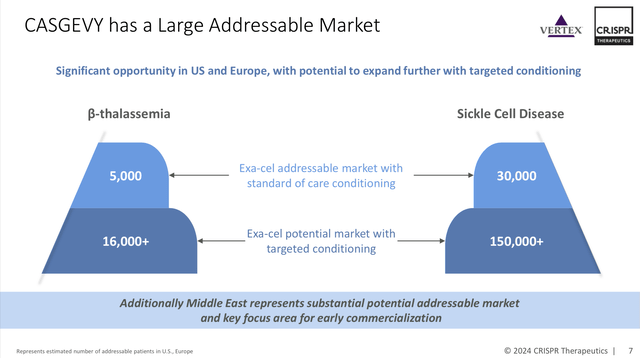

SCD is getting most of the attention right now. CRSP believes there’s a huge market for this.

CRSP IR

Note, though, that this will take time to produce financial results. It’s not like simply taking a pill.

It’s lengthy process with important preliminary steps. The patient information section of casgevy.com describes things in detail.

Briefly (very briefly) put…

- It starts with “conditioning medicines” (that may cause sterility). Mobilization medicines take stem cells from bone marrow.

- A machine then separates different cells. Some are stored for possible backup use.

- The main batch is sent to a site that makes the patient’s Casgevy.

- The Casgevy is then intravenously infused into the patient who stays at a treatment center.

- Infusion occurs gradually, potentially taking 4-6 weeks.

This is likely to require some travel. According to CRSP’s first-quarter report, there were 25 treatment centers as of mid-April.

Even without travel, Casgevy is very expensive. The one-time course of treatment is price at $2.2 million. Lyfgenia, a different protocol offered by bluebird bio (BLUE), costs $3.1 million. But insurers, including Medicaid, are working to develop payment approaches. (biopharmadive.com)

That compares to industry estimates of $1.2 million for a lifetime’s worth of other SCD treatments.

CRSP has other things in the hopper.

CRSP IR CRSP IR

But at this stage, even before the first item of commercial revenue is booked, and even before FDA approval, it’s impractical to factor any of this into numerical projections.

The May 8, 2024 Morningstar report, which gives CRSP a five-star rating based on its potential. But its CRSP analyst, Rachel Elfman, assigns “probabilities of approval between 0% and 20% to these candidates due to their early stages.”

(If you don’t have premium access to Morningstar, you may be able to get this report through the Research section of your on-line broker’s website.)

Getting to Dollars and Cents for CRSP Will Be Challenging

Back to near-term commercialization…

The Casgevy Total Addressable Market numbers suggested by the company are just that, company suggestions. There’s still a lot we don’t know.

We don’t know how many suffers will choose to undergo Casgevy treatment as opposed to cheaper, less burdensome alternatives.

Several Seeking Alpha analysts are bullish. But on June 3, 2024 Analyst Stephen Ayers was less so. He rightly said “[t]he treatment landscape for SCD and TDT (AS) complex and evolving.”

He further opined “that the market for Casgevy, at least in the early years, will be markedly limited and is more likely to surprise to the downside.”

Time may ultimately prove Ayers wrong. Like courtroom lawyers and parties awaiting a jury verdict, we’re left to wait patiently for our Jury of One… Father Time.

For now, given the level of uncertainty here, at the bare beginnings of CRSP’s life as a commercial enterprise, even if it ultimately succeeds, I also can envision lots of downside surprises early on.

And I’ve been investing long enough to know how dedicated the Street is to thinking it can estimate credibly. And I couldn’t begin to count how often the Street freaks, in one direction or the other, when a quarterly report varies.

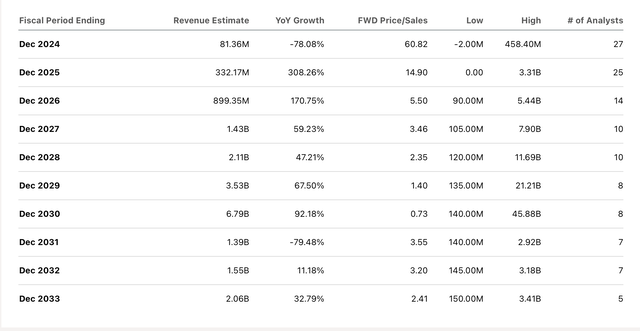

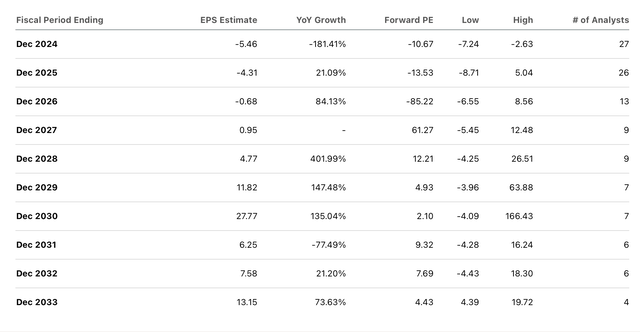

Take a look at Seeking Alpha’s compilation of consensus analyst projections for annual sales and EPS.

Seeking Alpha Estimates Presentation Seeking Alpha Estimates Presentation

It’s nice to talk about numbers like that. But to invest real money on that… Good havens no, at least not for me. There’s no data – yet – supporting any of that!

Risk

As with any not-yet-commercial-stage company, there’s one overarching mammoth-sized risk.

It’s our inability to reliably forecast.

If you’ve seen my May 28, 2024 Nvidia writeup, you have to know I love this, from the April 24, 2024 Crescent Value Research CRSP writeup:

How do you value a company with no consistent sales, earnings, cash flow, or other traditional metrics? I could try to come up with projections of future cash flows and discount them, a traditional valuation technique. That is very difficult to do and often very unreliable in mature companies; it’s almost impossible here as it’s pretty much guesswork. Yes, I may have some limited information in terms of market opportunity, list price and CRSP’s share of that, but trying to project how many patients of that market they will gain, as well as the discounts off list price that will inevitably be given is unrealistic.

That’s similar to how I presented the NVDA dilemma…

You can want to know. You can think you know. But really, you just can’t know!

I refer you to the Crescent Value writeup to see how it addresses the stock-recommendation challenge.

Below, I’ll show you how I adapt the Keynesian Beauty Contest approached I described for NVDA on May 28thto CRSP.

But before that, I’d be remiss if I didn’t address the obvious cash burn.

Any company that spends more than it takes in lives, like the Blanche DuBois character from Tennessee Williams’ “Streetcar Named Desire.” It depends on “the kindness of strangers.”

So much the more so it if doesn’t yet take in any commercial revenues.

Based on cash, marketable securities and quarterly cash burn, Ayers figures the company has an approximately 4.5 years cash runway.

My investment position doesn’t fret over that.

I believe as long as CRSP continues to show promise, strangers will keep contributing to keep it going. If it falters, it and the stock will tank. In the latter case, generous strangers won’t be able to help, unless they step in and buy the company for a lot less than today’s stock price.

The risk here is about the company’s ability to deliver commercial results, and our inability, at this stage, to really do more than guess and hope regarding the numbers.

What to do About CRSP Stock

As I did with NVDA, I’m going to borrow from behavioral finance. I’ll use the “Keynesian Beauty Contest” framework.

I’m going to act like a beauty contest judge that doesn’t pick a favorite contestant. Instead, I aim to pick the contestant I think will be most favored by the majority of other judges.

Applying that to the stock market… I’m not going to go on what I personally think of CRSP.

I’ll try to discern the views of the investment community as a whole, those whose trades will, rightly or wrongly, make or break a stock.

Let’s start with a big picture.

I’m going to compare CRSP’s share price trends to those of SPDR S&P Biotech ETF (XBI) and the Virtus LifeSci Biotech Clinical Trials ETF (BBC).

XBI is a broad-based standard benchmark against which biotech stocks can be compared.

BBC is a small specialty ETF. It invests in clinical stage biotech companies. Those are the kinds I refer to as R&D shops. There’s also the Virtus LifeSci Biotech Products ETF (BBP).

Interestingly, BBP is the fund that now owns a stake in CRSP. BBC doesn’t now have a position.

I understand this. CRSP is about to launch its first product. But still, BBC better illuminates CRSP’s history.

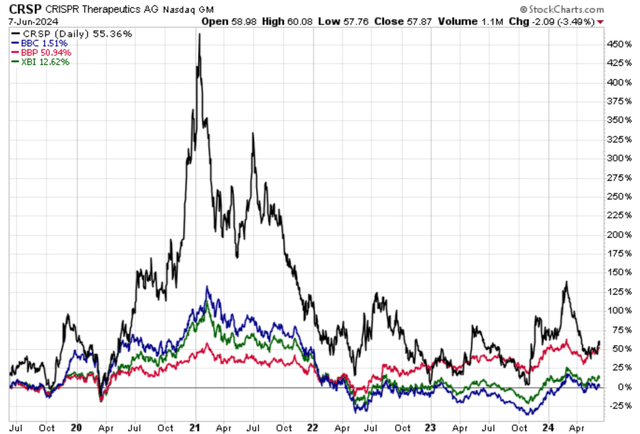

So, here’s the 5-year picture.

StockCjarts.com

Notice how BBC shined relative to BBP during the pandemic-era tech craze that peaked in late 2021. CRSP did, too…but much more so.

Now focus on 2022. We can’t help but remember how interest rates rose.

Accordingly, distant future growth-company earnings were discounted at higher rates. So present values (i.e., stock prices) fell. BBP, invested as it was in companies with-better near-term earnings, pulled ahead of BBC.

Meanwhile, reflecting the large role of clinical-state companies in its portfolio, XBI more or less mimicked BBC.

Notice, too, CRSP’s 2022 transition.

Early on, CRSP was a more volatile (and better if you like R&D-shop risk) version of the clinical-stage ETF. That reflects the “future of medicine” sentiment.

But then, as 2022 progressed and on toward the present, investors started looking ahead to CRSP’s eventual commercialization. So, more recently, it’s been a more volatile (and better if you’re risk oriented) version of BBP.

To me, this indicates that the Street is de-emphasizing CRSP’s futurist flavor. It’s thinking about commercial numbers!

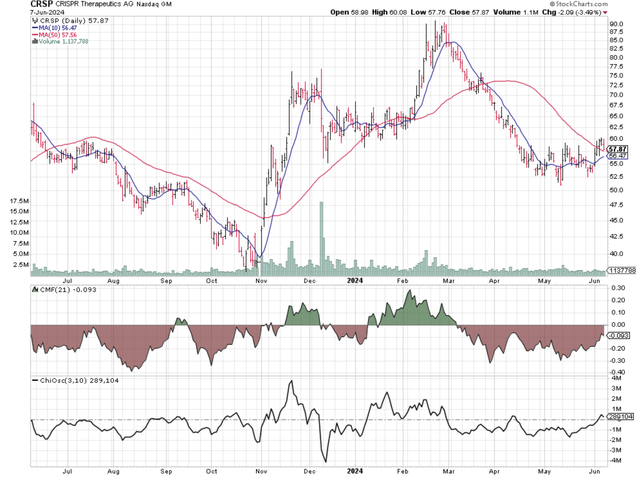

Let’s use my StockCharts.com favorite chart layout to decipher what investors, the Keynesian Beauty Contest judges, are thinking.

StockCharts.com

Let’s start with the 10-day exponential moving average (EMA). It’s approaching and may soon cross above the 50-day EMA. Bulls are asserting themselves.

We sort of see that too with the Chaikin Oscillator (CO). This indicator shows us which party to trades is more motivated. Buyers being more motivated than sellers exerts upward pressure on stock prices, and vice versa.

The CO suggested heavy seller motivation for a while. But it’s now about neutral.

Meanwhile, Chaikin Money Flow (CMF) tells a different story. It measures motivation for institutional investors. Whether they’re smarter or not, they definitely move more money. So, their sentiment matters a lot.

Institutional sentiment has been improving. But it remains well below neutral. I suspect many of them wonder, along with Ayers and I, about potential downside surprises with Casgevy’s initial results.

I won’t go bearish here. That’s in deference to the speculative potential. And I assume anybody even remotely considering CRSP has a very high tolerance for risk. But I don’t see enough now to bullishly rate the stock.

As I’ve said before, my investment stance depends mainly on whether I think a stock will be better than, in line with, or worse than the market.

Here’s how I apply that to the Seeking Alpha rating system:

- “Strong Buy” means I see the stock as being better than the market, and I’m bullish about the direction of the market.

- “Buy” means I see the stock as being better than the market, but am not confident about the market’s near-term direction.

- “Hold” means I see the stock as moving in line with the market.

- “Sell” means I see the stock as being worse than the market, but am not confident about the market’s near-term direction.

- “Strong Sell” means I see the stock as being worse than the market, and I’m bearish about the direction of the market.

Based on this scale, CRSP’s investment case having transitioned from pure futurism to product, and my inability to come up with a reason to not worry about early downside Casgevy surprises, I’m rating CRSP as a “Hold.”

Credit: Source link

{kind=link}