whyframestudio/iStock via Getty Images

Dear Friends:

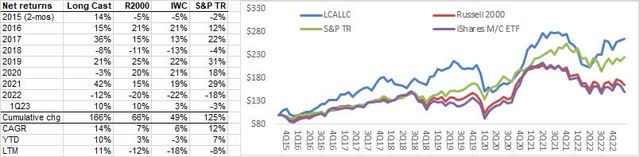

For the 1Q23 quarter (ended March 31, 2023), cumulative net returns improved 10%. Since inception in November 2015 through quarter end 1Q23, LCA returned a cumulative 166% net of fees or 14% CAGR. As a backdrop to returns, since inception we comfortably exceed two widely used representative indices for passive small company investing, the iShares MicroCap ETF and Russell 2000 Index, and the S&P. Past performance is no guarantee of future results. Individual account returns may vary.

I’ll be in Omaha this weekend for the Berkshire meeting and Markel Sunday Brunch. If you’ll be there and want to say hi, I would be thrilled to connect. Speaking of Sunday brunch, I recently participated in an Edwin Dorsey “Sunday Ideas Brunch” interview, which should be published in the coming days. It includes brief comments on two ideas, one of which (MTRX) I discuss in more depth here.

Portfolio Holdings

PESI increased over 200% in the quarter and was a significant contributor to 1Q23 returns. Other top contributors were DAIO, CCRD, and ENVX. CCRN was the most significant detractor along with OTCQX:TBTC and SOTK.

I initially wrote about PESI in the 4Q19 letter. It pairs a fixed asset “scale” business – one of only three DOE contractors licensed to treat low-level nuclear waste – with a services business comprised of engineers and folks in the field with Tyvek suits and shovels. It is still run by the same CEO who was hired in 2017 to fix what was then a moribund business. He did, doubling sales from 4Q18’s $49M ttm to $99M ttm at 3Q20. EBITDA peaked at $7M ttm in 2Q20. Pre-COVID it was on track for $150M sales which would reasonably support $12M in EBITDA. COVID heavily disrupted both services and treatment, with a notable slowdown in DOE waste transfers, but as work resumes, there is a long and wide opportunity pathway to achieving those levels.

The “sizzle on the steak” comes from the potential to process waste by “grouting it” at the company’s Perma-Fix Northwest facility, just outside the Hanford (WA) cleanup site. Recent exuberance around the stock is driven by a January 2023 “record of decision” and a March 2023 “final environmental assessment” for two different programs that would feed waste to this facility. One of these programs is expected to begin by the end of 2024.

Delays have persisted for years and I think it’s reasonable to anticipate more. No matter the timing, the potential could be large. As the CEO said on the 4Q22 conference call, discussing these opportunities: “To put this in perspective, this volume of waste would more than double the production of all of our plants combined on an annual basis. And given the fixed cost nature of our business, this could result in very significant cash flows over the next 10-year period.” Once the Hanford waste starts getting processed, an eventual price target of $30 isn’t unreasonable.

I’ve recently purchased for us two new investments and I’ll briefly discuss one below: Matrix Service (MTRX) an Engineering & Construction (E&C) company that’s adjacent to the hydrocarbon space. It bends metal, builds liquid and gas storage, conducts “turnaround” work at refineries, offers mining services, and has an additional services business in Electrical Transmission and Distribution.

The company is currently trading at around $5 / share. With 27M shares out, $15M in total debt, and $32M in cash, this yields an enterprise value of $120M. Pre-COVID this was a $400M EV company.

Industrial construction seems poised for a strong pipeline of work given the needed infrastructure for “new” energy (hydrogen, biofuels, ammonia, etc.), deferred CAPEX in traditional energy, and incremental N. American mining. This would support a rebound in MTRX’s backlog while margin reversion to pre-COVID levels offers a pathway to profitability.

The market is valuing the company on its present P&L, which is unattractive. E&C is one of the longest-lagging industries and the company is still completing work booked during COVID, when pricing was aggressive. One larger project is losing money and construction accounting requires that when a contractor realizes it is in a loss position on a project, it must immediately recognize the entirety of that loss including expected future losses through completion. These charges were recognized in the most recent quarter ended 12/31/22 (FY2Q23).

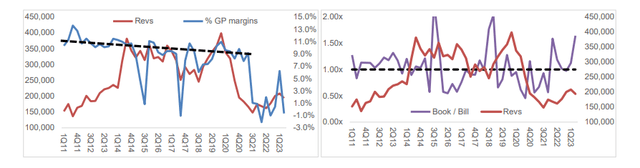

One can observe in the left chart above a blue line showing fairly consistent high single-digit gross margins in the period pre-COVID and then the immediate impact of the pandemic. The long lagging impact reflects work booked during COVID when there was a dearth of projects. Prior dips in ’15 and ’17 are due to earlier project losses, which occur from time to time in the construction business, regardless of the cycle, illustrating why it’s such a crazy industry. The right chart shows the book-to-bill ratio (purple line). Anything over 1x means the company is adding more work and the backlog is growing.

For the last six quarters, book-to-bill has been at or above 1x. Management at MTRX and at other E&Cs exposed to similar end markets talk about a robust pipeline of pending work supporting new and traditional energy. If MTRX is booking work near its historical margins as management says it is, this should unfold quite nicely for investors.

The same management has been in place for over a decade; they’ve guided the company through prior cycles. The balance sheet is healthy and can support loss projects through completion. Random intangibles like weather can have a material impact on the business, so this can be a frustrating industry to invest in. But the time to buy E&C companies is when the income statement is at its worst and backlog growth lies ahead. That defines the present opportunity.

In Conclusion: On Growing Wealth

MTRX is our first hydrocarbon adjacent investment, a part of the market I’ve long said I’d avoid. The underlying support for avoiding hydrocarbons was a more than twenty-year-old argument with a college friend, now a chemist and environmental scientist at Princeton, to whom I could not then defend part ownership of businesses that were despoiling our environment.

Much has changed over the years. Where “the majors” once treated environmental regulations with antipathy, now they are making – and in some cases leading in – investments in hydrogen, in carbon capture, in biofuels, and in other parts of the energy transition. Furthermore, the reality is that hydrocarbons will be part of our energy diet for years – it’s got to come from somewhere – and N. American production is among the most responsibly produced.

My business is to try to create generational wealth for myself and clients. My entire investable net worth is invested alongside yours. Given my years covering the E&C space, whose largest customers are broadly in the hydrocarbon space, my experience and expertise offer an advantaged perspective and it’s irresponsible for my ultimate objective of creating generational wealth to avoid that area for didactic reasons. I’m happy to discuss this directly and in more detail.

I remain committed to building a durable and sustainable business based on a repeatable investment process and intelligent capital allocation. As always, I appreciate your entrusting me with your capital and the responsibility of being its steward. I look forward to continuing this conversation in the future.

Sincerely/Avi

Brooklyn, NY, May 2023

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Credit: Source link

{kind=link}