Darren415

After it reported its Q1 and then closed on its purchase of Florida-based VidaCann, I called Planet 13 (OTCQX:PLNH) the best American cannabis stock in mid-May. The price is 10% lower now, as the overall cannabis market has pulled back, but that’s not the only reason the best has gotten better. As I have been sharing, the company isn’t widely followed by investors or analysts. The sole analyst initiated estimates for 2025, and his outlook reinforces my bullishness.

An Updated Outlook for Planet 13

The sole analyst covering Planet 13, Canaccord Genuity, released an update on Thursday morning:

Canaccord Genuity

Matt Bottomley, the analyst, lowered his target from C$1.40 to C$1.20, but raised his rating to Buy from Hold. The target I had shared four weeks ago was US$0.77, which near C$1.06 is lower than this target.

The CG analyst lowered his estimate for 2024 revenue from $143 million to $137 million, and also reduced his adjusted EBITDA outlook to $12 million from $18 million. For 2025, though, his estimates were much higher than his outlook for 2024, with revenue projected to be $189 million and adjusted EBITDA at $32 million.

I use 2025 estimates for my year-end 2024 target prices, and I was estimating adjusted EBITDA of $29 million, which is 10% lower than the CG analyst.

The Planet 13 Valuation Is Extremely Cheap

I am maintaining my $0.77 target for year-end, which is up 39% from the close near $0.55 on Friday. My target is based on an enterprise value to projected adjusted EBITDA of 8X, though I am sticking with my own estimate. Note that my target price is also where its recently issued warrants are exercisable.

PLNH currently has a market cap of $179 million and trades at about 1X projected 2025 revenue. The stock alone trades at 5.6X the CG analyst adjusted EBITDA estimate for 2025 (6.2X my own outlook). The company has about $20 million of cash. Adjusting for enterprise value instead of market cap, the stock trades at just 5.0X the projected adjusted EBITDA (and 5.5X my own estimate).

The company trades very cheap to its projected adjusted EBITDA, but what stands out to me is the downside protection its balance sheet offers. Unlike its peers, all of whom have at least some debt if not a substantial amount, Planet 13 is debt-free. The stock trades at a very low price to tangible book value. The current ratio, which assumes that the equity didn’t increase at all from the VidaCann acquisition, would be 1.9X. My estimate is that it will be lower, which we will determine when the company reports its Q2 in August.

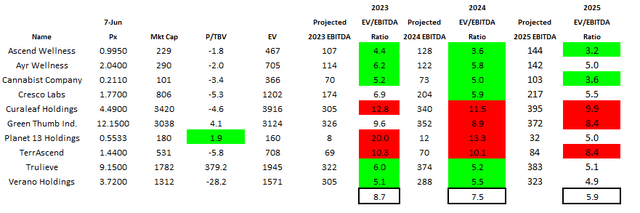

Comparing Planet 13 to the 5 Tier 1 MSOs and the 4 Tier 2 MSOs, it stands out for its low valuation:

Alan Brochstein, using Sentieo

There are a couple of cheaper Tier 2 MSOs, but the projected 5X EV/EBITDA for 2025 is below the average despite its much higher growth rate.

The Planet 13 Chart Is Promising

Planet 13 is down a bit in 2024, off by 13.6%. The New Cannabis Ventures Global Cannabis Stock Index has increased by 12.2%, while the NCV American Cannabis Operator Index, which has cooled off after a very hot first four months, is up 6.3%.

Since 8/29, the day before the rumor that the DEA had been requested by the Department of Health & Human Services to reschedule cannabis, PLNH has dropped 2.9%. The Global Cannabis Stock Index has increased by 22.6% since then, while the American Cannabis Operator Index has rallied 42.9%. Planet 13 has lagged substantially.

Looking at the one-year chart, the stock has pulled back to near its all-time low set last August:

Schwab

I see support at .48 (perhaps a bit higher), and resistance at $0.80 and $0.90. I am glad to see that the volume did pick up a lot recently. Since the peak in 2021, the stock has declined over 93%.

Conclusion

I have gotten a bit more bullish on American cannabis stocks in light of the forward momentum on rescheduling, which will wipe out the burden of 280E taxation if it goes through. It is not a done deal, but the DEA is moving towards changing cannabis from Schedule 1 to Schedule 3. If it fails to go through, it will be a very large problem for the peers of Planet 13.

When I wrote about Planet 13 four weeks ago, I pointed out that there were no estimates at all for 2025 and shared my own forecast. The one analyst who covers the stock provided an estimate for 2025 revenue and adjusted EBITDA this week, and I am very happy to see the adjusted EBITDA outlook is a bit higher than what I had estimated. I increased my already large position in my Beat the Global Cannabis Stock Index model portfolio this week to 19%, which is about the maximum position size.

Investors have been very optimistic about the MSOs in Florida and how they might benefit from the state’s potential adoption of adult-use based on a referendum in November. I am not sure that it will pass, as 60% of voters must approve it, but I am confident that Planet 13 will do very well in the state, if so.

Even if Florida fails to adopt adult-use, Planet 13 appears to be cheap and safer than other MSOs. 280E going away will help some of its peers more, but it will help Planet 13 too. My target appears to be conservative at $0.77 for year-end.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Credit: Source link

{kind=link}