da-kuk

Thesis

While the investor interest in fast-growing technology stocks arguably peaked in late 2021, the pullback that followed offered a more long-term perspective for investors in the tech sector. Many have since chosen to gain exposure to technology stocks using a more conservative approach; ETF investing. Fidelity Nasdaq Composite Index ETF (NASDAQ:ONEQ) offers a tested gateway for investors in the universe of technology and in this analysis I explore the fund’s attributes and performance, as well as the current technology sector market positioning.

ONEQ ETF Overview

Fidelity Nasdaq Composite Index ETF aims to provide investors with exposure to the technology sector by tracking the Nasdaq Composite Index. Incepted in late 2003 the fund has a strong performance track record, over $5.0B in Assets Under Management, and charges a relatively inexpensive 0.21% expense ratio. The fund pays a 0.75% dividend yield and has received a 5-star rating by Morningstar for the past decade.

The Tech Layoff Debate

With over 270 thousand layoffs in the tech industry in 2022 and a sharp pullback for almost the entire sector in the stock market, investors grew particularly pessimistic. According to many analysts, broad layoffs indicate worsening prospects and poor growth prospects for the sector going forward.

But what if the piling layoffs simply present as a symptom of the sector overextending, particularly within the aggressive growth and high valuation segment, and represent, as such merely a form of reverting back to normal operations? After all, the macroeconomic (fiscal and monetary) euphoria in the post-Covid-19 led to tech companies overestimating themselves and their growth capabilities. As the reality check is delivered, the tech sector likely still maintains solid growth prospects going forward and necessary downsizing efforts could actually help improve efficiency and control the cash flow bleeding that many tech firms display still today.

Technology at an Interesting Positioning

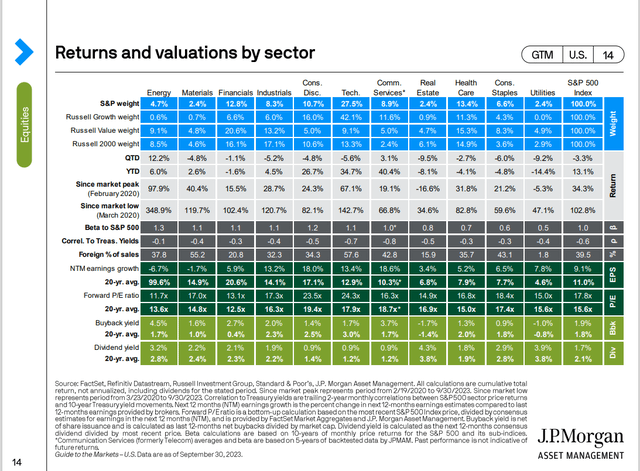

More than perhaps any other sector, Technology stocks are led in the market by mega-caps, including Apple (AAPL), Microsoft (MSFT), and Google (GOOG). Even though the broader sector has continued to struggle in a tighter macroeconomic environment these firms have actually recorded strong performance which is not indicative for the entire sector.

As a result, apart from a false picture of broader recovery that is painted over the technology sector, both its weighting and concentration have also increased. Technology stocks now account for 27.5% of the S&P 500 and over 40% of many large-cap growth indexes. YTD the sector has returned 34.7% (led by mega-caps), beating every other sector except communications.

A sector beta of 1.1 is again not highly representative of the higher risk the majority of technology firms add to a portfolio, as it is biased downwards by big movers like AAPL, MSFT and GOOG that vastly impact average market performance.

On the other hand, higher-than-historic-average earnings growth (13.4% vs 12.9% 20-year average) offer bullish signs going forward. Technology also offers the broader geographic diversification among sectors, with 57.6% of sales originating outside of the United States.

While still overvalued compared to both market and historical averages (24.3x P/E vs 17.9x 20-year average), sector valuations have returned to much more reasonable levels since the peak of the Covid-19-induced rally that ended in late 2021. Both share repurchases and dividend yields for the sector are lower than market averages (1.7% and 0.9% respectively)

J.P. Morgan Asset Management

Overall, I think that a bullish case for the sector in the mid and long term can still be substantiated today, especially given increased technological penetration in arguably every aspect of business and everyday life. Risks mainly stem from high valuations that could cause underperformance in the mid-term and also the sector’s high cyclicality that could lead to high volatility and a pullback in recessionary times.

Consistently Beating the S&P 500

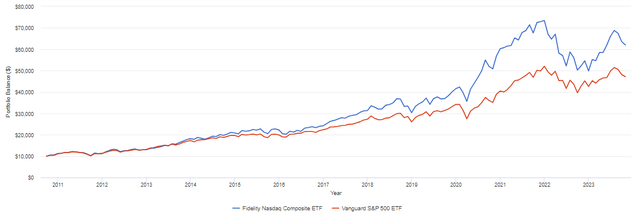

Fidelity Nasdaq Composite ETF has consistently outperformed the S&P 500 (Vanguard’s VOO) over the past 12+ years. The performance gap became evidently wide during the Covid-19 rally in late 2020 and 2021 and has widened again in 2023. An initial $10,000 in ONEQ in late 2010 would have returned today almost $62,000, marking an impressive 520% total return. For the same reference period and initial investing balance the S&P 500 would have yielded just over $41,000.

Portfolio Visualizer

Even though return metrics uniformly point to superior performance by ONEQ compared to the S&P 500, risk metrics lead to a more cautious conclusion. ONEQ displays a significantly higher standard deviation of returns and maximum drawdown (17.1% vs 14.4% and -32.1% vs 23.91%). On a risk-adjusted return basis the technology ETF still outperforms, as evidenced both by a higher Sharpe and Sortino ratio compared to the S&P 500 (0.85 vs 0.84 and 1.39 vs 1.31 respectively)

Portfolio Visualizer

Rival ETFs for Tech Bulls

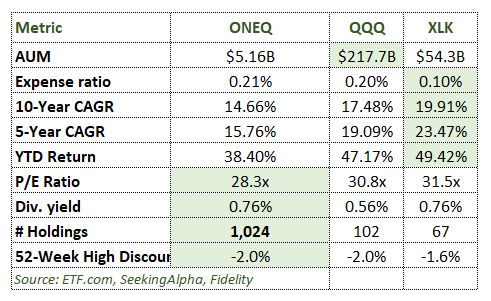

While a number of tech-friendly ETF investors have chosen, ONEQ as their choice to track the NASDAQ Composite Index or tech sector returns in general, there are actually many other ETF choices available for investors, including some significantly larger funds, the key attributes of which I compare to ONEQ’s in this segment.

Invesco QQQ ETF (QQQ) and Technology Select Sector SPDR Fund ETF (XLK) are the two most popular technology-focused ETFs. In terms of performance, both QQQ and XLK have outperformed over the past decade and on a YTD basis. Additionally, ONEQ charges the highest expense ratio of 0.21%. However, it is the least expensive fund and far more diversified compared to its peers.

Author’s Research

Final Thoughts

After all things are considered, it is likely that the tech sector will continue to perform well over the mid-term despite some risks related to cyclicality and relatively high valuations. Despite more popular ETF options that have outperformed over the past decade, ONEQ still stands to benefit tech-bullish investors.

Credit: Source link

{kind=link}