StockByM

Acacia Research Corporation (NASDAQ:ACTG) completed last month the recapitalization transaction it entered into with Starboard Value (“Starboard”) last October. This is a major milestone for the Company that (i) marks a shift in focus from investments with a one-time return potential to long-term investments that have the potential to compound over time; and (ii) aligns the interests of Starboard, the new controlling shareholder – a private fund managing roughly $4.6 billion, with those of minority shareholders, as it flattened the Company’s capital structure. ACTG’s shares are priced as of the close of trading on August 18, 2023 at just a slight premium to cash and a hefty discount to book value (both on a pro forma basis – as if the recapitalization transaction was completed on June 30, 2023). With Starboard’s network, resources and experience, there is a good potential for long-term value creation. The low share price offers an attractive opportunity to get one’s foot in the door.

According to Yahoo Finance:

ACTG invests in intellectual property and related absolute return assets; and engages in the licensing and enforcement of patented technologies. The Company operates through two segments, Intellectual Property Operations and Industrial Operations. The Company owns or controls the rights to various patent portfolios, which include U.S. patents and foreign counterparts covering technologies used in a range of industries. It is also engaged in the printing business.

That description primarily relates to ACTG’s business pre-recapitalization, as shall be further explained below.

New Controlling Party

I have been following ACTG for some time now. What initially aroused my curiosity about it is the involvement of Starboard, a multibillion-dollar activist fund. It is not every day that you see an activist hedge fund with multibillion dollars under management seeking to take over a publicly traded company (as opposed to trying to get it to engage in certain transactions such as M&A, spin-off etc. that could potentially unlock value).

These hedge funds, typically, initially take a position in a publicly traded company they find some interest in, which is small enough not to become an interested party and by that enabling them to buy some time to keep exploring the opportunity further while remaining, at least for the time being, under the radar. Should their conviction level grow stronger after taking an initial stake in a company, they may increase the size of that position, sometimes along the way crossing the 5% beneficial ownership threshold making them an “interested party” subject to the SEC reporting requirements. However, still if the “interested party” threshold is crossed, it is not ordinary to see an activist hedge fund taking over a publicly traded company with the expectation of turning it into a platform for some of its future investments.

Starboard is a private fund that manages ~$4.6 billion according to its latest 13F filing. A fund of such magnitude has access to a vast flow of potential deals for it to examine and most likely the ability to bring in co-investors to attractive deals, which could widen the spectrum of investment opportunities for ACTG.

Shift In Focus & Aligning Interests With Minority Shareholders

In ACTG’s Q4 2022 call, it was said that:

Under prior management, the primary focus was on transacting in complex situations, breaking them apart or restructuring them, and selling assets to create a one-time return. You may have heard the term in applied investment banking in this regard. While we may find such opportunities in the future, it is not our primary focus as it inherently minimizes the interest and focus in acquiring operating companies, especially as our goal is to acquire businesses with the eye of owners. Our vision and that of our Board is to build a portfolio of operating companies that can create compounding value over the long-term.

Also, in ACTG’s Q3 2022 call, it was stated that:

With Acacia, we now have a hybrid solution, a platform in vehicle that we believe brings the most effective parts of hedge fund and private equity structures together.

That hybrid solution in a publicly traded vehicle seems to create a win-win situation for ACTG and its shareholders by allowing a hedge fund-type vehicle to benefit from permanent capital which strengthens the ability to stick to a long-term strategy, potentially reaping the fruits of compounding, while allowing investors the agility to decide when to cash out.

The foregoing is bolstered by the following notes made in ACTG’s latest quarterly call:

We reorganized Printronix and our new leadership reducing costs improving efficiency and setting the stage for an evolution of the business model that we believe will generate more predictable cash flows. And importantly, we put a corporate incentive plan in place for employees of our parent company to clearly align our team’s incentives, with those of our shareholders.

Purpose Of The Recapitalization & Rights Offering

During the last 3 years, ACTG’s capital structure was quite complicated with Starboard owning preferred shares, two series of warrants and notes in ACTG. Complicated, multi-layered capital structures are often times a deterrent to investors, causing depressed stock prices. Presumably taking that into consideration and realizing that the Company will likely be looked at more favorably should its capital structure be simplified, in Q4 of 2022, ACTG and Starboard entered into a recapitalization agreement, the end result of which would be flattening the capital structure of ACTG, leaving ACTG with only common stock and very low debt. That recapitalization transaction was completed last month.

Part of the recapitalization was a rights offering at $5.25 a share, which Starboard undertook to participate in by purchasing at least 15 million shares. The rights offering price reflected a hefty premium of nearly 35% to the price of ACTG’s stock, which stood at $3.90 at closing of the last trading day prior to the announcement of the recapitalization agreement (although it makes sense to consider the price of the rights offering in the wider context of the entire recapitalization agreement, which includes a “recapitalization payment” to Starboard representing a negotiated settlement of the foregone time value of the Series B Warrants and the Series A Preferred Stock).

Implications of the Recapitalization

ACTG mentioned in its latest quarterly call the following:

The completion of the recapitalization transactions resulted in an incremental $166.8 million increase in book value and an incremental $41.4 million increase in shares outstanding. Adjusted book value as adjusted to give effect to the transaction as if it had been completed on June 30, 2023 rather than July 13, 2023 would be $502.2 million and diluted shares outstanding would be $99.9 million, resulting in an adjusted book value per share of $5.03 at June 30, 2023.

It was added by ACTG that:

On a pro forma basis, assuming completion as of June 30, 2023 of all phases of the Starboard transaction our cash per share would be approximately $3.44 per share.

ACTG’s stock price as of the close of trading on August 18, 2023 was $3.70, reflecting, on a pro forma basis, just a small premium of 7.5% on its cash and a substantial discount of 26.5% to its book value. Moreover, a stream of cash is expected given ACTG’s note in its latest quarterly call, according to which it is anticipating monetization events with respect to some of its remaining holdings in legacy life science assets in the not-too-distant future.

Having now the flat capital structure in place and with Starboard at the helm, I believe access to additional capital at reasonable terms, through Starboard’s own sources and/or through its network, should be within reach when attractive investment opportunities emerge. The nature of the recapitalization deal, which streamlines the capital structure of ACTG, supports a long-term approach, indicating that Starboard is there to stay.

I anticipate the current holdings of ACTG to gradually become a small, even marginal, part of its operations as it transitions towards its current goal of building a portfolio of long-term compounders.

Also, it is worth mentioning, that ACTG is not expected to bleed cash in the short term while it is looking for investment opportunities, since as a result of the recapitalization transaction ACTG reduced its cost structure in a meaningful way, which should allow it to cover its ongoing fixed corporate costs from interest earned on its cash and cash equivalents.

Margin Of Safety & Potential Catalysts

A discount of 26.5% to the pro forma adjusted book value, in a Company having a rock-solid balance sheet, strong cash position (comprising more than 2/3 of the adj. book value), low fixed costs, with good prospects for value creation leveraging the expertise and vast network of Starboard provides a decent margin of safety.

ACTG’s stock may have been missed by many due to its small size and limited coverage. However, once acquisitions start flowing in, I believe the stock price will respond, closing the current gap between the market price and the pro forma book value and going even higher to reflect the potential for long-term value creation enabled by the use of permanent capital to invest in long-term compounders with the backing of a multibillion-dollar private fund.

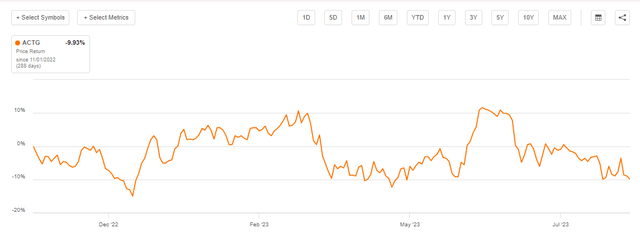

ACTG’s stock price has been sluggish despite the meaningful progress with the recapitalization transaction and even after its completion, which represents a major milestone in ACTG’s transformation.

ACTG stock performance since the recapitalization transaction was announced:

Seeking Alpha (8-18-2023)

ACTG stock performance year-to-date:

Seeking Alpha (8-18-2023)

It seems that ACTG now needs a catalyst that would trigger favorable reaction by the market and bring to light the potential for value creation in this newly-designed investment platform. That catalyst could be in the form of an announcement of a first significant investment under the new leadership of Starboard.

Some initial signs of that long-awaited catalyst may be seen on the horizon given the notes made in ACTG’s press release pertaining to the Q2 2023 financial results, where Martin D. McNulty, Jr. “MJ”, Interim Chief Executive Officer, stated:

We successfully completed the recapitalization transaction with Starboard Value LP, which follows on the heels of our transformation of Acacia by revamping our processes for identifying and pursuing transactions and establishing the framework to support acquisitions of both public and private companies. I am confident that we have the right team and processes in place, along with incentives to create value. Our pipeline of acquisition targets has grown and matured, and we are methodically advancing specific opportunities.

Asked about sell-side analyst coverage on the Q1 2023 call, Martin McNulty replied:

…I think the time to start talking to sell-side analysts is when we started to put some points on the board and are showing that we have a good pipeline that we’re getting deals done.

Growing interest from analysts could serve as another catalyst.

Risks To My Thesis

Although the recapitalization is now completed, which, as previously indicated, in my view, shows that Starboard is likely in ACTG for the long-term, there is always a possibility that Starboard will decide to get out of the Company at some point and if that happens, ACTG will lose access to Starboard’s valuable network, resources and experience. Another risk is that ACTG’s future investments (or a majority of them) will not pan out as expected. In addition, the matters I described above as potential catalysts may not have a positive effect on the stock price.

Conclusion

To summarize, I believe that Starboard’s size, network, experience and the vision for ACTG moving forward, which focuses on finding long-term compounders, along with the new flat capital structure, aligning Starboard’s interests with those of minority shareholders, present a real opportunity for ACTG to generate long-term value for its shareholders. The current stock price, with a decent margin of safety, offers an attractive entry point.

Credit: Source link

{kind=link}