Drs Producoes

BrasilAgro (NYSE:LND) is a farmer and land developer from Brazil.

I have covered the company since December 2021. My latest article, from January 2024, maintained the thesis that the company trades for an elevated price when comparing its market cap with its cycle-average profitability. Further, given the recent bullish commodity market and the fact that the company leverages those markets in many ways (production, land prices, receivable fair value variation), investing today is risky.

In this article, I review the company’s 1H24 results and 2Q24 earnings call. This period marks the end of the planting season and the beginning of the harvesting and selling done in 2H24; therefore, it gives us a peak on FY24 profitability.

With the company’s stock price mostly unchanged since January and agricultural commodity markets turning downward, BrasilAgro is still not an opportunity at these prices.

Planting and peak into harvesting

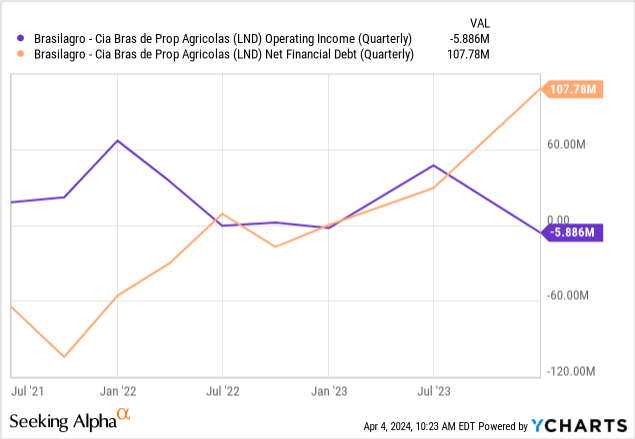

Seasonal losses and working capital accumulation: Someone reading the company’s financials for 1H24 would notice a decrease in cash reserves, an increase in debt, and operational losses.

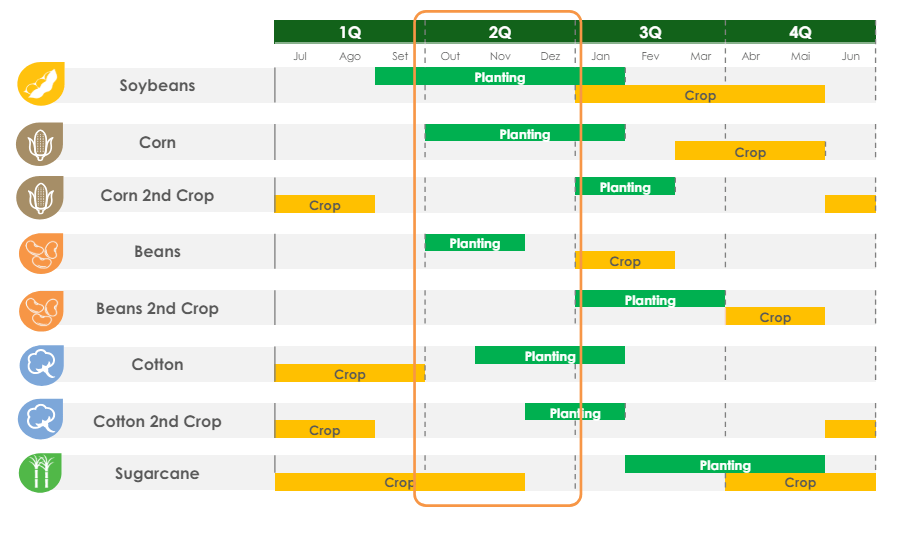

This process is seasonal and standard. The first half of the fiscal year (July to January) marks the planting season for grains (soybean and corn), which require the most significant investment in terms of working capital. The company’s financial statements show an increase of $50 million in biological assets from grains alone (soybean and corn plants on the ground). Without too many sales, the fixed cost structure (SG&A for the most part) is not as covered. The difference should be recouped in the second half. The picture below is very illustrative of this process.

Brasilagro planting and harvest cycle (LND’s 2Q24 results presentation)

Not a great 2H24 expected: There are indications that 2H24, and, as a consequence, FY24, in general, will not be a great period for the company.

First, the company has decided to plant less corn for the first harvest and very little for the second harvest because the margins are ‘negative’ according to management. Second, the Niño phenomenon is dry (negative) in Brazil, decreasing yields.

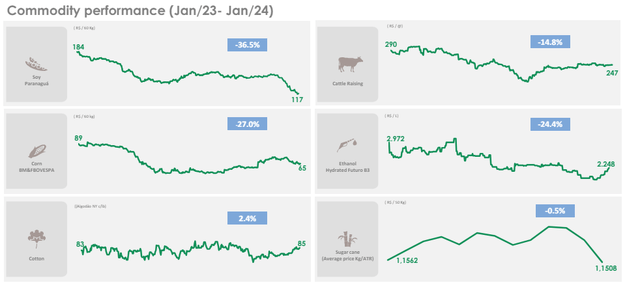

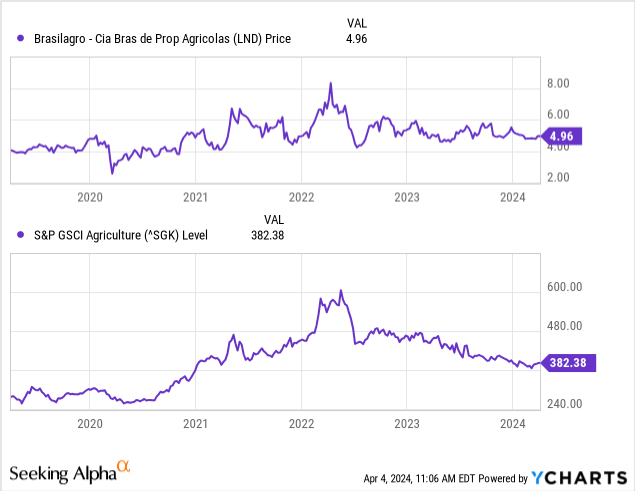

Third, agricultural commodity prices are generally decreasing (first image below). They will continue to do so, at least for the important soybean culture, as a big increase in Argentinian production is not offset by higher global demand (quite the contrary with a slowing China). For the important soybean, by 1H24, 60% of production was hedged at $13.2 per bushel (10% lower than last year’s harvest price). This year, soybeans have been trading below $12 per bushel since January (S_1:COM).

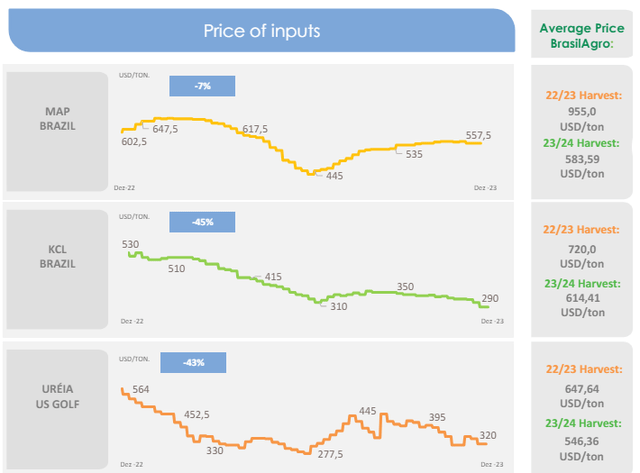

Fourth, although fertilizer prices have come down more than 40% since their 2022/23 peaks, most purchases have already been made for the 23/24 season, meaning savings are not as high (second image below, right side columns).

Agricultural prices, in Brazilian reais (LND’s 2Q24 results presentation)

Fertilizer prices (LND’s 2Q24 results presentation)

Other developments: Management also discussed other important, more long-term affecting areas.

BrasilAgro is investing in technology and infrastructure. On the technology side, the company is applying an agri-ERP system called Agrobit (a SAP partner) and installing wireless connectivity on its main farms, to move more into precision farming. This helps save on fuel and fertilizers for the most part. The company is also installing bio-fungicide preparation plants on its farms, which allow it to save on inputs. On the infrastructure side, the company is building irrigation on 4 thousand hectares in Bahia, with plans to continue this project in the dry(er) northeast of Brazil. Irrigation benefits cotton production in this region in particular.

On the real estate side, the company commented that it will probably remain a net seller of land, which is good given the cycle in Brazil. Commodity prices have been up in the past five years, so land prices in cash or multiples in produce bags (BrasilAgro’s preferred sale method) are elevated. According to management, it takes about three to five negative years for multiples to adjust down, at which time purchasing land would be more attractive. BrasilAgro is replacing land sales with maturing lands (moving from pasture to cultivation, a higher yield on land activity) and entering into long-term leases in underdeveloped lands, with the (potential) to eventually purchase those leases, although this is uncertain in my opinion.

Revisiting the valuation

Not much has changed from my latest valuation and article. The company’s stock price is flat, and agricultural commodity markets continue to disinflate after the post-pandemic boom.

As proposed in my latest article, the company could generate operational profits of $60/70 million under an optimistic scenario, as it has averaged since 2021 (ignoring land sales). After interest ($15 million) and taxes (30% in Brazil), $40 million would remain. We can see that even under an optimistic scenario (continuation of the bull cycle of commodities for the past three years), LND offers a relatively high P/E ratio of 12x (considering a $500 million market cap). This high P/E is justified by the high NAV per share based on current land prices.

However, under a pessimistic scenario, LND cannot produce much profit. Between 2014 and 2020, it averaged operating profits of $18 million, barely covering current interest expenses. The P/E ratio, in this case, is extremely high ($500 million for less than $5 million in income per year). The NAV gap would also disappear in this scenario as land prices readjust after a few years of a bear market (as commented by management in the latest earnings call).

This means BrasilAgro is still priced with an optimistic result in mind. This does not represent an opportunity. However, things could change in the second half, as relatively disappointing results, plus a prolonged bear market in commodities, could lead to more opportunistic prices. For the time being, I prefer to wait.

Credit: Source link

{kind=link}