Wachiwit/iStock Editorial via Getty Images

Overview and Investment Thesis

Grab Holdings Limited (NASDAQ:GRAB), one of Southeast Asia’s largest super apps, alongside Sea Limited (SE) and Gojek, encompasses various business segments, including mobility, delivery, and financial services. The super app is designed to offer a comprehensive range of essential services to meet the diverse needs of customers across the regions.

A significant component of Grab’s competitive advantage lies in its market leadership within the mobility and delivery segments, where it established itself as the go-to platform for ride-hailing and food delivery services across SEA. Specifically, Grab’s first-mover advantage, strong brand recognition, and extensive supply of demand and supply sets itself apart from other competitors. Moreover, by leveraging on its large ecosystems of users, it launched and extended its financial services to these users, including its digital payment solutions like GrabPay and DigiBank solutions like deposit savings accounts. The focus of its financial service business is to serve the underbanked and unbanked users across SEA. By providing a comprehensive suite of essential services, Grab enhances customer loyalty, drives network effects, and solidifies its position as a key player in the SEA market.

In its latest 1Q24 results, Grab reported strong growth in its mobility and delivery services, highlighting its competitive advantage as a market leader and its ability to capture market share from competitors while remaining profitable. Although its financial services segment is still in its early stages, it demonstrated robust revenue growth and a significant reduction in operating losses. I believe that the launch of its digital bank in Indonesia will trigger an inflection point in growth, leading to even more robust expansion and positive profits. With a strong balance sheet and a positive trajectory towards positive operating cash flow, Grab is well-positioned to maintain its market leadership and fend off competitors, supporting long-term profitable growth.

Discussion of 1Q24 Result

Grab’s Mobility Result

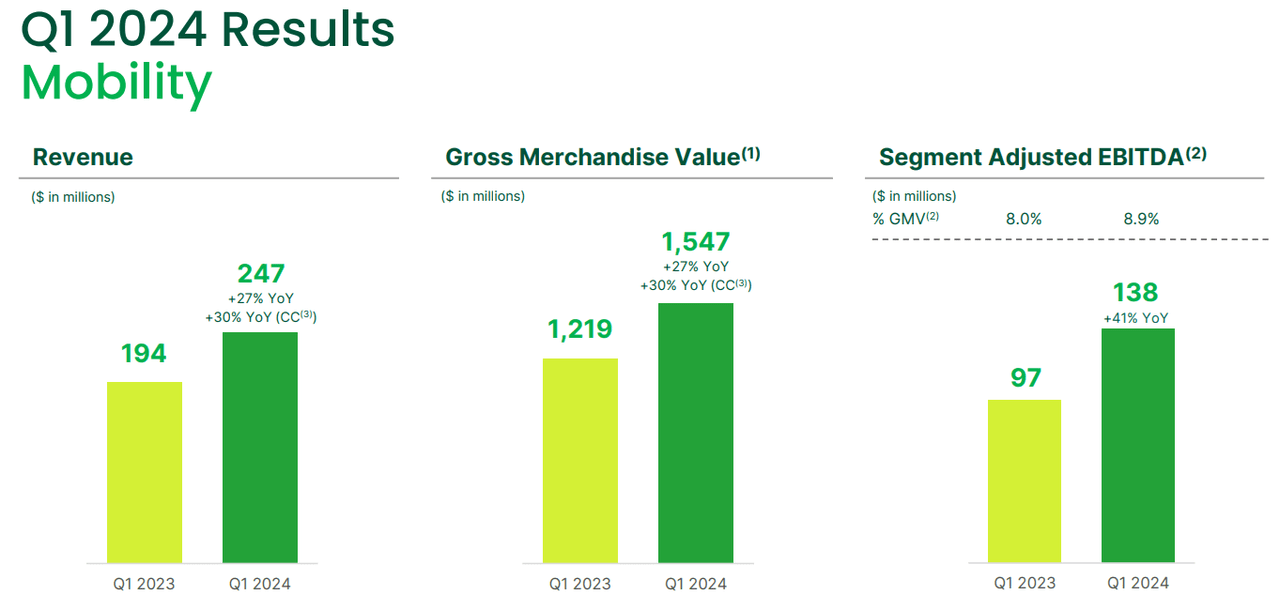

In 1Q24, Grab delivered GMV growth of 27% YOY to $1.6 billion, down from 28% YOY in 4Q23, and 32% YOY growth in FY23. The slight decrease can be attributed to a few factors, including increased promotions, with total incentives rising from 7.4% in 4Q23 to 7.7% in 1Q24 to stimulate growth, and there was an increased rebound in demand from both domestic and tourist markets.

Back in 2022, Grab witnessed a strong recovery in demand due to the post-COVID reopening across the SEA region as borders reopened and tourism rebounded. This resulted in an impressive GMV growth of 47% as they lapsed over a challenging period in FY21. Despite ongoing economic uncertainty prompting consumer spending cutbacks, the ongoing resurgence of tourism across SEA is anticipated to persist. This trend is expected to drive increased demand for Grab’s mobility services, outweighing the impact of reduced spending and contributing to continued growth in the future.

Gojek Mobility Result

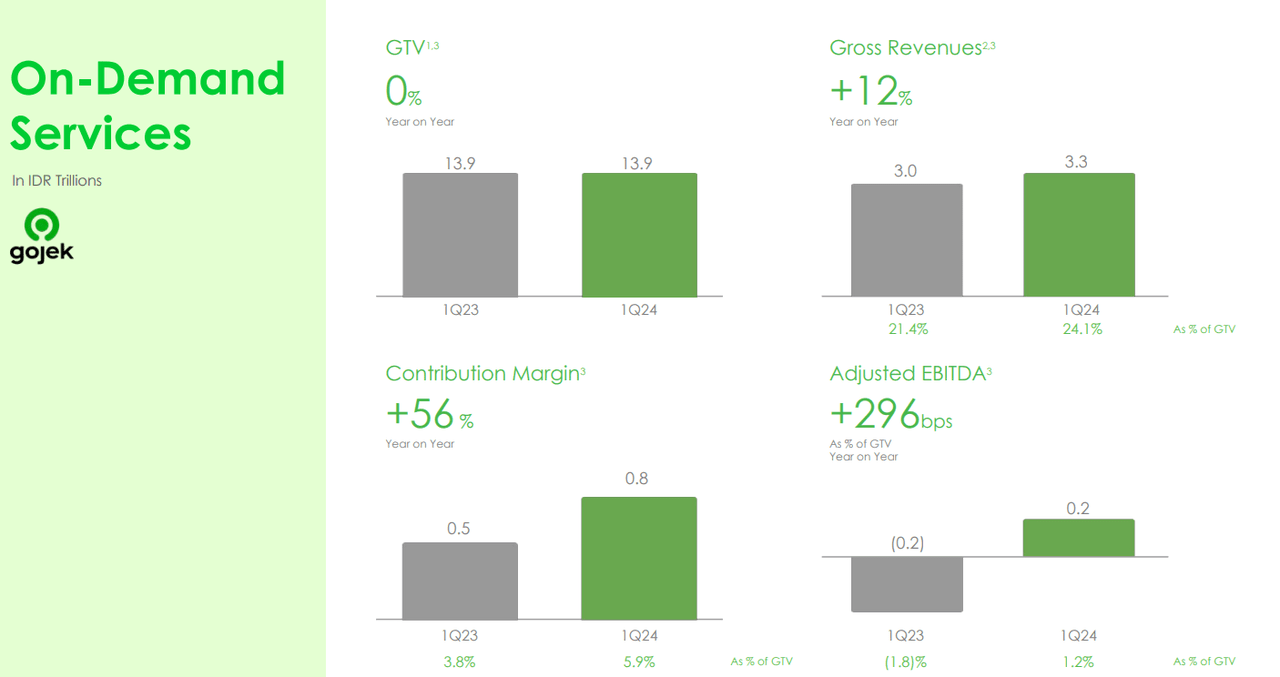

While Gojek did not provide a specific breakdown of its mobility Gross Transaction Value (GTV), its overall GTV in 1Q24 remained flat year-over-year. This suggests that Grab is capturing market share from its closest competitor, Gojek, highlighting Grab’s market dominance in the region. Additionally, Gojek’s adjusted EBITDA margin of 1.2% in Q1 2024 indicates its focus on achieving profitability. In contrast, Grab, already a market leader, can leverage its profitable position to further expand its market share, thereby widening the competitive gap between itself and Gojek.

This robust growth in GMV has led to revenue growth of 27% YOY, compared to 26% YOY growth in 4Q23. Segment-adjusted EBITDA has also improved by 41% YOY to $138 million, highlighting its strong operating leverage, which expanded its adjusted EBITDA margin from 8% in 1Q23 to 8.9% this quarter.

Food Delivery Result

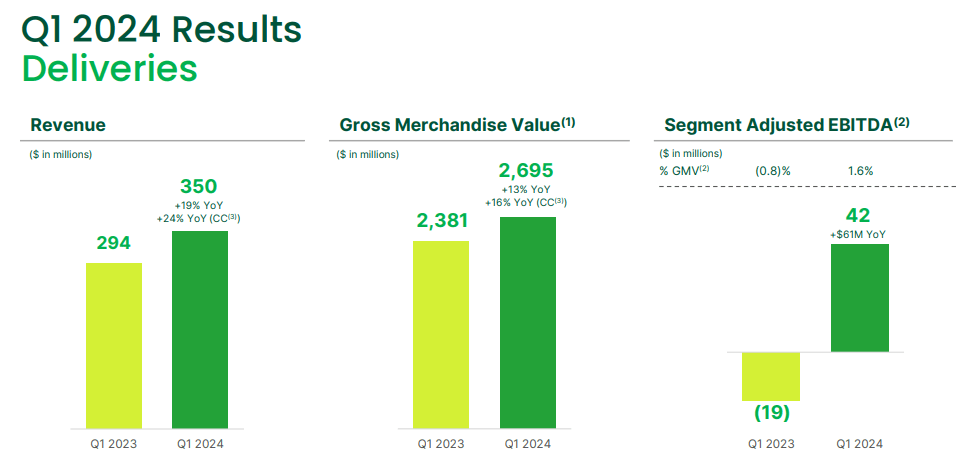

Turning to its food delivery business, its GMV grew 13% YOY, down slightly from 15% YOY growth in 4Q23, but a growth re-acceleration from 3.6% YOY growth in FY23. This 2nd consecutive quarter of double-digit growth was primarily driven by a strong rebound in demand, an increase in advertising revenue, and partially by the increase in subsidies. Additionally, during the 1Q24 earnings call, further sequential growth in GMV is expected in 2Q24, implying a continued rebound in demand from F&B spending. Shifting to profitability, its adjusted EBITDA improved by 320% YOY, expanding its margin from -0.8% in 1Q23 to 1.6% this quarter.

Unlike the mobility business, its food delivery business is more sensitive to macroeconomic conditions. With border restrictions during covid in 2021, and coupled with the rise in interest rates since early 2022 which severely reduced the demand for F&B food delivery, management has substantially reduced its incentives in the pursuit of profitability. According to a report done by MomentumWorks, SEA food delivery platforms’ total GMV only grew at a mere 5% YOY in 2023, indicating a sluggish rebound and persistent weak demand. However, as evidenced by this quarter’s results and expectations of sequential growth in GMV next quarter, this suggests that there is an ongoing resurgence in F&B spending which is likely to drive continued growth in FY24 and beyond.

Additionally, this quarter’s growth was also quite satisfactory, considering that the first quarter is typically slower for Grab due to the seasonal impacts of Chinese New Year and Ramadan. During Chinese New Year, people tend to visit family and eat home-cooked meals, and during Ramadan, Muslims abstain from eating and drinking during the day. These factors are particularly significant in regions like Singapore, Malaysia, and Indonesia, where Grab derives the majority of its revenue. Moreover, management has been proactive in introducing new services. For example, saver deliveries, which offer lower delivery fees in exchange for longer delivery times, have seen average order frequency increase by 1.8 times compared to non-saver users. Additionally, Grab’s priority delivery services, which aim to provide quicker delivery times, have experienced a 213% YOY growth and a 12% QOQ growth in transactions, now accounting for 7% of Grab’s overall deliveries. This not only demonstrates the resilience of its food delivery business but also highlights management’s innovation in enhancing customer experience by offering new services to meet diverse user needs.

In comparison, GrabFood’s closest competitor, Delivery Hero’s Foodpanda (OTCPK:DLVHF), experienced a negative 5% YOY growth for its Asia segment in 1Q24, despite being profitable, and this suggests that Grab is taking market share away from Foodpanda. Additionally, in Feb 2024, Delivery Hero’s management has terminated negotiations for the potential sale of its Foodpanda business in selected Southeast Asian markets, including Singapore, Malaysia, the Philippines, and Thailand, after “careful consideration”. However, they remain open to M&A and will proceed only when there is a high certainty of creating shareholder value. In my opinion, the fact that they remain open to acquisitions indicates the competitive nature of the food delivery business in SEA where Delivery Hero’s management prefer to focus their efforts and resources on markets where they have a strong competitive position, and competition is less intense.

Financial Service Result

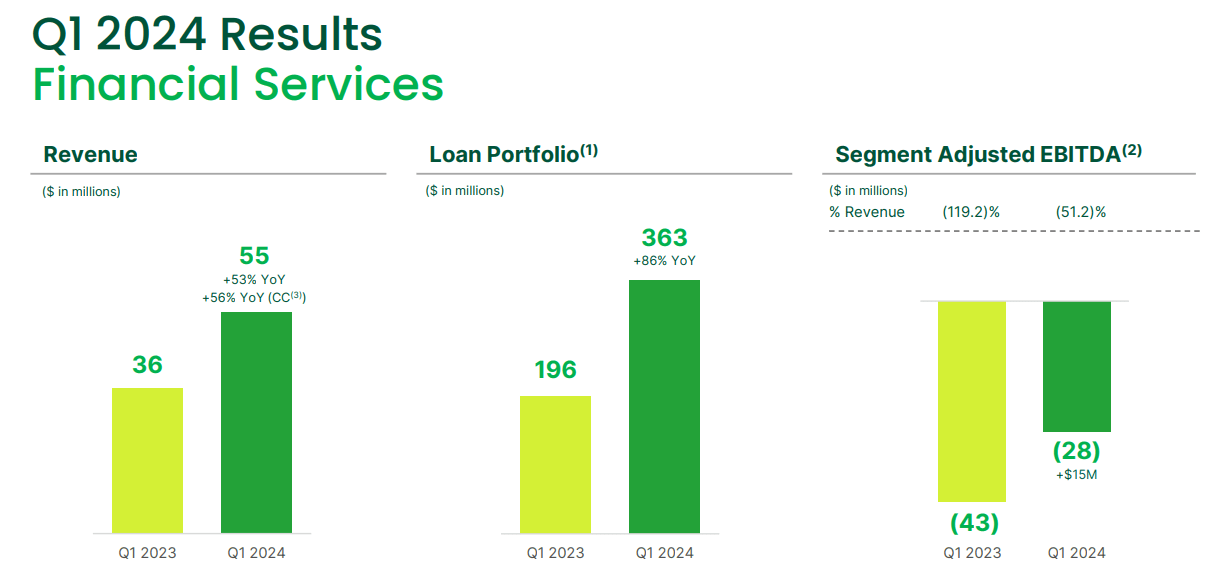

Grab achieved a 55% YOY growth in its financial services business, generating $55 million in revenue. This growth was primarily driven by increased lending activities across GrabFin and DigiBank, which grew 86% YOY to $363 million, and improved monetization of GrabFin’s payment services. The adjusted EBITDA margin for this segment improved significantly from negative 119% in 1Q23 to 51% in 1Q24, due to higher-margin revenue from lending activities and lower operating costs in GrabFin. Management expects this segment to break even by 2H26 as they continue to scale up their lending business.

In comparison, Sea Limited’s financial services segment, SeaMoney, is generating quarterly revenue of $499 million with an EBIT margin of 27%. This comparison underscores the potential margin that Grab could achieve, while also highlighting the superior execution of Sea Limited’s management compared to Grab’s. During the 1Q24 earnings call, management announced the upcoming launch of its digibank in Indonesia. In my opinion, the launch of the digibank in Indonesia will likely lead to accelerated growth, considering Indonesia is Grab’s largest market, similar to Sea Limited’s situation.

Net Cash

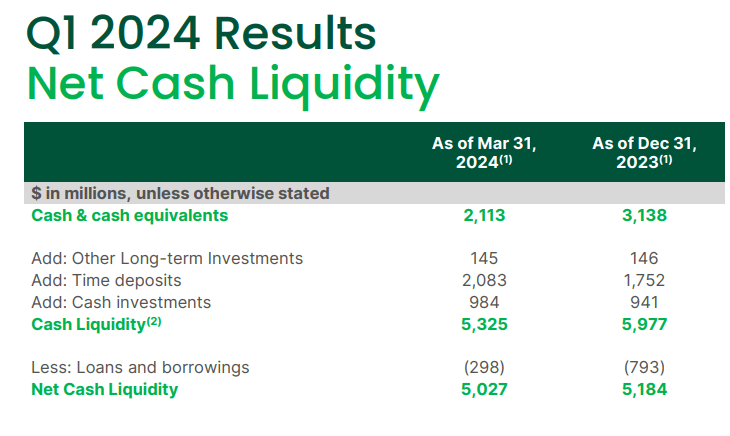

Turning to its balance sheet, Grab is in a strong financial position, with $5 billion in net cash. The company has made significant progress in reducing its debt, which decreased from $793 million in 4Q23 to $298 million this quarter, representing a 62% QOQ improvement. Over the past two years, management has significantly improved the balance sheet by reducing debt from $2.2 billion in FY22 and $1.4 billion in FY21.

Cash Flow From Operation

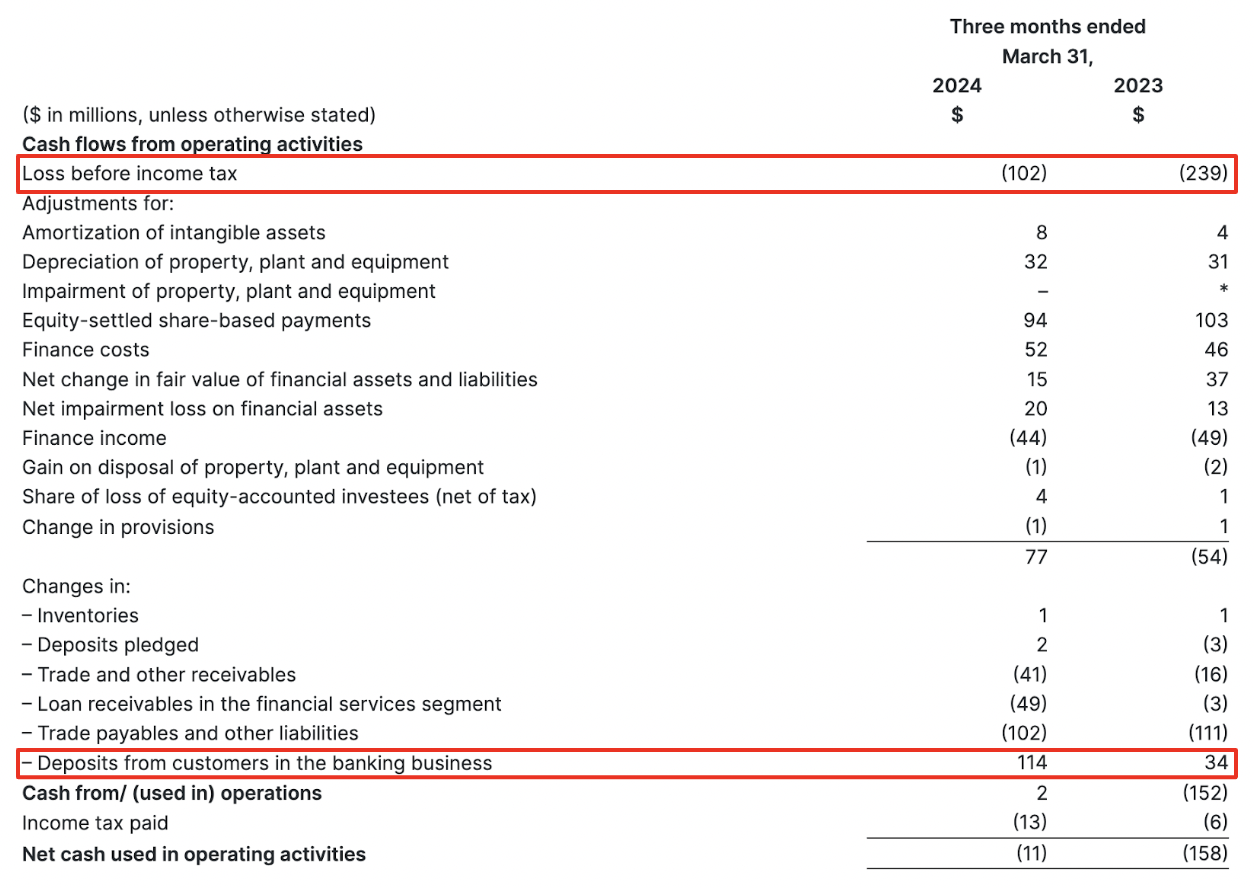

Net cash used in operations for the quarter were $11 million, a significant improvement of 99% YOY from $158 million in 1Q23, and 58% QOQ improvement from 4Q23, mainly driven by increased profitability and increased customer deposits in its digital bank, called GXS Bank.

Formed by Grab and Singtel, GXS Bank attracts users by offering a yield of up to 2.68% on deposits. As they prepare to launch their digital bank in Indonesia, Grab’s largest market, I anticipate strong synergies with Grab’s superapp will accelerate customer acquisition, leading to rapid growth in customer deposits. Coupled with improved profitability, this will put Grab on track to achieve and maintain positive operating cash flow.

Risks

Despite Grab’s market leadership position in both the mobility and food delivery business, the industry is still highly competitive. Should economic conditions improve and demand rebound, competitors may intensify their promotional efforts to expand their market share. This could prompt Grab to respond in kind, potentially impacting its margins. For its financial service segment, I highlighted the noticeable difference in execution between Sea Limited and Grab. SeaMoney has demonstrated that effective execution can lead to rapid scaling and profitability in lending services, I do anticipate Grab to adopt a similar playbook. However, any challenges or risks associated with scaling up its lending operations could impede its path to profitability.

Valuation

Author’s Valuation

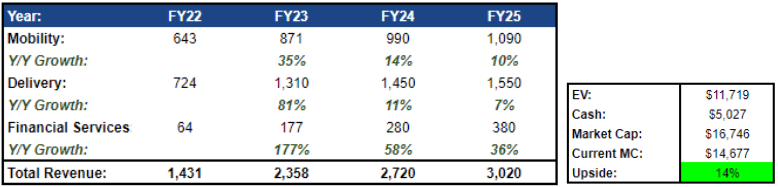

In my projections, I estimate revenue for mobility, delivery, and financial services to be $990 million, $1.45 billion, and $280 million, respectively, totaling $2.72 billion. This aligns with the midpoint of management guidance for FY24. Moving forward, I anticipate 10%, 7%, and 36% YOY growth for mobility, delivery, and financial services from FY24 to FY25. I believe this is achievable as FY24 represents a more normalized period, with growth expected to decline slightly thereafter. This would result in $3 billion in revenue by FY25.

Regarding valuation multiples, I’m referencing Grab’s closest peers. For mobility, I’ll use Uber’s EV/sales of 3.6x, as both companies hold market leadership positions in their respective markets with similar EBITDA margin profiles. For delivery, I’ll use DoorDash’s EV/sales of 4.5x for similar reasons. For the fintech segment, I’m using an EV/sales of 2x compared to the sector median multiple of 3x for PayPal, as Grab’s fintech segment is still in its early stages of development, with revenue yet to scale and profitability to be attained. This yields an enterprise value of $11 billion. Factoring in net cash of $5 billion, this generates a forward FY25 market cap of $16.7 billion, representing a 14% upside from its current market cap.

Conclusion

Grab has demonstrated its market leadership by capturing market share and delivering robust revenue growth across its mobility and delivery segments, despite facing competition in the highly competitive SEA market. Regarding its financial services segment, with improved execution, I believe Grab has the potential to scale up its revenue and margins similar to Sea Limited’s SeaMoney once its Digibank in Indonesia is launched. While still in its early stages, this segment shows promising growth potential, as evidenced by its growth rates and improvement in EBITDA losses.

However, Grab is not without its challenges. The competitive landscape remains intense, and economic fluctuations could impact demand and profitability. Additionally, executing on its financial services strategy to achieve profitability will require careful management and mitigation of risks. And, considering its valuation which suggests a 14% upside, I am rating Grab as a “Buy”.

Credit: Source link

{kind=link}